CHAPTER 8 FLOOD INSURANCE

150 likes | 260 Vues

This chapter covers essential information about flood insurance, focusing on the probabilities of flooding, community participation guidelines, and the National Flood Insurance Program (NFIP) structure. It explains the significance of Pre-FIRM and Post-FIRM properties in determining insurance costs and eligibility. The text tackles common myths about flood insurance and suggests incentives through the Community Rating System (CRS) to lower premiums. For personalized queries, contact your insurance agent or visit FloodSmart.gov for more resources.

CHAPTER 8 FLOOD INSURANCE

E N D

Presentation Transcript

Insurance Quiz - Flood Risk Probabilities • There is a % chance that a house will catch fire during the life of a 30-year mortgage. 5 • For a house located in a floodplain, there is a % chance that it will be inundated by a 100-year flood during the life of a 30-year mortgage…… 26 • Over a 50 year period, the probability increases to %. 39

Who Can Buy Flood Insurance? • Community Participation • All Zones

Community Participation • How does a community participate? • Application to FEMA • Meet minimum floodplain management requirements • 19,000+ communities participating • What does non-participation mean? • No flood insurance available • No disaster assistance • No federal mortgages in SFHA

Administrative Structure of the NFIP • Emergency Phase • Regular Phase

Eligible Structures • At least two rigid exterior walls and a roof • Principally above ground • Manufactured (mobile) home in SFHA, anchored to resist flotation, collapse or lateral movement.

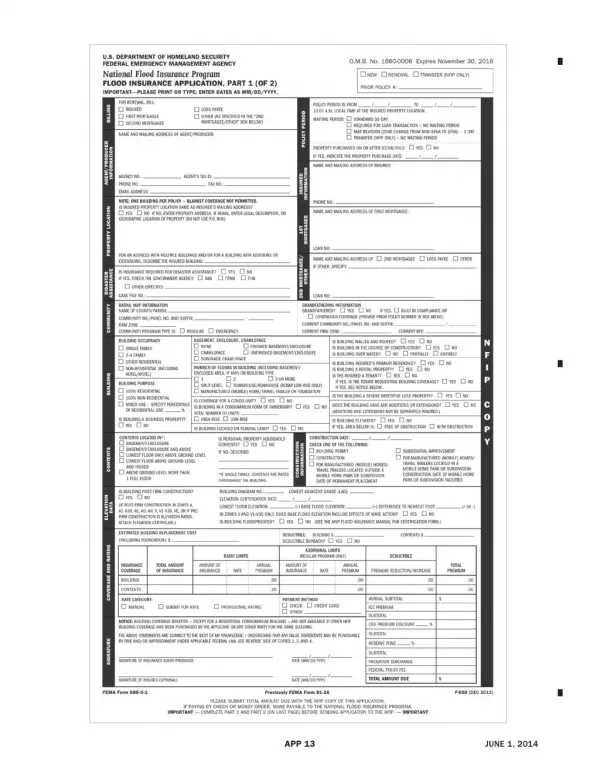

Pre-FIRM and Post-FIRM • The terms of Pre and Post FIRM are important to both FPM and rating buildings for insurance.

Comparison of Flood Insurance Existing Pre-FIRM House 1 FT ABOVE BFE 1 FT BELOW BFE 10 FT BELOW BFE $634/YR VS $634/YR VS $634/YR ($19,020) ($19,020) ($19,020) BASED ON $60,000 BLDG & $15,000 CONTENTS COVERAGE

Comparison of Flood Insurance Existing POST-FIRM House 1 FT ABOVE BFE 1 FT BELOW BFE 10 FT BELOW BFE $220/YR VS $930/YR VS $12,491/YR ($6,600) ($27,900) ($374,730) BASED ON $60,000 BLDG & $15,000 CONTENTS COVERAGE

Flood Insurance Costs for 30-Year Loan +1 FT Pre-FIRM House -1 FT -10 FT $634/YR VS $634/YR VS $634/YR ($19,020) ($19,020) ($19,020) +1 FT Post-FIRM House -1 FT -10 FT $220/YR VS $930/YR VS $12,491/YR($6,600) ($27,900) ($374,730)

EXPLODING THE MYTHS: • Flood Insurance does not cover basements. • You can only buy flood insurance in the floodplain. • Federal disaster assistance will cover your damages. • You can’t buy flood insurance during a flood. • Flood Insurance is only available from the government. “We Can’t Replace Your Memories ... But We Can Help You Build New Ones”

Community Rating System • Another way to reduce the cost of a flood policy!

Incentive CRS provides an incentive for communities to initiate new flood protection activities.

Class 9 8 7 6 5 4 3 2 1 Discount 5% 10% 15% 20% 25% 30% 35% 40% 45% CRS Premium Discounts • Points • 500-999 • 1000-1499 • 1500-1999 • 2000-2499 • 2500-2999 • 3000-3499 • 3500-3999 • 4000-4499 • 4500+

Flood Insurance Questions? • Specific insurance questions, contact your insurance agent or call 1-800-427-4661 • www.floodsmart.gov