Download

1 / 62

690 likes | 1.16k Vues

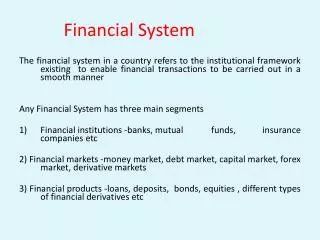

Financial System in India. Financial Sector consists of three main segments viz., 1) Financial institutions -banks, mutual funds, insurance companies 2) Financial markets -money market, debt market,capital market, forex market 3) Financial products -loans, deposits, bonds, equities.

E N D

Financial System in India • Financial Sector consists of three main segments viz., • 1) Financial institutions -banks, mutual funds, insurance companies • 2) Financial markets -money market, debt market,capital market, forex market • 3) Financial products -loans, deposits, bonds, equities

Banking in India - Banking in India is governed by BR Act,1949 and RBI Act,1934 - Banking in India is controlled/monitored by RBI and Govt of India - The controls for different banks are different based on whether the bank/s is/are a) statutory corporation b) a banking company c) a cooperative society

Banking Regulation Act,1949 (BR Act)-1 - BR Act covers banking companies and cooperative banks, with certain modifications. - BR Act is not applicable to a) primary agricultural credit societies b) land development banks • BR Act allows RBI (Sec 22) to issue licence for banks

Reserve Bank of India Act,1934(RBI Act)-1 • RBI Act was enacted to constitute the Reserve Bank of India • RBI Act has been amended from time to time • RBI Act deals with the constitution, powers and functions of RBI

Reserve Bank of India Act,1934(RBI Act)-2 • RBI Act deals with: • incorporation, capital management and business of banks • central banking functions • financial supervision of banks and financial institutions • management of forex/reserves • control functions : bank rate,audit,accounts • penalities for violation

Reserve Bank of India - 1 • Reserve Bank of India was established in • 1935, after the enactment of the Reserve • Bank of India Act 1934 (RBI Act). • Banking Regulation Act,1949 (BR Act)gave wide powers to RBI as regards to establishment of new banks/mergers and amalgamation of banks,opening of new branches,etc • BR Act,1949 gave RBI powers to regulate,superivse and develop the banking system in India

Money Market Instruments • Inter bank call money/deposit • Inter bank notice money/deposit • Inter bank term money/deposit • Certificates of Deposit • Commercial Paper • Treasury Bills • Bill rediscounting • Repos

Certificates of Deposit • CDs are short-term borrowings in the form of UPN issued by scheduled commercial banks and are freely transferable by endorsement and delivery. • Introduced in 1989 • Minimum period 7 days and maximum period one year. FIs are allowed to issue CDs for a period between 1 year and up to 3 years • Minimum amount is Rs 1,00,000.00 • Subject to payment of stamp duty under the Indian Stamp Act, 1899 • Issued to individuals, corporations, trusts, funds and associations • Issued at a discount rate freely determined by the market/investors

Commercial Paper • Short-term borrowings by corporates, financial institutions, primary dealers from the money market • Can be issued in the physical form (Usance Promissory Note) or de mat format • Introduced in 1990 • When issued in physical form are negotiable by endorsement and delivery and hence, highly flexible • Maturity is 7 days to 1 year • Unsecured and backed by credit rating of the issuing company • Issued at discount to the face value

Repos • Repo (repurchase agreement) instruments enable collateralised short-term borrowing through the selling of debt instruments • A security is sold with an agreement to repurchase it at a pre-determined date and rate • Reverse repo is a mirror image of repo and reflects the acquisition of a security with a simultaneous commitment to resell

INDIAN CAPITAL MARKET • Indian Capital Market plays an important role in the economic development of the country • It provides opportunities for investors to invest in the market and also to earn attractive rate of return. • It also creates source of funds for the various sectors • National Stock Exchange (NSE) and Bombay Stock Exchange (BSE) are the major stock exchanges in India

Securities & Exchange Board of India (SEBI) • SEBI was constituted on April 12/1988, and obtained the statutory powers in March,1992 • SEBI’s functions: • To protect the interests of investors • To recognize the business in stock exchanges and other security markets • To supervise and regulate work of intermediaries, such as stock brokers merchant bankers/custodians depositories/bankers to the issues

Association of Mutual Funds in India (AMFI) • AMFI is an association as a non profit organization. • AMFI represents mutual funds in India and working for healthy growth of the Mutual Funds. • AMFI conduct examinations for MF executives as part of their training activities

Insurance Regulatory & Development Authority (IRDA) • The regulator for insurance business in India is IRDA. • IRDA was established in 2000 • IRDA’s functions: • To regulate, promote and ensure orderly growth of the insurance business and reinsurance business in India • To protect the interests of policy holders

Insurance Sector • Insurance Sector in India can be divided into two main sections

Financial Intermediaries (1) • Mutual Funds- As financial intermediary promote savings and mobilise funds which are invested in the stock market and bond market • MFs are associations or trusts of public members and assist them in making investments in the financial instruments of the business/corporate sector for the mutual benefit of its members. • MFs aims to reduce the risks in investments Mutual funds help their investors to enhance their value by investing the funds in capital market. • Mutual funds offer various schemes: growth fund, income fund, balanced fund,sector wise funds, etc., • Regulated by SEBI

Financial Intermediaries (2) • Merchant banking- Another important financial intermediary which manages and underwrites new issues, undertake syndication of credit, advise corporate clients on fund raising • Subject to regulation by SEBI and RBI • SEBI regulates them on issue activity and portfolio management of their business. • RBI supervises those merchant banks which are subsidiaries or affiliates of commercial banks

Indian Banking - Significant events 1 • Three presidency banks were established in Calcutta (1806) in Bombay (1840) and in Madras (1843) • In the early part of 20th century, on account of the Swadeshi movement a number of join stock banks were established by Indians like Bank of India, Bank of Baroda and Central Bank of India. • In 1921 the three presidency banks were merged and the Imperial Bank of India was created. • During the period 1900 to 1925 many banks failed, and the Government appointed in 1929 a Central Banking Enquiry Committee to trace the reasons for the failure of banks. • The Reserve Bank of India Act was passed in 1934 and the RBI came into existence in 1935 and RBI was nationalised in 1949 • The Banking Regulation Act,1949 gave wide powers to RBI to act as the regulator for banks in India

Indian Banking -Significant events 2 • In 1955 State Bank of India became the successor to the Imperial Bank of India ,under the State Bank of India Act,1955. • In 1959 State Bank of India (Subsidiary Banks) Act was passed to enable SBI to take over State Associated banks as SBI’s subsidiaries • In 1969 the Government of India nationalised 14 major commercial banks having deposits of Rs.50 crore or more • In 1975 Regional Rural Banks were established under RRB Act 1976, which was preceded by RRB Ordinance in 1975 • In 1980 six more commercial banks were nationalised, with a deposit of Rs.200 crore or more

Progress of banking in India • In the liberalised, privatised and globalised environment, banks opeating in India have diversified their banking activities by offering Para Banking facilities like • Merchant banking/Mutual funds • ATMs/Credit Cards/Internet banking • Venture capital funds • Factoring • Bancassurance

Classification of Banks-3 • Public Sector Banks =State Bank of India+SBI’s associate banks+ Nationalised banks • Private Sector Banks=Indian Private Sector Banks (Old/New generation banks)+Foreign banks in India • Other Banks=Regional Rural Banks(RRB)

RESERVE BANK OF INDIA • SUPERVISORY & REGLATORY • Issuance of currency notes • Banker’s Banker • Lender of the last resort • Credit Control & Monetary Policy • Exchange Control & Forex Management • Funds Transfer

CREDIT CONTROL • QUANTITATIVE CREDIT CONTROL • QUALITATIVE CEDIT CONTROL’ • CRR & SLR • BANK RATE • OPEN MARKET OPERATIONS

Functions of Banks - 2 • Commercial Banks-Core Banking Functions • Acceptance of deposits from public • Lending funds to public/corporates • Investing funds in various opportunities • Collecting cheques/drafts and other Negotiable Instruments • Remitting funds

Functions of Banks-3 • Commercial Banks – Para Banking Services • Providing safe deposit lockers • Acceptance of safe custody items • Acceptance of standing instructions • Offering internet banking facilities • Issuance of credit and other cards including ATM cards • Offering various products like Mutual funds,insurance products, merchant banking services • Acting as executors and trustees

Foreign Currency Non-residentDeposit Accounts –FCNR (B) • FCNR (B) accounts • NRIs,PIOs,residing outside India can open FCNR (B) accounts • FCNR (B) accounts are maintained as fixed deposits in certain designated currencies • The designated currencies are: • US$, GBP, Japanese Yen, Euro, Cad$, Aus $ • Maintained in Banks in India in the above mentioned foreign currencies and interest is also earned in such foreign currencies • Repatriation of funds (principal, interest) is allowed

Know Your Customer (KYC) -1 • KYC: Know Your Customer • Know your customer (KYC) norms are applicable to all types of customer a/cs. • It deals with not only to identify the customer but also to understand the activities of the customer, and to ensure that the operations in the customer account/s is/are for genuine purpose

Know Your Customer (KYC) -2 • Application of KYC norms have become important due to various reasons. • In view of many issues on account of drugs smuggling, money laundering, terrorist activities, arms dealing,etc., banks need to be careful in dealing with their clients.

BANKER-CUSTOMERRELATIONSHIP • DEBTOR-CREDITOR • CREDITOR-DEBTOR • AGENT-PRINCIPAL • LESSOR-LESSEE • BAILEE-BAILOR

NEGOTIABLE INSTRUMENTS BANKER’S DUTIES & RESPONSIBILITIES C0LLECTING BANKER COLLECTION OF CHEQUES

Six Cs • Character • Capital • Capacity • Collateral • Condition • Compliance

CHARGES • HYPOTHECATION • PLEDGE • MORTGAGE • ASSIGNMENT • LIEN • SET OFF