PROFIT THEORY

This course companion explores the nuances of profit theory in economics, highlighting how economists' measurement of profit differs from that of accountants, particularly regarding opportunity cost. It explains the concepts of total profit, normal profit, abnormal profit, and losses, using examples to illustrate the implications of revenue exceeding, equating, or falling short of total costs. The practical application of these concepts helps entrepreneurs understand their financial situations better, enabling informed decisions on business viability and future ventures.

PROFIT THEORY

E N D

Presentation Transcript

PROFIT THEORY IB ECONOMICS – A COURSE COMPANION (Blink & Dorton, 2007)

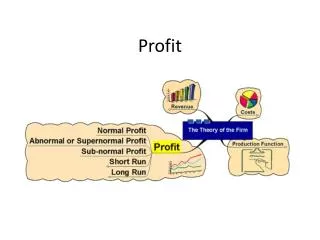

PROFIT THEORY • How economist’s measure profit is different to accountants, because of the issue of opportunity cost. • For example, a person might be making $80,000 a year profit from running their business, but they were making $80,000 a year as marketing manager before they started to run their own business. Running a business may involve more stress, and higher levels of uncertainty.

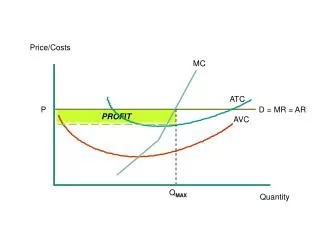

PROFIT THEORY How do economists measure profit? Total Profit = Total revenue – total cost (fixed, variable and opportunity cost)

PROFIT THEORY Normal Profit • If total revenue is equal to total cost, the firm is making normal profit. Abnormal Profit • If total revenue is greaterthan the total cost, the firm is making abnormal profit. Losses • If total revenue is less than total cost, then the firm is making losses.

Table Analysis – Firm A • A firm is making an abnormal profit of $20,000. • This means that the revenue earned by the firm is not only covering all the costs, but it is in fact $20,000 more. • This will make the entrepreneur happy, as he/she was expecting to cover her opportunity cost of $60,000 and in fact gets $80,000.

Table Analysis – Firm B • Firm B is making normal profit. • The revenue earned by the firm exactly covers all the costs. • The entrepreneur will be satisfied.

Table Analysis – Firm C • Firm C is making losses. • Although an accountant would say that the firm is making a profit of $40,000 ($200,000-$160,000) the entrepreneur will not be happy. • Fixed and variable costs are covered, but opportunity cost is not covered. • The entrepreneur should close down the firm, moving to the entrepreneur’s next best occupation.