Download

1 / 5

170 likes | 849 Vues

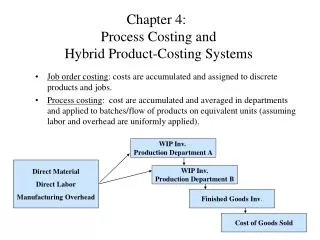

Chapter 4: Process Costing and Hybrid Product-Costing Systems. Job order costing : costs are accumulated and assigned to discrete products and jobs.

E N D

Chapter 4: Process Costing and Hybrid Product-Costing Systems • Job order costing: costs are accumulated and assigned to discrete products and jobs. • Process costing: cost are accumulated and averaged in departments and applied to batches/flow of products on equivalent units (assuming labor and overhead are uniformly applied). WIP Inv. Production Department A Direct Material Direct Labor Manufacturing Overhead WIP Inv. Production Department B Finished Goods Inv. Cost of Goods Sold

More Process Costing Definitions • Equivalent Units: a measure of the amount or production effort applied to a physical unit of production. For example, if there are 100 units that are 75% complete, there are 750 equivalent fully complete units. • Transferred-in Costs: costs that are assigned to in-process parts that are transferred from one production department to another. • Weighted -Average Method: method of process costing where the costs assigned to the beginning WIP inventory are added to the current period production costs. The cost per equivalent unit is a weighted average of the beginning WIP and the current cost.

Direct Materials: Flour Eggs Sugar Sprinkles Direct Labor and MOHA are applied uniformly throughout cookie making process. Cookie making is performed in a single stage production facility (Bala’s kitchen). DM transferred in at 0% completion for Batter/Baking QC to remove burnt, broken, and malformed cookies is performed at 30% completion. Taste samples are also taken form this 30% Additional DM added at 40% complete to enhance taste and physical characteristics of cookie. Additional DM added at 80% complete for decoration. Process Costing at Bala’s Cookie Factory Batter/Baking (0% Stage) DM Input (80% of DM) Flour Eggs Sugar QC (30% Stage) Defect rate = 1% Icing (40% Stage) DM Input (10% DM) Sugar Decoration (80% Stage) DM Input (10% DM) Sprinkles COOKIES FOR D39, Section 69!

Weighted Average Method of Process Costing Steps to Prepare Departmental Production Report • Step 1: Analysis of Physical Flow of Units (Physical units in beginning work in process) + (Physical units started) - (Physical units completed and transferred out) Physical units in ending work in process. • Step 2:Calculation of Equivalent Units (Eq. units of activity in units completed/transferred out) + (Eq. Units of activity in ending work in process) Total equivalent units of activity

Weighted Average Method of Process Costing Steps to Prepare Departmental Production Report • Step 3: Computation of Unit Costs Work in process + Costs incurred during March Total costs to account for Total costs to account for = Cost per equivalent unit Equivalent Units • Step 4: Analysis of Total Costs Calculate cost of goods complete and transferred out of department. Calculate costs remaining in WIP and then the conversion.