NFIP Flood Insurance

170 likes | 318 Vues

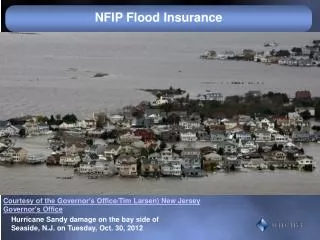

NFIP Flood Insurance. Courtesy of the Governor's Office/Tim Larsen) New Jersey Governor's Office. Hurricane Sandy damage on the bay side of Seaside, N.J. on Tuesday, Oct. 30, 2012. Biggert-Waters Flood Insurance Reform Act 2012. Increase Annual Premium from 10% to 20% Phase in Actuarial Rates

NFIP Flood Insurance

E N D

Presentation Transcript

NFIP Flood Insurance Courtesy of the Governor's Office/Tim Larsen) New Jersey Governor's Office Hurricane Sandy damage on the bay side of Seaside, N.J. on Tuesday, Oct. 30, 2012.

Biggert-Waters Flood Insurance Reform Act 2012 • Increase Annual Premium from 10% to 20% • Phase in Actuarial Rates • Pre-FIRM Non-Primary Homes • Pre-FIRM Business • Estimated 25% each year • August 2013 No Longer rate subsidy for: • Property not insured by NFIP • Property purchased • Policies that lapse • Increase Lender’s Penalties from $350 to $2,000 per violation

Advisory Base Flood Elevationswww.region2coastal.com/sandy/abfe • Dec 15, 2012 10 NJ Counties including Ocean and Monmouth Counties • Visit Web-site to determine any changes in Flood Zone or BFE • Communities must still adopt new maps and new BFEs Wind blows across a flooded street as Hurricane Sandy moves up the coast on October 29, 2012 in Atlantic City, New Jersey. / Getty

Effects of the Map Changes - Flood Zones • Moderate And Minimal Flood HazardAreas (non-SFHA) • Zone B, C OR X • Special Flood Hazard Areas • A, A1-A30, AE, AO, AH, A99, AR • Inland, Rivers, Lakes, Low-Lying Areas • V, V1-V30, VE • Ocean Front

Preferred Risk vs. Standard Policy • Preferred Risk Policy (PRP) • Must be in zones B, C, OR X at time of application • Fixed premiums; fixed limits • Limited Loss History • Standard • Rates in Manual • Flexible • Those that do not qualify for a PRP and SFHA Note: The PRP extension allows the insured to purchase a PRP for 2 years from effective date of a map change which moved a risk from a B,C or X zone into a high risk flood zone.

Pre- or Post-FIRM Before 12/31/74 or Before the Original FIRM Date After 12/31/74 or After the Original FIRM date Pre Post

Substantial Improvement/Damage • Reconstruction, Addition, Rehab or improvement of a building, the cost of which equals or exceeds 50% of the Market Value before the start of Construction • Use the Substantial Improvement Date as the Date of Construction

Two Year Preferred Risk Policy Eligibility ExtensionFEMA Bulletin W-12054 • Under the 2 year PRP Eligibility Extension, buildings newly map into a SFHA on or after 10/1/2008 became eligible effective 1/1/2011 for a two year extension. • At the end of the 2 year period the policies would be rewritten as standard-rated policies. • Currently this program has be extended until further notice for both renewals and new map revisions.

Grandfather Rules • Allows a property owner to lock in a Flood Zone and/or a BFE • Pre-FIRM • Obtained prior to the effective date of a map change, the Policyholder is eligible to maintain the prior zone and base flood elevation as long as continuous coverage is maintained. • The policy can be assigned to a new owner at the option of the policyholder.

Grandfather Rules • POST-FIRM • If a building was constructed in compliance with a specific FIRM, the owner is always eligible to obtain a policy using the zone and base flood elevation from that FIRM, (must provided that proof). Continuous coverage is not required. • Obtained prior to the effective date of a map change, the Policyholder is eligible to maintain the prior zone and base flood elevation as long as continuous coverage is maintained. • The policy can be assigned to a new owner at the option of the policyholder.

Increase Cost of Compliance (ICC)Coverage D • Will pay up to $30,000 • Maximum Property plus ICC can not exceed Act • Residential $250K • Non-Residential $500K • Eligible for buildings classified as substantially damage and/or repetitive loss structure in which community has a provision in its Floodplain Management Law Ordinance. • ICC Options • Elevation – to raise home • Relocation – move home • Demolition – clear site including discontinue utility service • Floodproofing – primarily for non-residential buildings. Involves making the building watertight.

Photo Credit: Photo via Brian Thompson/ Lockerz Damage From Hurricane Sandy in Seaside Heights, New Jersey: Casino Pier Roller Coaster