Download

1 / 12

120 likes | 373 Vues

Generalised Mean Variance Analysis and Robust Portfolio Construction February 2006 Steve Wright Tel 44 20 7568 1874. Business Context. Institutional fund management Low frequency noisy non stationary data Dominance of subjective analysis

E N D

Generalised Mean Variance Analysis and Robust Portfolio Construction February 2006 Steve Wright Tel 44 20 7568 1874

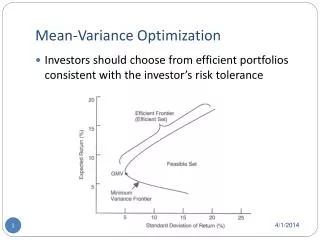

Business Context • Institutional fund management • Low frequency noisy non stationary data • Dominance of subjective analysis • Regulatory and client pressure for accountability. • Interactive tools add structure to the process • Mean Variance Analysis for portfolio diversification • Widely accepted theory • With practical problems • Recommendations are sensitive to small changes in user inputs • Out of sample performance of the risk models can be an issue • Hence portfolio churn and lack of confidence in the process • A robust extension of Mean Variance analysis

The investment process can be complex Strategy GlobalValuation Economics Research Analysts Third Party Data Providers Company Database Sector Preferences Regional Preferences Style Preferences Asset class Preferences Company preferences Mandates and Constraints Ex post statistics Portfolio Construction Ex ante statistics Risk & Return modelling Transaction cost control (Portfolio)Trading Futures Markets FX Markets Debt Markets Returns

An ideal investment process • Mutually consistent across portfolios (more risk = more equity) • Simple and understandable by an intelligent non specialist. • Stable enough to avoid generating excessive volume of trades. • Reliable enough to have acceptable out of sample behaviour. • Capable of reflecting all likely practical operating constraints • Transparent enough to be monitored easily • A starting point for discussion of the key issues

Is risk volatility or lack of diversification Minimum Risk Maximum Return Standard MV Optimisation Minimum Risk Maximum Return Rank Optimisation

Conclusions • Forecast and portfolio construction is not an exact science. It is an art with no black and white answers. An interactive tools allow you to get a feel for these uncertainties. • Probability based methods can improve your forecast construction by bringing statistical rigour to qualitative analysis and making the results of quantitative analysis more intuitive and realistic. • We cannot eliminate risk, but we can improve the stability, reliability and relevance of the measures used