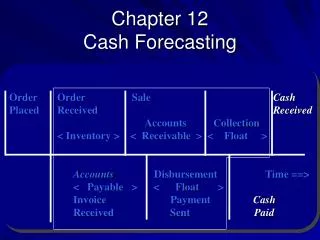

Chapter 12 Cash Forecasting

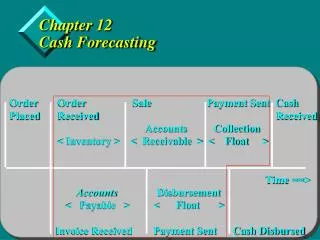

Chapter 12 Cash Forecasting. Order Order Sale Payment Sent Cash Placed Received Received Accounts Collection

Chapter 12 Cash Forecasting

E N D

Presentation Transcript

Chapter 12Cash Forecasting • Order Order Sale Payment Sent Cash • Placed Received Received • Accounts Collection • < Inventory > < Receivable > < Float > • Time ==> • AccountsDisbursement • < Payable > < Float > • Invoice Received Payment Sent Cash Disbursed

Learning Objectives • Explain importance of short-term cash forecasts. • Indicate why the monthly cash budget is important to top management, and specify the two objectives for its development. • Indicate how daily cash forecasting differs from monthly forecasting. • Explain the receipts and disbursements, pro forma balance sheet, and distribution methods of cash forecasting.

Forecasting Monthly Cash Flows • Importance to top management • Monthly cash forecast objectives • Forecasting philosophy • Forecast parameters • Statistical tools (Appendix A & B)

Importance to top management • Useful planning tool • Typical billing and payment cycle is monthly • Monthly interval is adequate for funding requirements – quarter is too long • Alerts management to threats

Monthly cash forecast objectives • Accuracy • Avert overdrafts, determine credit lines, aid in selection of investment maturities • Usefulness • Too much or too little detail is expensive • Need variance as well as mean

Forecasting Philosophy • Number and type of forecasts • Short, intermediate, long range; daily, monthly, quarterly, annual. • Expenditure on forecasts • Function of CF variability • External versus internal forecasts • Quantitative versus judgmental forecasting

Forecast Parameters • Forecast horizon • Variable identification • Modeling the cash flow sequence • Format of the receipts and disbursement forecast • Interpreting the receipts and disbursement forecast • Developing the receipts and disbursement forecast • Modified accrual method • Pro forma balance sheet method • Model estimation • Model validation

Forecast Parameters • Forecast horizon • How far into the future are we forecasting • Variable identification • Short horizon needs greater detail • Modeling the cash flow sequence • Receipts and Disbursements method • Modified accrual • Pro Forma Balance Sheet

Receipts and Disbursements method • Accuracy declines beyond one month • Format of the receipts and disbursement forecast – see page 421 • Interpreting the receipts and disbursement forecast • Credit lines may be prearranged to cover anticipated shortfalls • Project surplus amounts and durations for investment • May help to establish a target cash balance • Developing the receipts and disbursement forecast • Obtain sales forecast (distribution is better) • Project cash receipts • Project cash disbursements

Modified accrual method • Simplest form: • Strength is ease of implementation and relative accuracy for intermediate forecasts • Weakness is lack of detail to ensure accuracy for short term forecasts

Pro forma balance sheet method • Use percent of sales to forecast • Notes payable may be used as “plug” number • aLess cash and marketable securities • Generally more useful for longer periods than a month

Model estimation • See appendix A and B • Sensitivity • Simulation

Forecasting Daily Cash Flows • Horizon • Variable identification • Modeling the cash flow sequence • Structuring the daily cash forecast • Distribution method • Model estimation • Model validation

Forecasting Daily Cash Flows • Horizon • Historical data may be projected using proper techniques, but a lot of “known” data is included • Variable identification • Rule-of-thumb: the shorter the horizon the greater the detail • Modeling the cash flow sequence • Relies less on statistics and more on known timing of cash flows • Structuring the daily cash forecast • A few (generally) known major flows and many small flows

The Distribution Method • Cash flows are not evenly distributed throughout the week or the month • Disbursement Example: • Where: • CD = Cash Disbursement • MDF = Month’s disbursement forecast • See page 430 and appendix B

Summary • The chapter began with a discussion of the philosophy and environment within which cash forecasts are made. • The value of forecasts is to borrow less or extend investment maturities. • The two major cash forecasting time intervals (monthly and daily) were presented and the processes for variable identification, modeling the cash flow sequence, model estimation, and model validation discussed.