Download

1 / 24

250 likes | 396 Vues

This document provides a comprehensive overview of fraud, examining why it occurs, common types, and effective investigative techniques. Key factors contributing to fraud include non-observance of rules, inadequate supervision, and technological misuse. Various fraud types discussed include bank transactions, postal services, and computer-related offenses. The investigation process focuses on detecting fraud sources, assessing losses, identifying offenders, and ensuring evidence preservation. A detailed methodology is outlined for documenting findings and executing remedial actions to prevent future occurrences and restore customer trust.

E N D

Investigation Investigation

Why frauds take place? • Non-observance of rules • Laxity in Supervision • Lacunae in Rules and operating procedure • Lenient approach against minor irregularities • Ignoring with warning, censure etc where a strong penalty is warranted

Why frauds take place? • Improper induction of technology • Misuse of Password, Retaining data entry module, data entry based on cut off date • Data entry based on passbooks etc

Kinds of frauds • Savings Bank transactions • Treasury / Sub Accounts (Cash & Stamps) • Money Orders • Bogus Money Order • Franking Machine • Postal Life Insurance • Theft & Dacoity • Computer related

Kinds of frauds….. • Mails • Loss of contents of bags • Loss of tampering of bags • Pilferage of stamps • Pilferage of articles • Use of defaced stamps • Loss of cash bag/valuable • Insured Articles, Registered & VP article

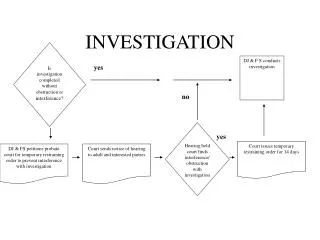

WHAT HOW BY WHOM WHEN WHY Details of offence, violation of rule Manner in which it is committed Responsibility Period of fraud Criminal intention Ingredients for detection of fraud

Object of Investigation • Detection of source of the fraud • Identification of modus operandi • Examination material objects used in the fraud & their preservation • Assessment of • extent of loss • damage to image of PO • extent of customer dissatisfaction

Object of Investigation…. • Identification of failures & lapses that abetted the fraud • Detection of related frauds • Fixing of responsibility • Main offenders • Active abettors • Passive abettors (contributory negligence)

Object of Investigation…. • Assessment of compensation/ claim to be paid • Decision on whether to report to police • Gathering evidence for departmental action • Remedial measures to avoid recurrence • Suggested amendments to rules • Restoration of faith of customer

Seizure and verification of documents • Identification of related documents • Verification of available inputs with reference to records. • Establishing a prima facie case based on the verification • Identifying the main offender(s).

Seizure and verification of documents • Recording the statement of the main offender based on the records, statement of customers/complainant and statements of witnesses • Recording the statement of supporting staff including subsidiary offenders • Seizure of all related documents

Preparation of Inventory • Shortage of Cash and stamps • Physically verify the available cash and stamp balances in the presence of the SPM/BPM and other available staff • Shortage/loss of Savings Certificates • List of unsold stock • Shortage/loss of Indian Postal Orders • List of unsold stock

Preparation of Inventory… • Shortage/loss of Accountable articles • List of insured/VP/eMO/Regd • Non – Delivery of Ordinary articles • List of undelivered letters • Pilferage of postage stamps • Raiding of the counters and unauthorized possession of articles and stamps noticed – to be seized. • Unauthorized possession of Pass books etc. • During inspection/investigation – to be seized

Preliminary Investigation Report • Preamble to contain the source/information which led to the commencement of the investigation showing the date of visit/conducting the enquiry • A brief description of the office is to be included • The basic information pertaining to the irregularity/ fraud to be furnished • The findings based on the evidences collected to be included

Preliminary Investigation Report… • The extent of involvement of the main offender and subsidiary offenders is to be assessed and furnished • There has to be a conclusion based on the findings. • The further course of action proposed to be furnished • The details of assistance required should be made clear

Exercise 10.2.3 (Case study)

Past Work Verification • Verification of work of official done in last one year from date of commission of fraud • Savings Bank: • Cent per cent • MO & others: • Some % as per the quantum of frauds suspected minimum of 20%

Past work verification…. • On completion of past work verification submit final report containing following information • Total amount of fraud involved • List of officials amounting contributory negligence • Claim applications • Any other items requires attention

Components of DLIR/CLIR • Introduction – Profile of the place • How the fraud came to light • Departmental enquiry -commencement & completion • Total amount involved and net loss • Adjustment of loss/ particulars of recovery • Modus Operandi • Principal Offender – Biodata with past history • Criminal prosecution • Preservation of Records

Components of CLIR/DLIR…. • Visits and Inspection • Contributory negligence – Divl office, Sub Divisional office, Account office, HO, SBCO • Settlement of claims • Lacunae in Rules • Action taken so far – 100% verification,Issue of Charge sheet etc • Action to be completed. • SQF is to be attached to the CLIR

Exercise (Scrutiny of given Report)