U.S. Banking System

U.S. Banking System. Financial Institutions Commercial Banks Focus: corporate services: lending, cash management Savings and Loans Focus: real estate mortgages Credit Unions Focus: Consumer loans and accounts. U.S. Banking System. Regulation of Banking System Most foreign countries

U.S. Banking System

E N D

Presentation Transcript

U.S. Banking System • Financial Institutions • Commercial Banks • Focus: corporate services: lending, cash management • Savings and Loans • Focus: real estate mortgages • Credit Unions • Focus: Consumer loans and accounts Payment System and Banking Relationships

U.S. Banking System • Regulation of Banking System • Most foreign countries • Few, large banks • Canada: Bank of Nova Scotia, TDB, CIBC, Bank of Canada, etc., found all across country Payment System and Banking Relationships

U.S. Banking System • Regulation of Banking System • United States • Numerous, small banks • Depression era legislation limited bank branches • Why? • In the 1980s, many Texas banks were in trouble • Legislation permitted out of state banks to acquire “troubled banks” • 1995: legislation passed permitting interstate banking • Many predicted only a few, large banks would remain at this point • With some banks increasing in size, such as Bank of America • Banks can provide cash collection and concentration for operations across country • But, personal touch was often lost: loan officers moved; phone trees Payment System and Banking Relationships

U.S. Banking System • Regulation Q • Corporations can not receive interest income on checking account balances • Sole proprietorships can have interest earning accounts • Alternative strategies: • Sweep accounts: excess balances into overnight loans • Firms with large cash balances • Money market mutual funds: • Minimum check amount generally $500 • Uninsured • Minimal risk as generally invested in government securities Payment System and Banking Relationships

U.S. Banking System • FDIC Insurance • $250,000 per account through 2009 • Married couple • Multiple banks • Capital requirements • Tier 1: $3 of common stock for $100 of assets • Tier 2: $8 of common, preferred stock for $100 of risk weighted assets • 100% risk factor: business loans • 50% risk factor: real estate loans • 0% risk factor: T bills • 150% risk factor: past due loans Payment System and Banking Relationships

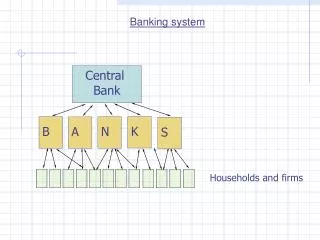

U.S. Banking System • Fed • Structure • 12 district banks • 25 regional branches • 6 regional check processing centers • Impact on payment system • Assists in processing checks • Provides wire transfer system for large payments • Provides ACH for small dollar electronic payments • Regulates availability schedules Payment System and Banking Relationships

U.S. Banking System • Check clearing • Fed credits collecting bank’s account and debits drawee bank’s account • Collecting bank records deposit; drawee bank records check • MICR line: • Fed Reserve Bank Code • Bank ID Number • Account Number • Check Number Payment System and Banking Relationships

U.S. Banking System • Check clearing • On Us: written on bank where check is deposited (30% checks) • Local: process by: • Courier presenting, clear through correspondent, local clearing house • Availability: max two business days • Out of Town: process by: • Courier presenting, presenting image, correspondent, Fed • Availability: max five business days Payment System and Banking Relationships

U.S. Banking System • Check clearing • Float • Collection: Day check written – Day funds available • Disbursement: Day check written – Day funds taken from account • Component • Mail • Processing • Clearing • Based on bank’s availability schedule Payment System and Banking Relationships

U.S. Banking System • Availability schedule: Fifth Third Bank, pages 291-295 • Eastwood Bank, Rochester, MN • First $100 next day • Local checks: two days • Out of town checks: five days • Longer availability: • Deposit more than $5,000 • Redepositing NSF check • Account has been overdrawn • New accounts: first 30 days • Electronic deposit: immediately • Cash, wire transfer, cashier checks up to $5,000: next day • Other checking deposits: 10 days Payment System and Banking Relationships

Electronic Payments • Wire Transfers: entry increasing one bank’s account and decreasing the other • Immediate access for large dollar amounts ($30,000 average) • Overnight loans of repo agreements • More expensive than other forms of moving funds • ACH: automatic deposit of payroll checks; government checks • One or two day availability • Cheaper to process than checks • $5 per ACH; 10 cents per item in ACH at First-Mid Illinois • Payor knows when funds will be withdrawn • May reduce float • Incentives to adopt ACH Payment System and Banking Relationships

Debit Cards • Processed locally or through ACH • Vendor: • Immediate availability for local accounts • Two business day availability if out of town • Customer: • Local checks: immediate withdrawal of funds • ACH: two days withdrawal Payment System and Banking Relationships

International Payments • Giro system • Payment made by customers; often at post office • Not sent to creditor • Funds are transferred between accounts based on account number • Bank then notifies company funds are available • Used for regular periodic payments • Can be made automatically • Value dating • Delays availability of deposits • Moves debit date for checks • To compensate for payment of interest Payment System and Banking Relationships

Managing Bank Relationships • Reliable services with reasonable costs • Services • Collection services: availability; concentration; lockbox • Payment services: wires; ach; letters of credit • Information services: advisory services on collection and disbursement • Credit services: line of credit; factoring; medium-term loans • Investment services: money market funds; repos Payment System and Banking Relationships

Managing Bank Relationships • Reliable services with reasonable costs • Reasonable costs • Account analysis statement • Benefit from company’s deposits exceed cost of bank providing services to company • I.E., is this company a profitable customer for bank? • Earnings Credit Allowance = Average collected balance x Earnings credit rate • Average collected balance = Ledger balance (amount in account) – Float (deposits not collected) – Required Reserves (Funds which can not be loaned) • Earnings credit rate = Based on T-bill rates; less than money market rates • Cost of providing services • Processing on us, local, out of town checks • Processing returned; redeposited checks • Fund transfers • Deposits • FDIC Insurance • If benefit > cost; excess benefit carried to next period • If cost > benefit; service charge or required balances increased next period Payment System and Banking Relationships