Download

1 / 32

320 likes | 538 Vues

14-1 Nominal versus Real Interest Rates. Interest Rates expressed in terms of dollars (or, more generally, in units of the national currency) are called nominal interest rates . Interest rates expressed in terms of a basket of goods are called real interest rates.

E N D

14-1 Nominal versus Real Interest Rates • Interest Rates expressed in terms of dollars (or, more generally, in units of the national currency) are called nominal interest rates. • Interest rates expressed in terms of a basket of goods are called real interest rates.

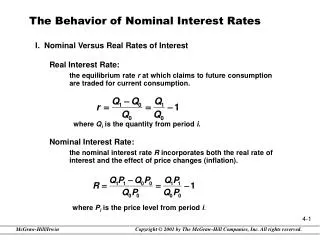

14-1 Nominal versus Real Interest Rates Figure 14 - 1 Definition and Derivation of the Real Interest Rate it = nominal interest rate for year t. rt = real interest rate for year t. (1+ it): Lending one dollar this year yields (1+ it) dollars next year. Alternatively, borrowing one dollar this year implies paying back (1+ it) dollars next year. Pt = price this year. Pet+1= expected price next year.

14-1 Nominal versus Real Interest Rates • then, the expected rate of inflation equals Given , and knowing that Consequently, If the nominal interest rate and the expected rate of inflation are not too large, a simpler expression is: The real interest rate is (approximately) equal to the nominal interest rate minus the expected rate of inflation.

14-1 Nominal versus Real Interest Rates • Here are some of the implications of the relation above: • If • If • if

14-1 Nominal versus Real Interest Rates Figure 14 - 2 Nominal and Real One-Year T-bill Rates in the United States since 1978 Nominal and Real Interest Rates in the United States since 1978 Although the nominal interest rate has declined considerably since the early 1980s, the real interest rate was actually higher in 2006 than in 1981.

14-2 Nominal and Real Interest Rates and the IS–LM Model • When deciding how much investment to undertake, firms care about real interest rates. Then, the IS relation must read: • The interest rate directly affected by monetary policy—the one that enters the LM relation—is the nominal interest rate, then: The real interest rate is:

14-2 Nominal and Real Interest Rates and the IS–LM Model Note an immediate implication of these three relations: • The interest rate directly affected by monetary policy is the nominal interest rate. • The interest rate that affects spending and output is the real interest rate. • So, the effects of monetary policy on output depend on how movements in the nominal interest rate translate into movements in the real interest rate.

14-3 Money Growth, Inflation, and Nominaland Real Interest Rates • This section focuses on the following assertions: • Higher money growth leads to lower nominal interest rates in the short run, but to higher nominal interest rates in the medium run. • Higher money growth leads to lower real interest rates in the short run, but has no effect on real interest rates in the medium run.

14-3 Money Growth, Inflation, and Nominaland Real Interest Rates Revisiting the IS–LM Model • Reducing the IS relation, LM relation and relation between the real and nominal interest rate gives us: • IS • LM • The IS curve is still downward sloping. • The LM curve is upward sloping. • The equilibrium is at the intersection of the IS curve and the LM curve.

14-3 Money Growth, Inflation, and Nominaland Real Interest Rates Figure 14 - 3 Equilibrium Output and Interest Rates Revisiting the IS–LM Model The equilibrium level of output and the equilibrium nominal interest rate are given by the intersection of the IS curve and the LM curve. The real interest rate equals the nominal interest rate minus expected inflation.

14-3 Money Growth, Inflation, and Nominaland Real Interest Rates Figure 14 - 4 The Short-Run Effects of an Increase in Money Growth Nominal and Real Interest Rates in the Short Run An increase in money growth increases the real money stock in the short run. This increase in real money leads to an increase in output and decreases in both the nominal and real interest rates.

14-3 Money Growth, Inflation, and Nominaland Real Interest Rates Nominal and Real Interest Rates in the Medium Run • In the medium run, output returns to the natural level of output, . • In the medium run, the rate of inflation is equal to the rate of money growth minus the rate of growth of output.

14-3 Money Growth, Inflation, and Nominaland Real Interest Rates Nominal and Real Interest Rates in the Medium Run • In the medium run, the nominal interest rate increases one for one with inflation. This result is known as the Fisher effect, or the Fisher Hypothesis. For example, an increase in nominal money growth of 10% is eventually reflected by a 10% increase in the rate of inflation, a 10% increase in the nominal interest rate, and no change in the real interest rate.

14-3 Money Growth, Inflation, and Nominaland Real Interest Rates From the Short Run to the Medium Run • In the short run, lower nominal interest rates lead to higher output and inflation. In the medium run, this situation changes. • In the short run, • Over time, • In the medium run,

14-3 Money Growth, Inflation, and Nominaland Real Interest Rates From the Short Run to the Medium Run • In words: • So long as the real interest rate is below the natural real interest rate, output is higher than the natural level of output, and unemployment is below its natural rate. • From the Phillips curve relation, we know that as long as unemployment is below the natural rate of unemployment, inflation increases. • As inflation increases, it becomes higher than nominal money growth, leading to negative real money growth. • In the medium run, the real interest rate increases back to it initial value.

14-3 Money Growth, Inflation, and Nominaland Real Interest Rates Figure 14 - 5 The Adjustment of the Real and the Nominal Interest Rates to an Increase in Money Growth From the Short Run to the Medium Run An increase in money growth leads initially to decreases in both the real and the nominal interest rates. Over time, however, the real interest rate returns to its initial value, and the nominal interest rate converges to a new higher value, equal to the initial value plus the increase in money growth.

14-3 Money Growth, Inflation, and Nominaland Real Interest Rates Evidence on the Fisher Hypothesis • To see if increases in inflation lead to one-for-one increases in nominal interest rates, economists look at: • Nominal interest rates and inflation across countries. The evidence of the early 1990s finds substantial support for the Fisher hypothesis. • Swings in inflation, which should eventually be reflected in similar swings in the nominal interest rate. Again, the data appears to fit the hypothesis quite well.

Nominal Interest Rates and Inflation across Latin America in the Early 1990s Figure 1 Nominal Interest Rates and Inflation in Latin America, 1992 to 1993

14-3 Money Growth, Inflation, and Nominaland Real Interest Rates Figure 14 - 6 The Three-Month Treasury Bill Rate and Inflation since 1927 Evidence on the Fisher Hypothesis The increase in inflation from the early 1960s to the early 1980s was associated with an increase in the nominal interest rate. The decrease in inflation since the mid-1980s has been associated with a decrease in the nominal interest rate.

14-3 Money Growth, Inflation, and Nominaland Real Interest Rates Evidence on the Fisher Hypothesis • Figure 14-6 has at least three interesting features: • The steady increase in inflation from the early 1960s to the early 1980s was associated with a roughly parallel increase in the nominal interest rate. • The nominal interest rate lagged behind the increase in inflation in the 1970s, while the disinflation of the early 1980s was associated with an initial increase in the nominal interest rate. • The other episode of inflation underscores the importance of the “medium-run” qualifier in the Fisher hypothesis.

14-4 Expected Present Discounted Values Interest Rates Figure 14 - 7 Computing Present Discounted Values The expected present discounted value of a sequence of future payments is the value today of this expected sequence of payments. Computing Expected Present Discounted Values

(a) One dollar this year is worth 1+it dollars next year. (b) If you lend/borrow 1/(1+it) dollars this year, you will receive/repaydollar next year. 14-4 Expected Present Discounted Values Interest Rates Computing Expected Present Discounted Values (c) One dollar is worth dollars two years from now. (d) The present discounted value of a dollar two years from today is equal to .

The word “discounted” comes from the fact that the value next year is discounted, with (1+it) being the discount factor. The 1-year nominal interest rate, it, is sometimes called the discount rate. 14-4 Expected Present Discounted Values Interest Rates Computing Expected Present Discounted Values

The present discounted value of a sequence of payments, or value in today’s dollars equals: When future payments or interest rates are uncertain, then: Present discounted value, or present value are another way of saying “”expected present discounted value.” 14-4 Expected Present Discounted Values Interest Rates Computing Expected Present Discounted Values The General Formula

This formula has these implications: Present value depends positively on today’s actual payment and expected future payments. Present value depends negatively on current and expected future interest rates. 14-4 Expected Present Discounted Values Interest Rates Using Present Values: Examples

14-4 Expected Present Discounted Values Interest Rates Using Present Values: Examples • To focus on the effects of the sequence of payments on the present value, assume that interest rates are expected to be constant over time, then: Constant Interest Rates Constant Interest Rates and Payments When the sequence of payments is equal—called them $z, the present value formula simplifies to:

The terms in the expression in brackets represent a geometric series. Computing the sum of the series, we get: 14-4 Expected Present Discounted Values Interest Rates Using Present Values: Examples Constant Interest Rates and Payments

Assuming that payments start next year and go on forever, then: Using the property of geometric sums, the present value formula above is: 14-4 Expected Present Discounted Values Interest Rates Using Present Values: Examples Constant Interest Rates and Payments, Forever Which simplifies to:

14-4 Expected Present Discounted Values Interest Rates Using Present Values: Examples Zero Interest Rates If i = 0, then 1/(1+i) equals one, and so does (1/(1+i)n) for any power n. For that reason, the present discounted value of a sequence of expected payments is just the sum of those expected payments.

Replacing nominal interest with real interest rates to obtain the present value of a sequence of real payments, we get: 14-4 Expected Present Discounted Values Interest Rates Nominal versus Real Interest Rates and Present Values Which can be simplified to:

Key Terms • nominal interest rate • real interest rate • Fisher effect, Fisher hypothesis, • expected present value • discount factor • discount rate • present discounted value • present value