Download

1 / 6

70 likes | 262 Vues

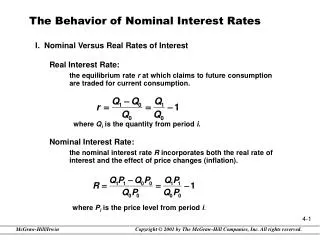

I. Nominal Versus Real Rates of Interest Real Interest Rate: the equilibrium rate r at which claims to future consumption are traded for current consumption. where Q i is the quantity from period i . Nominal Interest Rate:

E N D

I. Nominal Versus Real Rates of Interest • Real Interest Rate: the equilibrium rate r at which claims to future consumption are traded for current consumption. where Qi is the quantity from period i. • Nominal Interest Rate: the nominal interest rate R incorporates both the real rate of interest and the effect of price changes (inflation). The Behavior of Nominal Interest Rates where Pi is the price level from period i.

One-period inflation rate: • Combining expressions: • Solving for the real rate:

II. Expected Inflation and Nominal Interest Rates • Fisher reasoned that in competitive markets, rational individuals would want to maintain purchasing power by demanding rates of interest that incorporate anticipated price increases. • Expected rates are before-the-fact (ex ante) predictions of future rates. • Actual rates reflect after-the-fact (ex post) calculations. • Fisher’s nominal interest rate: or an approximation, Nominal interest rate = Anticipated real interest rate + Expected inflation rate

Problems with the nominal theory of interest rates: • real interest rates and inflation are not observable and must therefore be predicted • how should inflation be determined • very difficult to test • not based upon theoretical models • Mundell Effect: • Inflation reduces wealth. Attempts at saving to restore wealth cause a downward pressure on interest rates. This results in a less than one-to-one adjustment in nominal rates for changes in expected inflation. • Darby Effect: • Taxes on nominal returns result in a demand to be compensated. This causes a greater than one-to-one adjustment in nominal rates for changes in expected inflation.

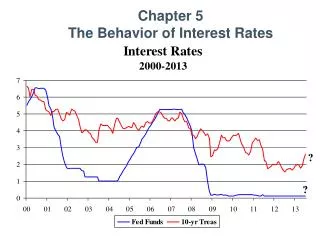

III. Empirical Evidence Regarding Inflation and Nominal Interest Rates • Insert 4.1 • Expected Real Rate and Inflation Proxies • Past inflation rates as predictors • Survey data on inflationary expectations • Long vs. short-term interest rates • Inflation indexed bonds • Commodity-linked bonds • Extracting Estimates from Theoretical Models • Macroeconomic models • Aggregate money supply and demand models • Other Problems in Testing • Which inflation rate? • Logical tautologies • Non constant real rate of interest • IV. Evidence From Several Countries • Insert 4.2 & 4.3 • The positive relationship between nominal interest rates and inflationary expectations.

V. Index Bonds as a Solution to Fisher’s Problem • What are they? • How do they work? • VI. Where Does This Lead Us? • The effect of inflation on nominal interest rates seems clear but imprecise. What is the implication of this for investors? • Question: Suppose you were planning for retirement at some • distant point in the future. What are your choices; what are your • expectations; and what are the risks? VII. Summary • The distinction between nominal and real interest rates was developed. • Financial investments generally carry nominal rates of return • Changes in nominal interest rates may not keep pace with changes in expected inflation because of forecasting errors, wealth effects, and tax repercussions.