Download

1 / 23

230 likes | 652 Vues

Flood Insurance Regulations Justin M. Anderson, Esq. Staff Attorney National Credit Union Administration Overview Statutes (Flood Disaster Protection Act, National Flood Insurance Act, and National Flood Insurance Reform Act of 1994) NCUA’s Flood Insurance Regulation

E N D

Flood Insurance Regulations Justin M. Anderson, Esq. Staff Attorney National Credit Union Administration

Overview • Statutes (Flood Disaster Protection Act, National Flood Insurance Act, and National Flood Insurance Reform Act of 1994) • NCUA’s Flood Insurance Regulation • How Flood Insurance Works • Insurance Procedures • Questions and Answers

Section 1 Statutes and Regulations • Flood Disaster Protection Act and Flood Insurance Act– Protection for borrowers and lenders • National Flood Insurance Reform Act of 1994 • Purpose • Requirements

Nat’l Flood Insurance Reform Act of 1994 • Requires flood insurance on all real property securing a loan if the property is in FHA. • Flood insurance required for the life of the loan • CU’s must escrow flood insurance premiums if other payments are being escrowed • Force-placement

Nat’l Flood Insurance Reform Act of 1994, Continued • Civil penalties on lenders in non-compliance • Cost of flood insurance determination can be passed on to borrower • Credit union must use a standard flood hazard determination form

Nat’l Flood Insurance Reform Act of 1994, Continued • Small loans are exempt • No federal flood emergency relief funds unless borrower has active FIP • Ceiling on coverage - $250,000 for residential, $100,000 for residential contents and $500,000 for non-residential contents

NCUA Regulation Part 760 • Flood hazard determination • Escrow requirements • Forced placement of flood insurance • Civil Money Penalties

NCUA’s Flood Insurance Regulations • Flood hazard determination – Whenever a loan is made, increased, renewed or extended • Credit unions are not required to perform prospective or retroactive reviews – Should be done • Standard Flood Hazard Determination Form • Use of previous determination – Seven years, done on standard form and no map changes

NCUA’s Flood Reg Continued • Use of third party determinations – Third party must guarantee accuracy • Insurance coverage – Outstanding loan principal or maximum coverage limits • Member notification of property in a designated flood area

NCUA’s Flood Reg Continued • Escrow requirement and exemption for commercial property loans • Requirements for forced placement of flood insurance • Notification of force placement and the 45-day response time • CMP’s - $385 per violation and a maximum of $130,000 in any calendar year – Apply even if the credit union sells the loan

Section 2Flood Insurance Basics • Flood insurance program’s two phases: • First phase triggered by a flood emergency • Second phase begins after a detailed study and requires a community to adopt and enforce a floodplain management ordinance • Failure to do so may result in probation and/or suspension • Probation – Written notice from FEMA • Suspension – Renders community non-participating

Property and Exemptions • What types of property are eligible for flood insurance? • Insurance coverage on multiple, eligible buildings • What types of property are ineligible for flood insurance? • What Property is exempt from flood insurance

Flood Insurance Requirements • First, determine whether subject property is in a flood hazard area and whether the community in which the property is located is a participant in the NFIP • Use of 3rd party determinations • Use of flood maps • Zone A – once every 100 years • Zone B – every 100 to 150 years • Zone C – minimal flood activity

Flood Zones Continued • Zone X – new designation to replace B and C • Zone D – possibility of flood has not been determined • Zone V – costal improved area in a 100 year area • Zone AR – flood protection system restoration areas • FEMA performs a review of the flood maps every 5 years • Participation in the NFIP

Map Changes by Letters • Property owners can ask FEMA to determine if a building is in a flood hazard area and to amend the map to reflect the determination • Letter of Map Amendment – Goes to Federal Insurance Administration and concerns elevations ( 60 days to respond) • Letter of map revision – Concerns changes to the land and costs $425 for a review (90 days to respond) • Letter of Determination Review – Credit unions and borrowers jointly contest a flood determination, costs $80 (45 day response)

Flood Determination Fees • Credit union or 3rd party may charge a “reasonable fee” for making the determination • Made in connection with making, increasing, extending or renewing a loan • Determination reflects a change by FEMA • Forced placement

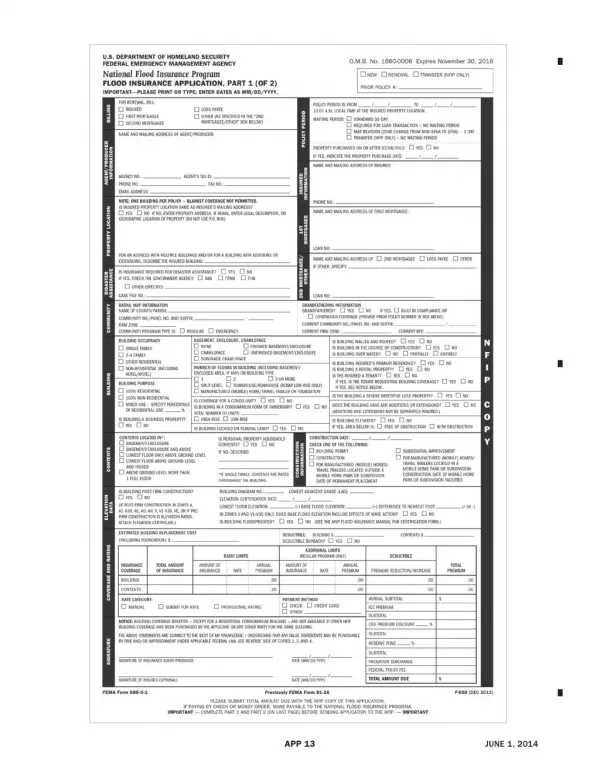

Standard Flood Hazard Determination Form • Form is used to determine if the property is in a flood area • Need the following information • Lender’s name and address • Property address • FEMA map community number, panel number, and flood zone • Is the community in a regular or emergency program • Information about flood insurance availability

Notice Requirements • Applies to improved property in flood hazard areas and includes the following: • Warning that building is in SFHA • Description of flood insurance purchase requirements • Statement that flood insurance is available under NFIP or from private insurers • Statement as to whether federal disaster relief assistance could be available • If flood insurance is required must notify the borrower within a reasonable period of time • NCUA recommends within 10 days

Loan Servicers • Credit unions must notify the flood insurance provider, within 60 days, of an change in servicer • FEMA requires credit unions to notify the flood insurance provider of the identity of the servicer when: • The credit union makes, increases, extends, renews, sells or transfers a covered loan • Must be done within 60 days from the date of the change

Section 3Credit Union Compliance • Credit unions must obtain evidence of flood insurance and must maintain insurance documentation • Evidence of flood insurance • Flood insurance application and receipt or check • FEMA proof-of-purchase certificate • For new purchasers, flood insurance is effective the day after payment • If no loan transaction is involved, flood insurance is effective in 30 days

Recordkeeping • FEMA and NCUA requirement • Necessary documentation: • Completed standard flood hazard determination • Copies of notices regarding community participation • Member’s written acknowledgement • Copy of flood insurance policy

Mortgage Portfolio Protection Program • Offered by Federal Insurance Administration • Applies to lenders who need to obtain flood insurance for properties in FHA in a participating community and after notice borrower has not obtained insurance • Also available to all lenders if they comply with certain guidelines • Intended to be used as a last resort • Can be canceled if borrower proves to the credit union that there is a current policy that was in effect before the date of the MPPP

Questions? Contact Information: Justin M. Anderson, Esq. NCUA, Office of General Counsel 703-518-6556 Janderson@ncua.gov