Download

1 / 73

750 likes | 1.2k Vues

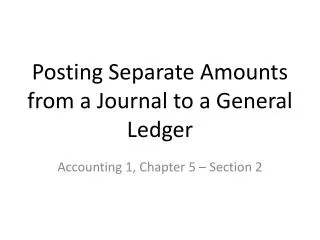

Posting Journal Entries to Ledger Account and Trial Balance. Journalizing and Posting. JOURNAL. Page 2. Post. Ref. Date. Description. Debit. Credit. 2005. Dec. 31. Dec. 1 NetSolutions paid a premium of $2,400 for a comprehensive insurance policy covering two years. 1 2 3 4.

E N D

JOURNAL Page 2 Post. Ref. Date Description Debit Credit 2005 Dec. 31 Dec. 1 NetSolutions paid a premium of $2,400 for a comprehensive insurance policy covering two years. 1 2 3 4 Prepaid Insurance 2 400 00 Cash 2 400 00 Paid premium on two-year policy.

JOURNAL Page 2 Post. Ref. Date Description Debit Credit 2005 Dec. 1 2005 Dec. 1 1 2 3 4 Prepaid Insurance 2 400 00 Cash 2 400 00 Paid premium on two-year policy. ACCOUNT NO. 15 ACCOUNT Prepaid Insurance Balance Post. Ref. Credit Credit Debit Debit Date Item 2 400 00 2 400 00

JOURNAL Page 2 Post. Ref. Date Description Debit Credit 2005 Dec. 1 2005 Dec. 1 1 2 3 4 Prepaid Insurance 2 400 00 15 Cash 2 400 00 Paid premium on two-year policy. ACCOUNT NO. 15 ACCOUNT Prepaid Insurance Balance Post. Ref. Credit Debit Credit Debit Date Item 2 2 400 00 2 400 00

1 2 3 4 Prepaid Insurance 2 400 00 15 Cash 2 400 00 Paid premium on two-year policy. JOURNAL Page 2 Post. Ref. Date Description Debit Credit 2005 Dec. 1 2005 Nov. 30 ACCOUNT NO. 11 ACCOUNT Cash Balance Post. Ref. Credit Credit Debit Debit Date Item 2 2 000 00 5 900 00 Dec. 1 2 400 00 3 500 00

1 2 3 4 Prepaid Insurance 2 400 00 15 Cash 2 400 00 Paid premium on two-year policy. JOURNAL Page 2 Post. Ref. Date Description Debit Credit 2005 Dec. 1 2005 Nov. 30 11 ACCOUNT NO. 11 ACCOUNT Cash Balance Post. Ref. Credit Credit Debit Debit Date Item 2 2 000 00 5 900 00 Dec. 1 2 2 400 00 3 500 00

1 Dec. 1 NetSolutions paid rent for December, $800. 14 15 16 17 Rent Expense 52 800 00 Unearned Rent 11 800 00 Paid rent for December.

1 Dec. 1 NetSolutions receives $360 for three month’s rent for land beginning December 1. 14 15 16 17 Cash 11 360 00 Unearned Rent 23 360 00 Received advanced payment For three months’ rent of land.

4 Dec. 4 NetSolutions purchased office equipment on account from Executive Supply Co. for $1,800. 18 19 20 21 Office Equipment 18 1 800 00 Accounts Payable 21 1 800 00 Purchased office equipment on account.

6 Dec. 6 NetSolutions paid $180 for a newspaper advertisement. 21 22 23 24 Miscellaneous Expense 59 180 00 Cash 11 180 00 Paid for newspaper ad.

11 Dec. 11 NetSolutions paid creditors $400. 24 25 26 27 Accounts Payable 21 400 00 Cash 11 400 00 Paid creditors on account.

JOURNAL Page 3 Post. Ref. Date Description Debit Credit 2005 Dec. 13 Dec. 13 NetSolutions paid a receptionist and part-time assistant $950 for two weeks’ wages. 1 2 3 4 Wages Expense 51 950 00 Cash 11 950 00 Paid two week’s wages.

16 Dec. 16 NetSolutions received $3,100 from fees earned for the first half of December. 5 6 7 8 Cash 11 3 100 00 Fees Earned 41 3 100 00 Received fees from customers.

16 Dec. 16 Fees earned on account totaled $1,750 for the first half of December. 9 10 11 12 Accounts Receivable 12 1 750 00 Fees Earned 41 1 750 00 Received fees from customers.

20 Dec. 20 NetSolutions paid $900 to Executive Supply Co. on the $1,800 debt owed from the December 4 transaction. 13 14 15 16 Accounts Payable 21 900 00 Cash 11 900 00 Paid part of amount owed to Executive Supply Co.

21 Dec. 21 NetSolutions received $650 from customers in payment of their accounts. 18 19 20 21 Cash 11 650 00 Accounts Receivable 12 650 00 Received cash from customer on account.

23 Dec. 23 NetSolutions paid $1,450 for supplies. 22 23 24 25 Supplies 14 1 450 00 Cash 11 1 450 00 Purchased supplies.

27 Dec. 27 NetSolutions paid the receptionist and part-time assistant $1,200 for two weeks’ wages. 27 28 29 30 Wages Expense 51 1 200 00 Cash 11 1 200 00 Paid two weeks’ wages.

31 Dec. 31 NetSolutions paid its $310 telephone bill for the month. 31 32 33 34 Utilities Expense 54 310 00 Cash 11 310 00 Paid telephone bill.

JOURNAL Page 4 Post. Ref. Date Description Debit Credit 2005 Dec. 31 Dec. 31 NetSolutions paid its $225 electric bill for the month. 1 2 3 4 Utilities Expense 54 225 00 Cash 11 225 00 Paid utility bill.

31 Dec. 31 NetSolutions received $2,870 from fees earned for the second half of December. 5 6 7 8 Cash 11 2 870 00 Fees Earned 41 2 870 00 Received fees from customers.

31 Dec. 31 NetSolutions earned $1,120 on account for the second half of December. 9 10 11 12 Accounts Receivable 12 1 120 00 Fees Earned 41 1 120 00 Recorded fees earned on account.

31 Dec. 31 NetSolutions paid dividends of $2,000 to stockholders. 14 15 16 17 Dividends 33 2 000 00 Cash 11 2 000 00 Paid dividends to stockholders.

16 Dec. 16 NetSolutions received $3,100 from fees earned for the first half of December. 5 6 7 8 Cash 11 3 100 00 Fees Earned 41 3 100 00 Received fees from customers.

16 Dec. 16 Fees earned on account totaled $1,750 for the first half of December. 9 10 11 12 Accounts Receivable 12 1 750 00 Fees Earned 41 1 750 00 Received fees from customers.

20 Dec. 20 NetSolutions paid $900 to Executive Supply Co. on the $1,800 debt owed from the December 4 transaction. 13 14 15 16 Accounts Payable 21 900 00 Cash 11 900 00 Paid part of amount owed to Executive Supply Co.

21 Dec. 21 NetSolutions received $650 from customers in payment of their accounts. 18 19 20 21 Cash 11 650 00 Accounts Receivable 12 650 00 Received cash from customer on account.

23 Dec. 23 NetSolutions paid $1,450 for supplies. 22 23 24 25 Supplies 14 1 450 00 Cash 11 1 450 00 Purchased supplies.

27 Dec. 27 NetSolutions paid the receptionist and part-time assistant $1,200 for two weeks’ wages. 27 28 29 30 Wages Expense 51 1 200 00 Cash 11 1 200 00 Paid two weeks’ wages.

31 Dec. 31 NetSolutions paid its $310 telephone bill for the month. 31 32 33 34 Utilities Expense 54 310 00 Cash 11 310 00 Paid telephone bill.

JOURNAL Page 4 Post. Ref. Date Description Debit Credit 2005 Dec. 31 Dec. 31 NetSolutions paid its $225 electric bill for the month. 1 2 3 4 Utilities Expense 54 225 00 Cash 11 225 00 Paid utility bill.

31 Dec. 31 NetSolutions received $2,870 from fees earned for the second half of December. 5 6 7 8 Cash 11 2 870 00 Fees Earned 41 2 870 00 Received fees from customers.

31 Dec. 31 NetSolutions earned $1,120 on account for the second half of December. 9 10 11 12 Accounts Receivable 12 1 120 00 Fees Earned 41 1 120 00 Recorded fees earned on account.

31 Dec. 31 NetSolutions paid dividends of $2,000 to stockholders. 14 15 16 17 Dividends 33 2 000 00 Cash 11 2 000 00 Paid dividends to stockholders.

Posting Journal Entries to the Ledger Accounts Let’s see what the cash account looks like after posting the cash portion of this transaction for JJ’s Lawn Care Service.

Ledger Accounts After Posting This ledger format is referred to as a running balance (as opposed to simple T accounts).

What is Net Income? Net income is not an asset it’s an increase in owners’ equity from profits of the business. A=L+OE Increase Decrease Increase Either (or both) of these effects occur as net income is earned . . . . . . but this is what “net income” really means.

Retained Earnings A=L+OE Capital Stock Retained Earnings The balance in the Retained Earnings account represents the total net income of the corporation over the entire lifetime of the business, less all amounts which have been distributed to the stockholders as dividends.

Revenue and Expenses The price for goods sold and services rendered during a given accounting period. Increases owner’s equity. The costs of goods and services used up in the process of earning revenue. Decreases owner’s equity.

The Realization Principle: When To Record Revenue Realization Principle Revenue should be recognized at the time goods are sold and services are rendered.

The Matching Principle: When To Record Expenses Matching Principle Expenses should be recorded in the period in which they are used up.

EQUITIES Debit for Decrease Credit for Increase EXPENSES REVENUES Debit for Increase Credit for Decrease Debit for Decrease Credit for Increase Debits and Credits for Revenue and Expense Expenses decrease owner’s equity. Revenues increase owner’s equity.

EQUITIES Debit for Decrease Credit for Increase CAPITAL STOCK Debit for Decrease Credit for Increase Investments by and Payments to Owners Payments to owners decrease owners’ equity. Owners’ investments increase owners’ equity. DIVIDENDS Debit for Increase Credit for Decrease

Let’s analyze the revenue, and expense transactions for JJ’s Lawn Care Service for the month of May. We will also analyze a dividend transaction.

May 29: JJ’s provided lawn care services for a client and received $750 in cash. Will Sales Revenue increase or decrease? Will Cash increase or decrease?

Sales Revenue increases $750 with a credit. Cash increases $750 with a debit. • May 29: JJ’s provided lawn care services for a client and received $750 in cash.