Purchase Lot

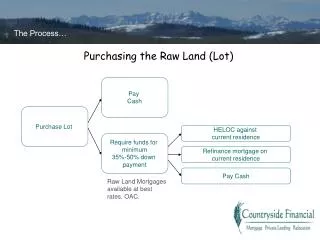

The Process…. Purchasing the Raw Land (Lot). Pay Cash. Purchase Lot. HELOC against current residence. Require funds for minimum 35%-50% down payment. Refinance mortgage on current residence. Pay Cash. Raw Land Mortgages available at best rates. OAC. The Process….

Purchase Lot

E N D

Presentation Transcript

The Process… Purchasing the Raw Land (Lot) Pay Cash Purchase Lot HELOC against current residence Require funds for minimum 35%-50% down payment Refinance mortgage on current residence Pay Cash Raw Land Mortgages available at best rates. OAC.

The Process… Building A New Home + 15% Foundation/Backfill (Land paid out if mortgaged) Hire Builder Builder can self-finance + 40% Lockup Builder requires draws Own lot & ready to build a new home Draw Mortgage/ Progress Advances + 65% Drywall/Services + 85% Kitchen cupboards; doors; bathrooms Self-Build Client requires draws + 100% Take-out Client can self-finance Insured: 4 Draws Allowed If 15% is drawn, then the 85% draw is not available – it is an either/or to a maximum of 4. Conventional files may allow more. * Costs may increase depending on each builder’s expectations, deposits and upfront costs. Important to note… 10% holdbacks are required against all draw mortgages as per Section 18(1) of the Builders Act. * Lender/Broker mortgage fees may apply. If applicable, will be determined and disclosed at start of mortgage process. * Interest rates vary – OAC; subject to income, credit history and property.

The Process… Home is Complete – Take-Out Mortgage (pays back the draw lender) and begins a new traditional loan Take-out mortgage OAC Clients continue with their usual bank Home is done and you’re are ready to move in! Best discounted rates/terms available; products for all client situations Take-out mortgage with Countryside Financial OAC Additional rate reductions available Exceptional specialized service and knowledge provided At time of take-out, the loan may be increased to a higher loan-to-value or rolled over from the progress advance. Clients may choose to pay themselves back some capital and take out additional equity. The loan turns into a ‘traditional mortgage’ and all mortgage products become available OAC.

Other Considerations… Potential Costs to Client DescriptionFees ApplicableMortgage Available & Rates Raw Land Purchase - Lender & Broker Fee’s may apply - 65% LTV maximum; open or closed mortgage. - Legal & Appraisal - Best rates available. Progress Advance Mortgage - Lender & Broker’s Fee’s may apply - 95% LTV maximum for insured build; 80% - Legal & Appraisal LTV maximum for conventional build (may be subject - Appraisal/Inspections at each draw to sliding scale). - Best rates available. Take Out Mortgage - Legal & Appraisal - 80% LTV for refinance. - Best rates available. * All above on-approved-credit. Lender and Broker Fees may increase with credit risk. CMHC (if applicable) premium on top. Legal Costs $800 up to $1500 + Appraisal Costs $500 + for each as required $500 + for take-out mortgage to confirm market value and fully constructed Progress Inspections $150 + for each as required to confirm percentage complete at each draw Hold Backs 10% As per Alberta building guidelines, holdbacks are required for a period of 45 days at end of construction period. The % is based on each draw and will be held back by your lawyer.