Download

1 / 64

640 likes | 868 Vues

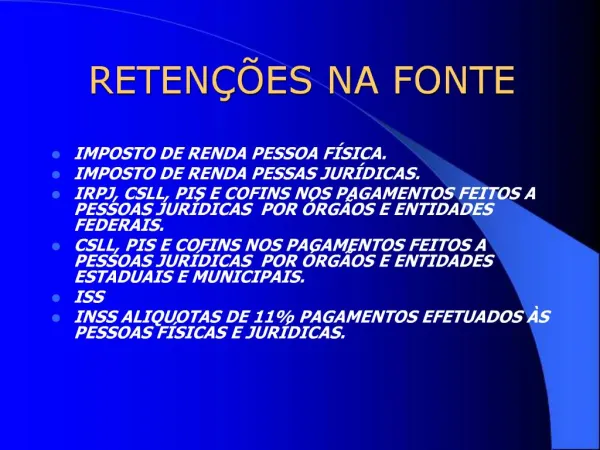

. (1)IRRFIMPOSTO DE RENDA NA FONTE BENEFICIRIOPESSOA JURDICA. 1.1 PRESTAO DE SERVIOS DE NATUREZA PROFISSIONAL. Esto sujeitos ao IRRF, de 1,5% a partir de 1994, as importncias pagas ou creditadas por PJ outras PJ, pela prestao de servios caracterizadamente de natureza profissional.

E N D

1. IRRF - IMPOSTO DE RENDA NA FONTE e CSRF � CONTRIBUI��ES SOCIAIS RETIDAS NA FONTE BENEFICI�RIOS PESSOA JUR�DICA IRRF - Servi�os Profissionais Decreto 3.000/1999, art. 647 (RIR/99) Instru��o Normativa SRF 23/1986 CSRF - Contribui��es Sociais Retidas na Fonte Lei 10.833/2003, art. 30 Instru��o Normativa SRF 459/2004 Instrutor: Sergio Reolon 07.07.2010