A Challenging future For North American Refiners

270 likes | 480 Vues

A Challenging future For North American Refiners. Alan Gelder Head of Downstream Consulting. Miami October 26, 2010. $/bbl. 9. 8. 7. 6. 5. 4. 3. 2. 1. 0. 2005. 2006. 2007. 2008. 2009. 2004. 1995. 1996. 1997. 1998. 1999. 2000. 2001. 2002. 2003.

A Challenging future For North American Refiners

E N D

Presentation Transcript

A Challenging future For North American Refiners Alan GelderHead of Downstream Consulting MiamiOctober 26, 2010

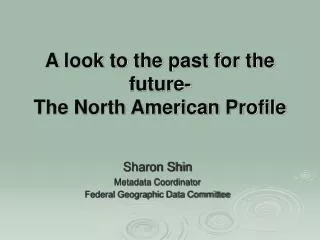

$/bbl 9 8 7 6 5 4 3 2 1 0 2005 2006 2007 2008 2009 2004 1995 1996 1997 1998 1999 2000 2001 2002 2003 Global Composite Margin ($/bbl Nominal) $/bbl Real Refining is a margin business with earnings set by the balance between supply and demand Global Spare Refining Capacity Global Composite Refining Margin Source: BP Stats Review, Wood Mackenzie

The drop in oil demand impacted supply of OPEC heavy crudes, so limiting margin uplift of deep conversion configurations Heavy crude supply has been squeezed by recession Price discount reflects lower refining value Substantial price discount benefited heavy crude refiners 03 – 07 but… … the discount disappeared in 2008 Source: Wood Mackenzie Product Markets Service

Demand has started to recover but it is uneven • Demand is projected to recover by about 2 million b/d in 2010 • And economy allowing should be above pre-recession levels in 2011 • But Europe, N America and OECD Asia are still 6-7% pre-recession levels in 2012 • Demand in Other Regions is 5 million b/d higher in 2012 than in 2007 • Middle distillates a heavy loser during the downturn – but strongest recovery • Fuel oil down -15% • Light ends buoyed by emerging market demand and recovery in naphtha Source: Wood Mackenzie

Mature Markets Mature Markets Emerging Markets Emerging Markets “ “ Weak Weak ” ” GDP GDP “ “ Strong Strong ” ” GDP GDP Aging population Aging population Young populations Young populations +17.3 +18.2 Growing carbon commitment Growing carbon commitment Weaker carbon commitment Weaker carbon commitment Supply security: reduce demand Supply security: reduce demand Supply security: Supply security: access to resource access to resource Weak public finances Weak public finances Growing middle class Growing middle class - - 3.4 2.3 Higher savings rate Higher savings rate Reduced savings rate Reduced savings rate Oil demand will continue to grow but the market is diverging Mn b/d change in demand between 2007 and 2020

Crude Oil Price Outlook is one of continued strength Brent Crude Prices The World “Oil Consumption Expense”* in Relation with GDP

Spare OPEC Productive Capacity declines with growing global oil demand, so supporting high prices Source: Wood Mackenzie

Breakeven Oil Prices for Probable Deepwater and Oil Sands Developments provide a pricing floor to sustain oil supply Source: Wood Mackenzie

Demand in the US and European demand is not projected to retain 2007 levels, so local demand growth is an unlikely saviour.

40 35 30 25 Billion Gallons 20 15 10 5 0 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Any renewable fuel Cellulosic biofuels Biodiesel Other 10% Ethanol 15% Ethanol 20% Ethanol We expect biofuel consumption to increase sharply in the US over the next decade, in response to mandates, though not achieving these entirely Ethanol Share of Gasoline Market, US Possible ethanol blend requirements under the US RFS • In the USA the target is 36 bn gallons of ethanol by 2022, which we also do not expect fully to be met Source: Wood Mackenzie

Mb/d 9.5 9.0 8.5 8.0 7.5 7.0 6.5 2001 2003 2005 2007 2009 2015 1995 1997 1999 2011 2013 Refinery Gasoline Ethanol US gasoline demand recovery is not an “oil” story, as every drop will be met by increased ethanol consumption Source: Wood Mackenzie Product Markets Service

utilisation North America Greater Europe Asia Pacific 95% 90% 85% 80% 75% 70% 2005 2006 2007 2008 2010 2015 Refining runs to remain low in North America and Europe, but improve in Asia due to regional demand growth Source: Wood Mackenzie’s Product Markets Service

Refiners look to heavy crude upgrading to enhance margins but we expect a relative shortage of heavy crude oils… Global incremental heavy crude supply vs. demand – and sensitivity analysis 8 7 ±25% ideal heavy crude demand range 6 5 Impact of maximum possible heavy oil supply upside 4 Change, Mbd 3 2 1 0 -1 -2 2005 2007 2009 2011 2013 2015 2017 2019 Production base case Iran upside Neutral zone upside Kuwait upside Iraq upside Global "demand" change Source: Wood Mackenzie

Deteriorating profitability has brought cancellations to refinery projects globally Delays/cancellations of new refining capacity Source: Wood Mackenzie

kb/d Cumulative New Refineries Cumulative Capacity Expansions Cumulative Non Ref Sup growth Cumulative Demand growth 16,000 14,000 12,000 10,000 8,000 6,000 4,000 2,000 0 -2,000 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 However, demand growth does not catch up with net capacity additions until 2017, so a prolonged period of weak margins are expected. *Excludes capacity creep and utilisation rate changes Source: Wood Mackenzie’s Product Markets Service

Margins can be sustained but at relatively weak levels and only through reduced utilisation - meaning long term pressure on industry ROCE Forecast Source: Wood Mackenzie

NCM, $/bbl MEDIAN EASTERN EXPORTER EUROPEAN REFINERY Low crude Low cost crude Advantaged configuration Product export costs gains MIDDLE freight Efficiency Grassroots projects in Middle East are typically more competitive than many refiners in the OECD markets, so challenging existing sites NCM comparison – New Middle East export refinery vs. European asset Source: Wood Mackenzie Refinery Evaluation Model

Even at peak, downstream earnings were relatively minor within the overall integrated context Source: Companies

Activity in 2010 is a sign that oil majors are reacting to the difficult business environment • CVX - re-focussing on its core Pacific Basin market • Total and Shell - reducing exposure to a declining market and gasoline surplus (disposal of smaller, non core assets but Gonfreville demonstrates ongoing commitment) • Repsol – optimising performance through asset integration and capacity reduction • COP – dealing with loss making asset • Murco – re-focussing on the upstream and limited US downstream interests Source: Wood Mackenzie

Conclusions • Global economic recession dramatically reduced refinery earning potential • Increase in spare refining capacity reduced margins generally and the value of future projects • Reduced fuel oil supply hindered upgrading economics • Tight heavy crude markets limited incentive to process heavy crudes • Recovery in demand growth is expected, led by high growth economies, but recovery in refining sector could be delayed • Legacy capacity investments result in sustained overhang of spare capacity • Upgrading investment will keep heavy crude markets tight • New projects are developing sites that are very competitive on a global perspective • IOC’s are rationalizing their refining portfolio, which provides certain opportunities for other market participants (operators and fuels marketers)

Alan GelderHead of Downstream ConsultingT +1 713 470 1806E alan.gelder@woodmac.com • Alan Gelder joined Wood Mackenzie in 2005 and now leads the Downstream Consulting team. Alan has led consulting assignments all over the world, focusing on major transactions (projects and M&A) and their alignment with key success factors for industry players and third parties. Alan is currently based in Wood Mackenzie’s Houston office. • Alan also has extensive experience of supporting the financial community’s involvement in major projects, such as the Saudi Aramco’s export-oriented mega-Projects, Reliance’s refinery in Jamnagar, India and the Oryx GTL project in Qatar. • Prior to joining Wood Mackenzie, Alan worked for ExxonMobil in a variety of project planning and technical process design roles. His European experience was supplemented by assignments in the United States and Thailand, where he led the technical start up of a major upgrading project in the Sriracha refinery. • Alan has a first class Master Degree in Chemical Engineering from Imperial College, London, which has been supplemented by an MBA from Henley Management College.

Wood Mackenzie Disclaimer • This presentation has been prepared by Wood Mackenzie Inc for delivery at the Energy Buyers Conference during October 2010. It has not been prepared for the benefit of any particular attendee and may not be relied upon by any attendee or other third party. If, notwithstanding the foregoing, this presentation is relied upon by any person, Wood Mackenzie Inc does not accept, and disclaims, all liability for loss and damage suffered as a result. • The information contained in these slides may be retained by attendees. However, these slides and the contents of this presentation may not be disclosed to any other person or published by any means without Wood Mackenzie Inc's prior written permission.

Global Presence Edinburgh London Moscow Calgary Boston France Denver New York Annapolis Beijing Tokyo Houston Seoul Dubai Mexico India Venezuela Kuala Lumpur Singapore Brazil Brisbane Perth Sydney Argentina Wood Mackenzie Offices Associates & Partners

Research Coverage Across The Value Chain ENERGY MARKETS SERVICE MACRO OILS SERVICE UPSTREAM SERVICE PATHFINDER GRV OPAL GLOBAL OIL SUPPLY SERVICE GLOBAL PRODUCTS OUTLOOK EXPLORATION SERVICE GLOBAL ECONOMIC MODEL DOWNSTREAM ONLINE RADAR CORPORATE ANALYSIS TOOL PVT GAS & POWER SERVICE GLOBAL LNG ONLINE GLOBAL GAS MODEL PRISM COAL SUPPLY STUDIES

Wood Mackenzie’s Research Product Suite UPSTREAM COAL M&A Service • Coal Supply Service • Coal Market Service • Coal GEM Upstream Service GAS & POWER MACRO ENERGY Exploration Service • Gas & Power Service • Gas & Power Tool • Power Valuation Tool Energy Markets Service Global Economic Model • LNG Service • LNG Tool • LNG GEM Macro Oils Service PathFinder Executive Briefing Service Global Gas Model Corporate Analysis Tool Carbon Service DOWNSTREAM Corporate Service METALS AND MINING Corporate Benchmarking Tool Downstream Oil Service • Cu, Zn, Pb, Al, Ni, Au, Ag • Metal Markets Service • Concentrate Service • Cost Services for mines, smelters • & refineries Product Markets Service Global Oil Supply Tool Unconventional Gas Service Refinery Evaluation Model

Wood Mackenzie Kintore House 74-77 Queen Street Edinburgh EH2 4NS Global Contact Details Europe +44 (0)131 243 4400 Americas +1 713 470 1600 Asia Pacific +65 6518 0800 Email energy@woodmac.com Global Offices Australia - Canada - China - Japan - Malaysia - Russia - Singapore - South Africa - United Arab Emirates - United Kingdom - United States Wood Mackenzie has been providing its unique range of research products and consulting services to the Energy industry for over 30 years. Wood Mackenzie provides forward-looking commercial insight that enables clients to make better business decisions. For more information visit: www.woodmac.com