Timing Risk Can Impact Your Financial Plan

100 likes | 185 Vues

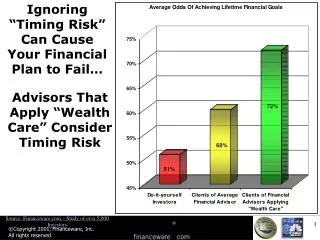

Many investors disregard timing risk, unaware that it can cause financial plans to fail in the long run. Advisors who prioritize "Wealth Care" consider timing risk alongside wealth goals. Learn how ignoring this risk can affect your future and why a customized plan with growth allocation may be more beneficial. Source: financeware.com study of over 5,000 investors.

Timing Risk Can Impact Your Financial Plan

E N D

Presentation Transcript

Ignoring “Timing Risk” Can Cause Your Financial Plan to Fail… Advisors That Apply “Wealth Care” Consider Timing Risk Source: Financeware.com – Study of over 5,000 Investors

If You Have No Goals, If You Aren’t Saving or Spending Money, You Can Ignore Timing Risk Does This Describe You?No Savings?No Spending?No Taxes? If So, Then Timing of Returns Makes NO DIFFERENCE

But Most Investors Have REAL Goals Some Are Distributing Wealth… Better To Have The Bull Market Early Or… We Could Assume There Are No Bull or Bear Markets… It Should Be Close Enough! Rather Than Later…

And Some Are Accumulating Wealth It Hurt To Have The Bull Market Early Or… We Could Assume There Are No Bull or Bear Markets… It Should Be Close Enough! Rather Than Later…

Can Wealth Forecasts Based On Assuming The Same Return Each Year Really Be That Far Off? Harry - 56 Year Old, Retiring at 65- Projected Portfolio Values at age 95: Assumed Return of 11.78%EACH YEAR: $11.3 Million Market Reality: Actual Market at 11.78% (’60-’98): Actual Market at 12.12% (’61-’99): Actual Market at 8.78% (’36-’74): Broke @ Age 88Broke @ Age 95$2.6 Million What Do You Think The Results Will Be If We Simply Use The Actual Returns In The Order They Actually Occurred?

Being “More Conservative” In Our Assumed Return Doesn’t Really Help Harry - 56 Year Old, Retiring at 65- Projected Portfolio Values at age 95: Assumed Return of 9.91%: $2.2 Million Market Reality: Actual Market at 9.91% (’30-’68): Actual Market at 8.78% (’36-’74): Actual Market at 12.12% (’61-’99): Broke @ Age 78$2.6 MillionBroke @ Age 95 Ignoring This Risk is leaving your future to the flip of a coin…

This is how Monte Carlo analysis can help you understand your odds Most plans assume you will achieve the AVERAGE return each year and IGNORE Bull & Bear markets. With probability analysis, we project many results including both Bull & Bear Markets.

By running these tests we can then forecast your “odds” of success Having never done this analysis, your current odds of success may not be very good

Aggressive Growth Allocation Growth Allocation But, while most advisors simply increase the return & risk… Adjusting your asset allocation may not be the best choice in meeting your objectives…

Aggressive Growth Allocation Growth Allocation Sometimes less risk is better… “Customized” Plan withGrowth Allocation We can customize your plan to meet your goals without necessarily increasing risk