Download

1 / 16

160 likes | 207 Vues

Explore the intersection of risk, profit, and utility theory in corporate finance to maximize wealth. Understand the Fundamental Theorem of Corporate Finance, objections to traditional methods, risk-adjusted discounting, implications of present-value coordinates, and foibles of capital allocation.

E N D

Risk, Profit, and Utility Theory Leigh J. Halliwell, FCAS, MAAA leigh@lhalliwell.com CAS Ratemaking Seminar Atlanta, GA March 7, 2007

Fundamental Theorem of Corporate Finance • “To calculate present value [of a project], we discount expected payoffs by the rate of return offered by the equivalent investment alternative in the capital market. The rate of return is often referred to as the discount rate, hurdle rate, or opportunity cost of capital” [Brealey and Myers, 2002, p. 15] • Simple, two-ingredient recipe: • 1: deterministic “expected payoffs” • 2: rate of return (time-1) Odd, actuarial science going stochastic, corporate finance staunchly deterministic.

Objections to this Theorem • 1: Can one real number (discount rate r) capture all the information lost when reducing a joint-probabilistic project to its expected value? (True, 10 1, but not by a smooth mapping.) Who calculates this r? Is it gleaned from “the market?” What is this market, that can provide an answer that has not been worked out in someone’s mind? Truth: The market is only a collection of persons, some making the best decisions possible, the rest operating rather passively on “expert advice” and herd instinct. (Cf. slide 12 “epiphenomenon”)

Objections to this Theorem (Cont’d) • 2: “Equivalent investment alternative” implies betas and stock market returns. Are stock returns more fundamental than projects? Have we put the cart before the horse? “The stock investor puts money not into a project, but into a corporation whose employees will put money into projects.” [Halliwell, 2003, p. 34] • 3: Projects of zero-expected payoff: 0(1+r)t = 0. • 4: Instantaneous projects: x(1+r)0 = x, no discount • 5: Reversed cash flows (in, then out): negative equity risk premium, or conversion to equity flows (i.e., capital allocation).

Even Stewart Myers Objects • “Since time and risk are logically separate variables, summing up their effects in [the discount rate] requires a particular assumption about [their] actual relationship.” • “The rate at which income is expected to be realized … depends on the rate at which uncertainty is expected to be resolved … If uncertainty is expected to be resolved at a constant rate over time, then [risk-adjusted discounting] predicts accurately. But this need not always be the case.” • “… the certainty-equivalent framework [versus risk-adjusted discounting] is applicable in a wider variety of situations.” [Robichek and Myers, 1966, pp. 727, 730, 728. Similarly Philbrick 1994]

Risk and Certainty Equivalence • 1. “… time and risk are logically separate variables.” • 2. Risk Theory should return to the birthplace of probability theory, viz., Pascal, Fermat, and gambling problems (1650s). • 3. Challenge to corporate finance: Set margins for casino games, e.g., Roulette. Are ‘0’ and ’00’ a sufficient house advantage (20:18 odds for even money)? ROE, capital allocation, and risk-adjusted discounting for the roulette wheel? Or are these zero-beta events and deserving of no expected profit? Should fair casinos take ‘0’ and ’00’ off the wheel? • 4. Insurance is like gambling, not like banking. • 5. Start with certainty: present value coordinates (next slide)

Implications of Present-Value Coordinates • Present value is a random variable, not a real number. • Ten blue dots represent possible outcomes (at t years, x dollars). • The value of this stochastic cash flow should lie between 75 and 100. If all points lay on the same isobar, the value would be that of the isobar. Risk-adjusted discounting can break out of the envelope. • Objection: What if the coordinate system changes? False dynamism; ruins 100%-certain events too. • If two PV random variables are (almost surely) equal, then they must have the same value. In symbols: Prob{PV[X] =PV[Y]} = 1 Value[X] =Value[Y] • PVs of outcomes are like sufficient statistics. Negative PVs as legitimate as positive; solvency and bankruptcy are constraints, not criteria (cf. slide 12 “constraints”). “Economics is the study of … maximization subject to constraints.” A. K. Dixit, Optimization in Economic Theory, 2nd ed., Oxford University Press, 1990, p. 1.

Foibles of Capital Allocation • Capital (a fancy name for wealth or money) does not work, despite advertising slogans. • Would capital allocated to a one-year hurricane treaty work off season (Dec-May)? Can we make capital moonlight? Some try to have it both ways (claiming capital to be “committed” and seeking to make it moonlight). • Capital allocation inevitably confuses rate of return (% per year, i.e., time-1) with return (%). • Example of short-lived exposure: 13% per year is 0.25% per week • Better to speak of “risk and expected profit” than of “risk and return.” The dollar, not year-1, is the meaningful unit.

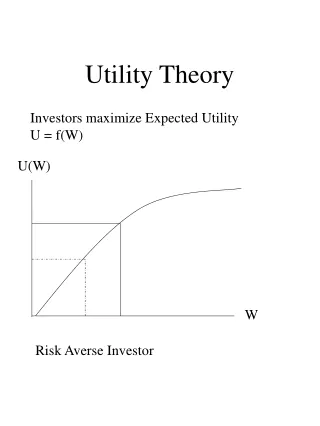

Question: Which Wealth is Better, $550 ± 50 or $600 ± 100? Answer: Which is greater, E[u(W1)] or E[u(W2 )]?

Ordering Projects by Expected Utility • Current stochastic wealth W Project has present value X and cost q. Wealth with project is W+X-q; W and X jointly distributed. Compare E[u(W+X-q)] with E[u(W)]. • Borch’s insurance formulation, W-L+p, equivalent • Instantaneous formulation Value=H[X] frequent in our actuarial literature. (e.g., Bühlmann 1980; Gerber 1979, Ch 5) Some are so future-oriented that they must displace instantaneous results to the end of an accounting period (with interest)! Why is a future time better than the present? Is an instantaneous problem illegitimate? Why continue to speak of “marginal utility,” if utility theory is no good?

New Perspective:How much to buy at a given price? • Comparing E[u(W+X-q)] with E[u(W)] can give you only a ceiling price (for one unit of X), not the appropriate price. • An economic agent should be free to choose how much of X to purchase at unit price q. Cash flows are scaleable. • New objective: Maximize f(q)=E[u(W+qX-qq)]. State-price form at maximum: q=E[YX], where E[Y] = 1 [Panjer, 1998, §11.2.4]. • “Fundamental Theorem” of Halliwell [2003, Appendix B]: For a given q, f(q) has one and only one maximum. The curve looks like an upside-down parabola. • Two or more agents together find the unique price q at which each maximizes its expected utility and all of X clears. If not disturbed by constraints, this is a Pareto optimum. • The agents constitute a market, but each agent is entitled to its own beliefs. The market is an epiphenomenon. Excel examples at www.casact.org/sections/care/0905/index.cfm?fa=sessions

Linear-Exponential Utility • Just about the only game in town, as argued by Hans Gerber [1979, Ch. 5] and in Halliwell [2003, Appendix C]. Has two desirable properties (a. and b. below) • Some argue for power-curve [or logarithmic] utility and relative risk aversion (RRA). Cf. Gerber and Pafumi [1998, 76]. • RRA appropriate for bundles of physical goods, e.g., apples and oranges, which come in non-negative amounts. • Stochastic cash flows deal with one good (cash/money) in random outcomes that can be positive or negative. As scaleable, negative amounts are as legitimate as positive. a. Linear-exponential utility is defined for all real numbers, unlike other common utilities (power/log, quadratic) • Only linear-exponential utility allows an X independent of W to be valued by itself. Otherwise, one would have to know everything in order to value anything. Linear-exponential utility has absolute risk aversion (ARA).

Bibliography • Borch, Karl H., “The Utility Concept Applied to the Theory of Insurance,” ASTIN Bulletin, 1(5), 1961, 245-255. • Bowers, N. L., Gerber, H. U., Hickman, J. C., Jones, D. A., and Nesbitt, C. J., Actuarial Mathematics, Society of Actuaries, 1986. • Brealey, Richard A., and Myers, Stewart C., Principles of Corporate Finance, Seventh Edition, New York, McGraw-Hill, 2002. • Bühlmann, Hans, “An Economic Premium Principle,” ASTIN Bulletin, 11(1), 1980, 52-60. • Gerber, Hans U., An Introduction to Mathematical Risk Theory, Philadelphia, S. S. Huebner Foundation, 1979. • Gerber, Hans U., and Pafumi, Gérard, “Utility Functions: From Risk Theory To Finance,” North American Actuarial Journal, Volume 2 (July 1998), 74-100 • Halliwell, Leigh J. “The Valuation of Stochastic Cash Flows,” CAS Forum (Reinsurance Call Papers, Spring 2003), 1-68. • “Valuing Stochastic Cash Flows: A Thought Experiment,” CAS Forum (Winter 2004), 291-294. • “Utility-Theoretic Underwriting,” www.casact.org/education/care/0905/handouts/ halliwell.pdf • Panjer, Harry H., editor, Financial Economics: with Applications to Investments, Insurance and Pensions, Schaumburg, IL, Actuarial Foundation, 1998. • Philbrick, Stephen W., “Accounting for Risk Margins,” CAS Forum (Spring 1994), 1-87 • Robichek, Alexander A., and Myers, Stewart C., “Conceptual Problems in the Use of Risk-Adjusted Discount Rates,” Journal of Finance, Vol. 21, No. 4 (Dec 1966), 727-730.