Understanding Surrender Value & Paid-Up Value in Life Insurance

Learn about the significance of surrender value & paid-up value in life insurance policies, how they are calculated, and the factors influencing them. Make informed decisions about your life insurance investments.

Understanding Surrender Value & Paid-Up Value in Life Insurance

E N D

Presentation Transcript

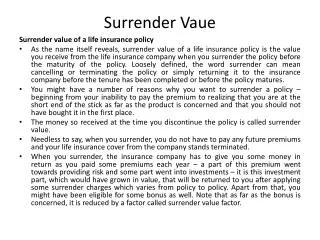

Surrender Vaue Surrender value of a life insurance policy • As the name itself reveals, surrender value of a life insurance policy is the value you receive from the life insurance company when you surrender the policy before the maturity of the policy. Loosely defined, the word surrender can mean cancelling or terminating the policy or simply returning it to the insurance company before the tenure has been completed or before the policy matures. • You might have a number of reasons why you want to surrender a policy – beginning from your inability to pay the premium to realizing that you are at the short end of the stick as far as the product is concerned and that you should not have bought it in the first place. • The money so received at the time you discontinue the policy is called surrender value. • Needless to say, when you surrender, you do not have to pay any future premiums and your life insurance cover from the company stands terminated. • When you surrender, the insurance company has to give you some money in return as you paid some premiums each year – a part of this premium went towards providing risk and some part went into investments – it is this investment part, which would have grown in value, that will be returned to you after applying some surrender charges which varies from policy to policy. Apart from that, you might have been eligible for some bonus as well. Note that as far as the bonus is concerned, it is reduced by a factor called surrender value factor.

To understand this better, let us look at the formula by which insurance companies arrives at the money they give to you. Surrender Value = [ {(Number of premiums paid / Number of premiums payable) * Sum Assured } + Accrued bonuses ] * Surrender value factor • If I want to explain with an example, let us say you have paid premium of Rs 14,000 each year for 3 years now for a policy with Sum Assured of Rs 2 lakhs which has a tenure of 15 years. You decide to terminate or surrender the policy. • Assume that you have accumulated a bonus of Rs 10,000. • The surrender value = [{(3/15)*2,00,000} + 10,000]*0.25 = Rs 12,500 • If you had stuck with paying the premiums for 6 years, the value would have been Rs 22,500 – if you look at the above example, you will note that the more number of premiums you pay, more is the surrender value. • Note that there is a rough thumb-rule to get to this surrender value – insurance companies usually pay 30% of the first 3 years premium back to you, minus the first year premium. • It must be noted that the surrender value is given out only when the life insurance policy has been in existence for 3 years. So if you want to surrender after a year or two, you will get no money. The money is received from the insurance company only after 3 full premiums have been paid.

Paid-Up value of a life insurance policy • What if you want to stop paying the premiums for the policy but do not want to terminate the policy ? The insurance company provides you with an option where in they will let the policy continue to its maturity with no premium expectation from you – the requirement is that the sum assured that was in existence when the policy was taken will now be reduced substantially. This is done by making the policy paid-up. • So when you make a policy paid-up, it still is in force with a reduced sum assured and does not discontinue. The reduced sum assured is called the paid-up value of the policy. • Here is the formula for Paid-up : • Paid-Up Value = (Number of premiums paid / Total number of premiums payable) * Original sum assured • In the above example that we took, the policy has a paid-up value of Rs 10,000 after 3 years. • Once you make a life insurance policy paid-up, it does not qualify for any bonuses. Note that the paid-up value is the amount you will receive when the policy matures or the money the nominee receives if you were die. • If you re-look at the surrender value formula, you will realize that it can be re-written as • Surrender Value = [ Paid-Up Value + Accrued bonuses ] * Surrender value factor • The surrender value factor is zero for the first three years and keeps rising from third year onwards. It differs from company to company and depends on various factors.