Download

1 / 34

340 likes | 627 Vues

ALBANIAN ASSOCIATION OF BANKS. SHOQATA SHQIPTARE E BANKAVE. ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE. ALBANIA Economy and Banking System. by Seyhan PENCAPLIGIL Member of AAB Executive Committee Budapest, 7-9 October 2008. ALBANIAN ASSOCIATION OF BANKS.

E N D

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAEconomy and Banking System by Seyhan PENCAPLIGIL Member of AAB Executive Committee Budapest, 7-9 October 2008

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN ECONOMY ALBANIA - Located in Southeastern Europe (Western Balkans) Economic Policy Framework • Open Market Economy, • No restrictions on profit and capital repatriation, • No exchange rate restriction, floating exchange rate regime, • Albania signed its Stabilization & Association Agreement with the European Union, the first formal step to eventual EU membership (12 June 2006).

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAMain Economic Features & Indicators • Macroeconomic performance of the Albanian economy has been good overall, with sustained growth and low inflation. • Annual economic growth has been around 6% during the last 5 years; 6% in 2007. • Domestic demand mainly driven by migrant remittances (EUR 947 million during 2007) which have significant impact on fiscal revenues and expenditures, as well as by other external current transfers, and rapidly expanding financial intermediation & credit. • Services, agriculture and industry share were respectively: 55,3%, 19,5% and 11.0% (2007).

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAMain Economic Features & Indicators (2) • EU is the main trading partner: 83.1% of exports and 59.8% of imports. SEE is the second trading partner: 12.4% of exports and 24.8% of imports. • Exports and imports (2007) reached EUR 786 million and EUR 3,04 billion – Net importer • …but more than 92% of the current account financed by remittances. • Foreign Direct Investments reached EUR 463 million (Dec.07). • Foreign reserves (Dec.07) were more than EUR 1.5 billion, covering 4 months of imports of goods and services.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAMain Economic Features & Indicators (3)

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAMacroeconomic Environment POLICIES Upward tendency of consumer prices during 2007. Inflation nearing 3 %. Fiscal Policy Prudential implementation of fiscal policies, by observing the planned parameters of fiscal indicators, has not transmitted excessive inflationary pressures and has contributed to maintaining price stability. Flat tax rate (10%) introduced since July 2007; labor tax (social insurance) to be cut to 15% by January 2009. Monetary Policy Monetary policy of the Bank of Albania has generally had a neutral stance, but following the inflationary pressures during 2007, BoA has taken prudent measures to put reins of inflation ans bring it within 2-4% target. Lending to the economy has been the main source of monetary expansion during 2007 and H1 2008.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAMacroeconomic Environment Albanian economy experienced relatively higher growth than other transition. With the exception of 1997 (following the collapse of the pyramid schemes), Albania has consistently outperformedor be in line with ecnomic growth of CEE countries. Source: IMF Source: IMF

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAMacroeconomic Environment Economic Growth Continuous and sustainable economic growth (5-6% annually). Price Stability Inflation is one the lowest within SEE countries (ranging between 2-4%).

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAMacroeconomic Environment Income & employment • GDP growth has enabled rise of income per capita beyond USD 3,400 per year, which, however, remains among the lowest figures in the region. • Notwithstanding the ongoing GDP growth in years, employment performance reflects a moderate behavior. • Unemployment rate reduction continues to be not significant, either in absolute value or in relative terms (Unemployment rate for 2007: 13.2%) .

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAMacroeconomic Environment Remittances • Albania’s receipts from workers’ remittances are, relative to GDP, among the highest in the world. • Remittances are considerably larger than exports (1.19 times – Dec.07) and FDI (2.05 times – Dec.07). • Remittances have significantly lowered the current account deficit and helped Albania build a comfortable level of external reserves. • Although the bulk of remittances is still sent through informal channels, the importance of the formal channel has being increased in recent years.

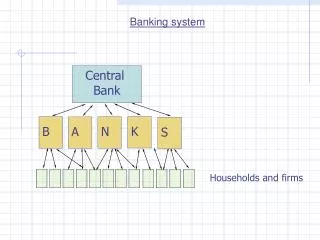

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Brief History Genesis The establishment of Imperial Ottoman Bank branch (1863) in Albanian territories. Central banking Establishment of the National Bank of Albania, jointly with Italian and Austrian banking groups, 4 October 1913. Mixed Central & Commercial Banking Establishment of National Bank of Albania (NBoA), 02 September 1925. Communist era NBoA was nationalized in 13 January 1945 and the Albanian State Bank (ASB) was established, with both functions as central & commercial bank.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Brief History Market Economy Two-tier banking system introduced and Bank of Albania established as the central bank of the Republic of Albania (1992). To date Albanian banking system has 16 commercial banks (from 01.01.2008 -).

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Main Features • Universal banking system, • The dominant sector within Albanian financial system, managing more than 95.5% of total financial assets, • Mainly foreign-owned (14 out of 16 banks are foreign-owned), • Some big International names entered Albanian banking system during 2007: - Intesa SanPaoloIMI bought American Bank of Albania and Italian-Albanian Bank (both banks were merged and by 01.01.08 operate under American Bank of Albania trademark); - Société Générale bought 75.01% of Popular Bank. • Almost all privately-owned (some minor state shareholdings), • A highly concentrated banking system; top five banks have a share of ~ 73% of total assets (Jun.08).

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Main Features Continuous institutional expansion and development… Other non-bank financial institutions [1] Subjects licensed by Bank of Albania. [2] Subjects licensed by Financial Supervision Authority, except for Leasing Companies.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Main Features More coverage with banking services…

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Main Indicators Performance of total assets Steady growth of banking assets…

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Main Indicators Deposits’ growth Continuous deposit growth – among the highest in SEE countries.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Main Indicators Credit performance Experiencing an extended credit boom, but credit ratios still low compared to EU and SEE standards.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Main Indicators Private Sector Loan Structure Credit Quality Still good credit quality despite credit boom; retail loans in expansion.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Main Indicators Average Interest Rates Still high interest rate spreads in ALL.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Performance Indicators

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Performance Indicators

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Exchange Rates Average Exchange Rates LEK (ALL) has been significantly appreciated against US$ during last years, and more stable against EURO.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Electronic Cards

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Regulatory Framework Law no.9662, dt.18.12.2006 “On Banks in the Republic of Albania”. Main Licensing Requirements for Credit Institutions • Banks shall be founded as joint stock companies. No discriminatory restrictions in terms of capital participation and formation. • The minimum amount of initial capital required, paid in cash, in respect of a bank, is not less than ALL 1 billion (for existing banks: ALL 850 million, but from March 1st, 2008 will be raised to ALL 1 billion); • Administrators having a business or professional history for the past 3 years, • The bank shall have at least two general executive directors. Licensing Requirements for bank’s branch office Similar requirements as those required for Albanian banks.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Regulatory Framework Licensing • Preliminary approval or deny, within 3 months from the date of its receipt of the application for a license at Bank of Albania. • A bank or branch of foreign bank, which has been granted preliminary approval shall, within one year starting from the day of the preliminary approval, request in writing from the Bank of Albania granting of the final license. Scope of activity • Universal banking principle. • The range of allowed banking & financial activities a bank may provide is subject of central bank’s approval (no capital quota qualifications).

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Banking Supervision Prudential Banking Supervision The supervision process is carrying out through the following instruments: • Periodic data reporting regarding banking financial indicators, through unified reporting system (reporting various balance and off-balance sheet items, as well as other indicators, as the supervision regulatory framework requires); • Ad hoc (special) reporting of various data; • On-site (full scale or targeted) examinations; • Off-site analysis. • CAMELS system is employed during on-site examinations (CAMELS rankings range from “1” – top performance- to “5” – poor performance).

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Banking Supervision (2) Bank of Albania has already approved a set of all necessary and well-detailed rules and regulations, whose implementation help to ensure prudential banking supervision, as follows: • Regulation “On Capital Adequacy”,, • Regulation “On the amount and fulfillment of minimum initial capital of the allowed activities of banks and branches of foreign banks”, • Guideline “On Bank’s Regulatory Capital”, • Regulation “On Market Risks”, • Guideline “On the Liquidity of the Bank”, • Regulation “On Significant Risk Management”, • Regulation “On Open Foreign Positions”, • Regulation “On Bank Relations with persons related to bank”.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Credit Register Bank of Albania passed the Regulation “On Credit Register Operation”, (18.07.2007), which has entered into force by 01.01.2008. Its purpose is to define the organization and operational rules of the Bank of Albania Credit Register, as an electronic database.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Payment System The Albanian payment system is run and regulated by Bank of Albania. Postal service network, part of payment system also, mainly for money transfer ordered by individuals. Bank of Albania is the operator of two payment systems: AIPS (Albanian Interbank Payment System), a real-time gross settlement system (RTGS), which processes all interbank big value (equal to or exceeding ALL 1,000,000 (~USD 10,000)) payments (a SWIFT-based Y-copy service, “live” from January 2004).

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Payment System (2) AECH (Albanian Electronic Clearing House) System, an automated clearing system, for processing banks’ payments to their clients (small value payments; “live” from 2005). The system is fully integrated with AIPS and the net clearing position is settled daily in AIPS. Both systems are owned by Bank of Albania. On August 2008, BoA approved the new legal framework on IBAN usage (effective by May2009). Direct Debiting regulation still in preparatory phase.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS ALBANIAN BANKING SYSTEM Future Developments & Challenges • Reduction of informal economy, • Further expansion of banking retail chains and products, more banking service coverage, • Introduction of new technology: e-banking, • Full implementation of IAS/IFRS, by January 2008, • Increasing the beneficial effects of remittances, by attempting to channel most of them through the financial system.

ALBANIAN ASSOCIATION OF BANKS SHOQATA SHQIPTARE E BANKAVE ALBANIAN ASSOCIATION OF BANKS Contacting AAB URL: www.aab.al E-mail: secretariat@aab-al.org