Download

1 / 14

140 likes | 313 Vues

Income Statement Review. Income Statement Basics. Income statement explains changes in retained earnings: RE YE ’02 = RE YE ‘01 + NI In ‘02 - Dividends In ’02 Net Income In ‘02 = Revenue In ‘02 - Expense In ‘02. Retained Earnings is a permanent account

E N D

Income Statement Basics Income statement explains changes in retained earnings: REYE ’02= REYE ‘01 + NIIn ‘02 - DividendsIn ’02 Net IncomeIn ‘02 = RevenueIn ‘02 - ExpenseIn ‘02

Retained Earnings is a permanent account • Net Income, Revenues and Expenses are temporary accounts • get folded into retained earnings at period-end • keep track of net income during the period • begin and end the period with zero balances

Net Income and Cash Flows • Over a long enough period net income = cash from operations + cash from investing • Therefore, the only issue is timing

Revenue recognition • Have performed all (or a substantial portion) of your service • Have received an asset (e.g., cash or receivable) which can be measured • Amount is adjusted up front for bad debts, sales discounts and allowances, etc. • Most common source of fraud

Expense recognition • Generally involves transforming an asset (stock) to an expense (flow) • Match to revenue if possible (e.g., product cost) • Merchandising--cost of acquiring inventory • Manufacturing--cost of making product (including overhead)

Otherwise charge to expense as consumed (e.g., SG&A and R&D) • Measured on same basis as the asset being expensed.

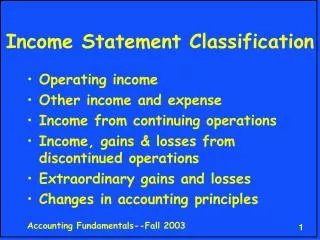

Income Statement Format Sales - Cost of Goods Sold Gross Profit - Selling, General and Administrative Expense Operating Income +/- Interest Expense/Income +/- Other Income, Gains, Expenses, Losses, etc. Pre-Tax Income from Continuing Operations - Income Tax Expense Net Income from Continuing Operations

+/- Income/Loss from Operations of Businesses Sold (net of income tax) +/- Gain/Loss on Business Sold (net of income tax) Income from Discontinued Operations +/- Extraordinary Gains/Losses (net of income tax) +/- Cumulative Effect of Accounting Change NET INCOME

Earnings Per Share • Basic EPS = Net Income to Common / Ave. Number of Common Shares Outstanding • For Coke, $3,050M Net Income / 2,478M Common Shares = $1.23 • Diluted EPS takes into account securities convertible into stock (e.g., stock options)