Costs

Costs. Learning Objectives: . Distinguish between explicit, implicit cost and economic cost. Distinguish between short-run and long-run cost. Distinguish between fixed cost, variable cost, total cost, marginal cost Explain the law of diminishing returns. . In Economics.

Costs

E N D

Presentation Transcript

Learning Objectives: • Distinguish between explicit, implicit cost and economic cost. • Distinguish between short-run and long-run cost. • Distinguish between fixed cost, variable cost, total cost, marginal cost • Explain the law of diminishing returns.

In Economics • Because of the condition of scarcity, economic cost (OC), which include all cost of production, are opportunity cost of all resources used in the production

Explicit Cost • Payment made by a firm to outsiders to acquire resources for use in production. • Example: • A firm hires labour and pays wages; it purchases materials and pays suppliers; it uses elictricity and pays the supplier and etc.

Implicit Cost: • A sacrificed income arising from the use of self-owned resources by firms. • For example: • In the case of office building owned and used by the firm, the opportunity cost is the potential income earned by renting the building. The hours of work the owner of the firm puts into his/ her business is equal to the potential income earned working elsewhere.

Economic Cost: • The sum of explicit and explicit costs, or total opportunity cost incurred by a firm for its use of resources, whether purchased or self-owned. • When economists refer to ‘cost’ they mean economic cost. • Example: • Suppose I make $ 60000 a year as a teacher. I decide to open my own coffee shop. The entrepreneurial effort I put in my business is $45000 a year. I set up my office in the basement of my house which I could rent for $4000 a year. I borrowed $30000 plus $2000 in interest a year to pay for my resources. I pay $18000 a year in wages. • Implicit cost= 60000+45000+4000=109000 • Explicit cost=2000+30000+18000=50000 • Economic cost =109000+50000= 159000

Distinguish between explicit, implicit cost and economic cost. • Why are economic costs greater than explicit costs? • Post your answer on edmodo.

Remember • In the short-run at least one factor input is fixed. • In the long-run all inputs are variable.

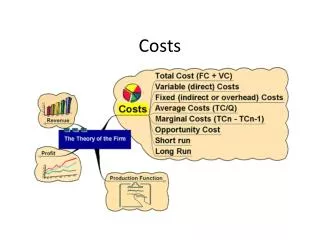

Costs • In buying factor inputs, the firm will incur costs • Costs are classified as: • Fixed costs – costs that are not related directly to production – rent, rates, insurance costs, admin costs. They can change but not in relation to output • Variable Costs – costs directly related to variations in output. Raw materials primarily

Costs • Total Cost -the sum of all costs incurred in production • TC = FC + VC • Average Cost – the cost per unit of output • AC = TC/Output • Marginal Cost – the additional cost of producing one more unit of output • MC= ΔTC/ΔQ or ΔTVC/ΔQ • (In the LR there are no fixed costs so all FC=VC)

AFC=TFC/Q • AVC=TVC/Q • ATC=TC/Q • TC=TFC+TAC • ATC=AFC+AVC

Distinguish between TC, MC and AC. • Post your answer on edmodo

Relating the cost and product curve: Law of diminishing returns

Relating the cost and product curve: Law of diminishing returns • The law of diminishing returns is very important in determining the shape of the cost curves. • Increasing marginal returns: • Extra output produced by an extra unit of labour rises • This means the the additional cost of producing n additional unit (MC) falls • Decreasing marginal returns • And additional output of each unit of labour is falling • Therefore the additional cost of each unit (MC) increases

remember • The U-shape of the AVC,ATC and MC is due to the laws of diminishing marginal returns. This also explains the why the AVC and MC curves are mirror images of the AP and MP curves

Test your knowledge • Explain the relationship between the product curves and the cost curves with reference to the laws of diminishing marginal returns.

Complete the provided handout on “Theory of Cost” and “Short-run”

You must be able to distinguish between increasing, decreasing and constant return to scale.

Remember • In the long-run, all inputs are variable

Increasing returns to scale: • It means that output increases more than in proportion to the increase in all inputs • Constant returns to scale: • It means that output increases at the same proportion as all inputs • Decreasing returns to scale: • Output increases less in proportion to the increase in all inputs.

Test your knowledge: edmodo • Post your answer on edmodo • distinguish between increasing, decreasing and constant returns to scale.

Long-run Average Total Cost Curve: • Curve shows the lowest possible AC that can be attained by a firm for any level of output when all firm’s input are variable. • It is the curve that touches each of many short-run ATC. • It is known as the planning curve

Economies of Scale = if making cost savings from the increase in scale of production • Diseconomies of scale = if average cost of production rises as the produce more

Financial Economies • Cost savings by the way firms raise money • Selling shares • Borrowing money to buy machinery • Lower interest (for loans)

Market Economies • Cost savings by the way they sell their product • Buy in bulk • Employ purchasing specialists and sales people

Technical Economies • Cost savings by method of production • Specialized workers and machinery • Research a faster method of production • Types of transport

Risk-bearing Economies • Cost savings by reducing the risk of fall in demand • Using many different suppliers • Diversification of goods

Management diseconomies • Too many departments and managers= disagreements

Labour Diseconomies • Disengagement of the workers • Strikes and disruptions

Read the Cost section of the micro packet or your text book and answer the following question • Describe factors giving rise to the economies of scale, including specialization, efficiency and marketing. • Describe the factors giving rise to the diseconomies of scale

Remember: • Short run – Diminishing marginal returns results from adding successive quantities of variable factors to a fixed factor • Long run – Increases in capacity can lead to increasing, decreasing or constant returns to scale