Download

1 / 24

270 likes | 612 Vues

The further step of Accounting Process after Recording is Classification of Accounts, done in Ledger: A Principal books of Accounts are discussed Here. Balancing of Ledger Accounts, a List of all accounts (Trial Balance) is discussed as a Summarization of Accounting process.

E N D

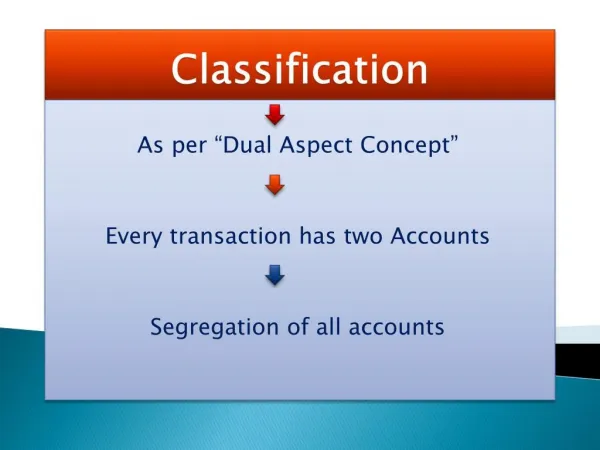

Classification As per “Dual Aspect Concept” Every transaction has two Accounts Segregation of all accounts

Ledger Classification In a book called “Ledger” Preparing “Ledger Accounts” Transferring Journal entries into Ledger “Posting”

Ledger Verifies the “Double entry / Dual aspect system” Compiles all related information to a particular account Includes Posting the entries & Casting& Balancing the accounts.

Ledger A Principal books of accounts Book of “Second Entry” Book for the “Analytical record” ( Note : Journal - Book for Chronological Record )

Specimen of Ledger A “T” shape Account, having two sides “Debit & Credit”

Process of ledger For Opening balance, “Balance Brought Down/Forward “ is used. For Closing balance, “Balance Carried Down/Forward “ is used. The closing Balance is of the side having “ higher total” Generally “Nominal Accounts” are not balanced

Question • Prepare the Stationery Account of a firm for the year ended 31.12.2015 duly balanced off, from the following details:

Summarizing At the period end the list of balances of all accounts Trial Balance (compilation of all transactions & accounts)

Trial balance The balances(Dr./Cr.) (from Ledger)- transferred to Trial Balance Purpose : To verify the arithmetical accuracy Rectification of Errors Basis of Financial Statements (Agreement of Trial Balance does not mean that there are no errors left at all) (Any Difference in Trial Balance- Suspense A/C)

Format of Trial Balance • Balance Method:

Format of Trial Balance Total & Balance Method:

Format of Trial Balance Total Method:

Methods of Trial Balance Balance Method (Dr/Cr Balances from Ledger Accounts are Transferred) Total Method The totals(without balancing) of both the sides of accounts Balance & Total Method. (The totals & Balances, both are recorded)

Balances of Trial Balance • Debit Balance : An Asset/ Debtor/ Expenses • Credit Balance: A Liability/ Creditor/ Incomes

MCQs Q.1. ____________is prepared to ascertain the arithmetical accuracy of posting and balancing of accounts

MCQs Q.2. The left hand side of an account is known as _________ and the right hand side of an account is known as ________

MCQs Q.3. Income tax in case of a sole trader is treated as _____

MCQs Q.4. On March 31, 2010 Narain Enterprises purchased a loader from Laxmi Motors for Rs. 1,75,000 which is shown in the balance sheet as on 31st March, 2010. This is –

MCQs Q.5. Payment received from debtor –

MCQs Q.6. Market value of investment is shown outside the Balance Sheet as a footnote according to

MCQs Q.7. Which of the following is a credit transaction?

MCQs Q.8. Sales of office furniture should be credited to:

MCQs Q.9. ______. is a summary of all assets and liabilities on a particular date.

MCQs Q.10. Which of the following lists the balance and the title of accounts given in the ledger, on a given date?