Download

1 / 18

810 likes | 1.84k Vues

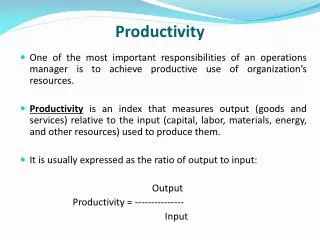

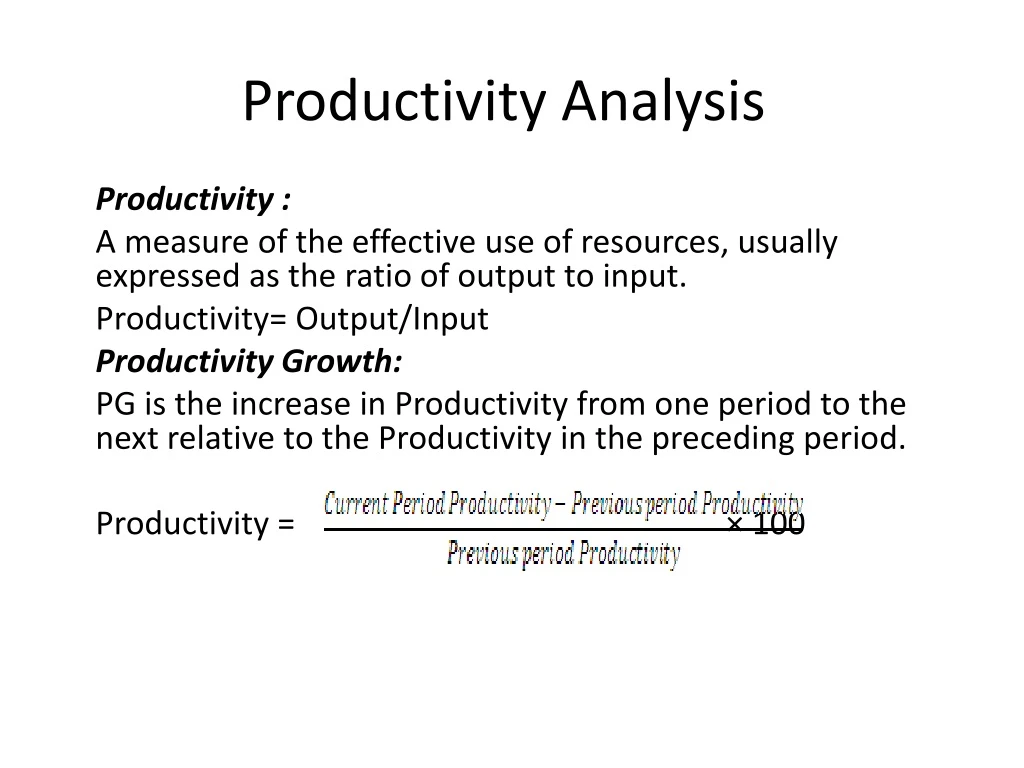

Productivity Analysis. Productivity : A measure of the effective use of resources, usually expressed as the ratio of output to input. Productivity= Output/Input Productivity Growth:

E N D

Productivity Analysis Productivity : A measure of the effective use of resources, usually expressed as the ratio of output to input. Productivity= Output/Input Productivity Growth: PG is the increase in Productivity from one period to the next relative to the Productivity in the preceding period. Productivity = × 100

Computing Productivity….. • Productivity is the ratio of output to input • For example, a firm that spends five days to manufacture 100 units has a productivity of 20 (100 units/5 days) units per day • A measure of productivity can either be operational or financial in nature • Operational productivity is the ratio of output units to input units (both physical measures) • Financial productivity is also a ratio of output to input, except that either the numerator or denominator is a dollar amount

Partial vs. Total Productivity A productivity measure may include all production factors or focus on a single factor or part of the production factors that the firm uses in manufacturing • A partial productivity measure focuses on the relationship between one input factor and the output attained • Examples include direct materials (DM) productivity, workforce productivity, and process productivity • A total productivity measures includes all input resources used in production

Partial Productivity Partial productivity measures are important because changes in the productivity of different resources do not always occur in the same direction or at an equal rate We will use Erie Precision Tool Company as an example Erie Precision Tool Company manufactures drill bits, and its operating information for 2006 and 2007 is provided (see next slide)

Partial Productivity (continued) Erie Precision Tool Company 2006 and 2007 Operating Data for DB2 20072006 Units of DB2 manufactured and sold 4,800 4,000 Total sales (price is $500) $2,400,000 $2,000,000 Direct materials (32,000@$25; 25,000@$24) 800,000 600,000 Direct labor (4,000@$50; 4,000@$40) 200,000 160,000 Other operating costs 300,000 300,000 Operating income $ 1,100,000 $940,000 Sales increased by 20%, but income increasedby only 17%. Did productivity decline?

Partial Productivity (continued) 4,800 units ÷ 32,000 pounds 4,000 units ÷ 25,000 pounds 4,800 units ÷ 4,000 hours 4,000 units ÷ 4,000 hours

Partial Productivity (continued) 4,000 units ÷ $600,000 4,800 units ÷ $800,000 4,000 units ÷ $160,000 4,800 units ÷ $200,000

Partial Productivity: Summary Analysis • The partial operational productivity measure for DM decreased while the partial operational productivity measure for DL increased • Partial financial productivity measures for both DM and DL decreased • The discrepancy between the DL measures suggests that although employee productivity/hr. increased, the cost increase due to higher hourly wages more than offset the gain in productivity/hr.

Operational vs. Financial Productivity Measures • Operational productivity measures • Use physical measures, which are easier for operational personnel to understand • The measures are unaffected by price changes and other factors, which makes them easier to benchmark • Financial productivity measures • Considers the effect of cost (major concern for management) and quantity of an input resource on productivity • Can be used in operations that use more than one production factor

Limitations of Partial Productivity • Measures only the relationship between an input resource and the output; ignores any effect that changes in manufacturing factors have on productivity • Ignores any effect that changes in other production factors have on productivity, such as an increase in material quality • Fails to include effects that changes in the firm’s operating characteristics have on the productivity of the input resources, such as installation of high-efficiency equipment • An improved partial productivity does not necessarily mean the firm or division operates efficiently

Total Productivity • Total productivity is a financial measure that compares output to the total cost of all input resources used to produce the output • Computation of total productivity involves three steps: • Determine the output of each period • Calculate the total variable costs incurred to produce the output • Compute “total productivity” by dividing the amount of output by the total cost of variable input resources

Total Productivity (continued) Once again using Erie Precision Tool Company.... Erie Precision Tool Company Total Productivity for DB2 Total productivity in units 20062007 (a) Total units manufactured 4,000 4,800 (b) Total variable manufacturing costs incurred $760,000 $1,000,000 (c) Total productivity: (a) ÷ (b) 0.005263 0.004800 (d) Decrease in productivity: 0.005263 – 0.004800 = 0.000463 0.000463 ÷ 0.005263 = 8.8%

Total Productivity (continued) Erie Precision Tool Company Total Productivity for DB2 Total productivity in sales dollars 20062007 (a) Total sales $2,000,000 $2,400,000 (b) Total variable manufacturing cost incurred $760,000 $1,000,000 (c) Total productivity: (a) ÷ (b) $2.6316 $2.4000 (d) Decrease in productivity: $2.6316 – $2.4000 = $0.2316 $0.2316 ÷ $2.6316 = 8.8%

Benefits and Limitations of Total Productivity • Total productivity measures the combined productivity of all operating factors, which decreases the possibility of managers manipulating some manufacturing factors to improve productivity measures for others • Personnel at the operational level may have difficulty linking the results to day-to-day operations • Deterioration in total productivity can result from costs of resources that are beyond the manager’s control

Benefits and Limitations of Total Productivity (continued) • The basis for assessing changes in productivity could vary over time a constant base-year is suggested • Productivity measures often ignore the effects on productivity of changes in demand for the product, changes in selling prices of the goods or services, and special purchasing or selling arrangements • Changes in demand alter the size of operations and productivity measures (but not necessarily productivity itself) • Receiving or offering a discount in price can alter total and partial productivity measures without affecting productivity

Multifactor Productivity • Determine the Multifactor Productivity for the combined input of lobor and machine time using the following data: • Output: 7040 units @$1.10 each • Input: • Lobor:$1000 • Materials:$520 • Overhead:$2000 • Multifactor Productivity= = = 2.20 units per dollar input

Factor that Affect Productivity • Numerous factor affect productivity. Generally the are methods, capital, quality, technology and management. • Standardizing • Scrap rate • Layoff • Labor turnover • Design of the work place • Incentive plan

Improving Productivity • Develop productivity measurement • Bottleneck Operation • Develop method • Establish reasonable goals for improvement • Reward workers for contribution • Measure improvement and publicize.