Download

1 / 27

860 likes | 3.15k Vues

Macroeconomic Schools of Thought . ECON 101: Principles of economics Summer session I Appendix ch 24 + other sources. Philosophical Debates in Economics. Consider a riddle:

E N D

Macroeconomic Schools of Thought ECON 101: Principles of economics Summer session I Appendix ch 24 + other sources

Philosophical Debates in Economics Consider a riddle: “A man and his son are driving to a championship football game. It is late December and the roads are covered with snow. They hit a patch of ice and crash into a telephone pole. An ambulance rushes the son to a nearby hospital and operating room. The doctor walks in and says, “I can’t operate, that’s my son.” How could this be true?” Whatever your answer is, assume it is incorrect and come up with a second answer.

Why Economists Disagree A paradigm is a conceptual framework, a context for organizing thought. It is like a pair of theoretical spectacles used to observe and think about the world. There are competing paradigms for understanding the economy, competing frameworks for organizing economic theory. So why do these frameworks exist?

Two Competing Theories of Knowledge • Blank Slate Theory of Knowledge • The mind confronts the world directly • Individuals have experiences from which they generate ideas • You put your hand in a fire and generate the idea “hot” • You look at a rose and generate the idea “beautiful” • Your mind reflects the world as if it were a mirror • The world writes on you as if you were a blank slate

Two Competing Theories of Knowledge • Paradigmatic Theory of Knowledge • The mind never perceives the world directly or experiences sensations innocently, that is, untranslated, or unmediated by a person’s prior conceptual framework. • Everyone is wearing theoretical spectacles and thinking within some paradigm • What one sees is a product of what is “out there” and the lens used to study it.

Paradigmatic Theory of Knowledge From a paradigmatic perspective, observation and thinking are active rather than passive processes. Instead of reflecting what is “out there”, the observer partially constructs what she or he sees. In particular, paradigms influence thought in the way we attend to how we think about things (or in our case, the economy).

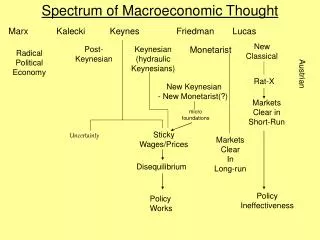

The starting point The term macroeconomics originated in the 1930s. The decade witnessed substantial progress in the study of aggregative economic questions. One theory and set of policy conclusions swept the field and became a new orthodoxy in macroeconomic policy questions. The book containing this theory was The General Theory of Employment, Interest and Money by John Maynard Keynes.

The starting point. This book started the Keynesian Revolution. But revolution against what? Keynesians called the old orthodoxy “classical economics” To study this emergence of Keynesian Theory, we need to study what was it that Keynes was against. To do this, we must study classical economics. But classical economics emerged as a revolution against a body of economic doctrines known as mercantilism.

Mercantilism I • Mercantilist thought was associated with the rise of the nation-state in Europe during the sixteenth and seventeenth century. • Two tenets of mercantilism were: • 1. Bullionism – A belief that the wealth and power of a nation were determined by its stock of precious metals. • 2. The belief in the need for state action to direct the development of the capitalist system.

Mercantilism II Adherence to bullionism led countries attempt to secure an excess of exports over imports to earn gold and silver through foreign trade. Methods use to achieve this: export subsidies, import duties, development of colonies to provide export markets. State action was believed to be necessary to cause the developing capitalist system to further the interests of the state (example: regulate trade, ban bullion exports)

Classical Economics I “Classical”—written on macroeconomic issues before 1936. More conventional terminology distinguishes between two periods in the development of economic theory before 1930. Classical – Adam Smith (Wealth of Nations, 1776), David Ricardo (1817), John Stuart Mill (1848) Neoclassical –Alfred Marshall (1920), A. C. Pigou (1933) Keynes lumped these two periods together as “classical”

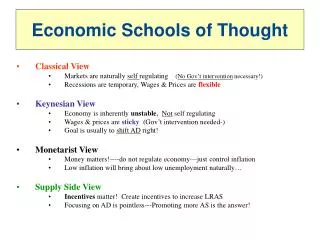

Classical Economics II Unlike the mercantilists, emphasized the importance of real factors in determining the wealth of nations. Stressed the optimizing tendencies of the free market in the absence of state control. Classical analysis was primarily real analysis: the growth of an economy was the result of increase stocks of the factors of production and advances in techniques of production.

Classical Economics III Money only played a role in facilitating transactions as a means of exchange (money had no intrinsic value) Most questions in economics could be answered without the role of money. Classical economists mistrusted the government and stressed the harmony of individual and national interests when the market was left unfettered by government regulations, except those necessary to ensure that the market remained competitive.

Classical Economics IV • In summary, two features of the classical analysis arose as part of the attack on mercantilism: • 1. Classical economics stressed the role of real as opposed to monetary factors in determining output and employment. Money had a role in the economy only as a medium of exchange. • 2. Classical economics stressed the self-adjusting tendencies of the economy. Government policies to ensure an adequate demand for output were considered unnecessary and generally harmful.

Keynesian I Keynesian Economics developed against the background of the Great Depression of the 1930s. Unemployment in 1929 (3.2%), 1933 (25%) Keynes, a British economist, was heavily influenced by events in his own countries than those in the US. High unemployment in the US caused a debate, led by Keynes.

Keynesian II Keynes thought that high unemployment in industrialized countries was the result of a deficiency in aggregate demand. Keynes’s theory provided the basis of economic policies to combat unemployment by stimulating aggregate demand. Before, classical economists recognized the human cost of unemployment but never had anything to say about the causes of unemployment.

Keynesian III Keynes warned that pessimistic expectations could precipitate downward spirals in the economy Sticky prices!

Monetarist I Monetarist Model developed in 1940s by Milton Friedman, Nobel Prize in Economics 1976, University of Chicago. Argued that the Keynesian approach overstates the amount of macroeconomic instability in the economy. Argued that most fluctuations in real output were caused by fluctuations in the money supply, rather than by fluctuations in consumption or investment spending.

Monetarist II Friedman argued that the severity of the Great Depression was caused by the Fed’s allowing the quantity of money in the economy to fall by more than 25%. Friedman argued that the Fed should adopt a monetary growth rule, which is a plan for increasing the quantity of money at a fixed rate. This will reduce fluctuations in real GDP, employment and inflation.

Monetarist III Friedman’s monetarist ideas attracted significant support during the 1970s and early 1980s, when the economy experience high rates of unemployment and inflation. Support declined during late 1980s and 1990s when the unemployment and inflation rate were relatively low.

New Classical I Mid 1970s: Robert Lucas, Thomas Sargent, Robert Barro. Similar thinking to the classical economists from before the Keynesian Revolution. One additional argument: rational expectations.

New Classical II Rational expectations –households (workers) and firms form expectations of the future values of economic variables (inflation rate) by making use of all available information. If actual inflation rate is lower than expected inflation rate, the actual real wage will be higher than expected real wage. Higher real wages will lead to a recession because firms will hire fewer workers and cut back on production. As workers adjust their expectations to the lower inflation rate, real wage will decline, employment and production will expand, bringing the economy out of recession.

New Classical III Agree with monetarists: Fed should adopt a monetary growth rule. They argue that a monetary growth rule will make it easier for workers and firms to accurately forecast the price level, thereby reducing fluctuations in real GDP.

Real Business Cycle I 1980s: Finn Kydland, Edward Prescott Agree with New Classicals: workers and firms form their expectations rationally but were wrong about fluctuations in real GDP Fluctuations in real GDP are caused by temporary shocks to productivity.

Real Business Cycle II These shocks can be negative (decline in the availability of oil or other raw materials) or positive (technological change that makes it possible to produce more output with same inputs) Model focuses on “real” factors (productivity shocks) rather than changes in the quantity of money.

Back to the riddle…. • Generally there are two sets of answers. • Most people give answers like • 1) The doctor is very confused; 2) The boy was messed up beyond recognition • 1) The doctor gave his sperm to a sperm bank and the boy was fathered from the bank; 2) The doctor was God • 1) Boy’s dead father was adoptive father; 2) Father in car was Catholic priest

Back to the riddle… The second set of answers includes the possibility that the doctor is the boy’s mother. There is no reason to assume that this is the case, but the interesting thing about the riddle is the degree to which traditional gender stereotypes prevent some people from even considering the possibility. Such is the power of paradigms: they assert themselves before you think and before you “see” To some extent, they even think and see for you.