Download

1 / 42

420 likes | 580 Vues

Predictive Models of Realized Variance Incorporating Sector and Market Variance. Haoming Wang April 16 th 2008. Motivation. We’ve seen that the realized variance of equities exhibits correlation with lagged daily, weekly, and monthly realized variance.

E N D

Predictive Models of Realized Variance Incorporating Sector and Market Variance Haoming Wang April 16th 2008

Motivation • We’ve seen that the realized variance of equities exhibits correlation with lagged daily, weekly, and monthly realized variance. • We know that equity returns are also correlated with market returns, what kind of correlation do equity variance levels have with market variance levels? • Further, it’s intuitive that the returns of individual equities are also correlated with the returns of companies in their own sector. What kind of correlation should we see with sector volatilities? • Examined regressions for pharmaceuticals and banks in the S&P 100.

Pharmaceutical Stocks • There are five companies in the S&P 100 classified as in the “Major Drugs” sector. • ABT – Abbott Labs • BMY – Bristol Myers Squibb • JNJ – Johnson & Johnson • MRK – Merck • PFE - Pfizer

Bank Stocks • Six companies in S&P 100 classified as money center banks. • BAC – Bank of America • BK – Bank of New York-Mellon • C – Citigroup • JPM – JP Morgan Chase • USB – US Bancorp • WFC – Wells Fargo

Motivation for Stock Choices • Want to choose two industries that were pretty different to see if my results weren’t just unique to the pharmaceuticals industry. • The bank industry and the pharmaceuticals industry seemed pretty different from each other. • Five pharmaceutical stocks have an average beta factor of 0.652. • Six bank stocks have an average beta factor of 0.945.

Background Mathematics • Realized variation (where rt,j is the log-return): • Realized sector variation: An average of daily realized variation for same sector stocks in the S&P 100 excluding whichever stock is being regressed. • Realized sector portfolio variance: average of daily stock prices is used as the price of the portfolio.

Background Mathematics • Realized variation (where rt,j is the log-return): • Realized semi-variance (where 1 is the indicator function that the return is negative) :

Background Mathematics • Further, according to BNKS, the realized semi-variance converges to half the bipower variation plus negative squared jumps, or:

HAR-RV Model • The multi-period normalized realized variation is defined as the average of one-period measures, or: • The daily hetereogeneous autoregressive realized variance (HAR-RV) model of Corsi (2003) is used with daily, weekly, and monthly periods:

HAR-RV Model • The above regression is for day ahead predictions, also looked at week-ahead and month-ahead regressions. • Finally, I looked log-log regressions, where the natural log of realized variance is regressed on the natural log of the regressors. • This gives an intuitive meaning: a 1% change in the regressors implies a β% change in the dependent variable.

Extended HAR-RV model • Added sector variance for daily, weekly, and monthly periods. • For example, the RV of PFE would be regressed on the average RV of ABT, BMY, JNJ, and MRK. • What happens when PFE RV is also included in the average? • The standard errors and R-squared remain the same; however, the interpretation is not as clear. • Further, the interpretation is trickier since the stock coefficient is incorporated into the sector coefficient. • Also included the RV of the S&P 500.

Sector As A Portfolio? • Investigated constructing a portfolio of the industry. • Across the board there’s higher standard errors and lower R-squared. • I decided to stick with using an average of the sector’s realized variance.

Data Range • Data for all 11 stocks and the S&P were gathered from 1997 to 2007. • 2606 trading days worth of observations for pharmaceuticals stocks. • 2519 trading days worth of observations for the bank stocks.

Results • We’ll focus on two companies: Johnson & Johnson (JNJ) and JP Morgan (JPM), one for each sector. • I’ve picked these two out because they show the greatest benefit from the inclusion of more regressors, but I’ll include averages as well.

Analysis • We see marked increases in the explanatory power of the regression model, with the greatest improvement in the weekly predictions. • This makes intuitive sense: it should be easier to predict smoothed out variance measures. • This is in line with the level of the R-squared: we have the highest level of R-squared in the weekly predictive model. • Seems intuitive that the model with the highest explanatory power should also see the most improvement.

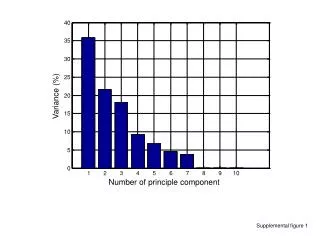

Analysis • In the pharmaceuticals sector, we see an average increase in R-squared of 5.12% for daily predictions, 5.80% for weekly predictions, and 6.41% for monthly predictions. • In the banking sector, we see an average increase in R-squared of 6.24% in daily predictions, of 6.83% for weekly predictions, and 3.41% for monthly predictions.

Analysis • In all regressions we see that the lagged daily sector variance is strongly significant. • There are clear sector effects at work, although only the previous day sector RV seems to play a consistently statistically significant role. • However, sector regressors are jointly significant for all time horizons. • While the p-values for the sector regressors remains at around the same level, it’s interesting to note that for JNJ the S&P regressors become much more significant as the horizon increases, perhaps suggesting that market effects play out in a longer time-frame for JNJ.

Analysis • The S&P coefficients are harder to interpret: there are no clear patterns in significance, although daily and monthly S&P regressors seem to be significant for JNJ, however, there is still the weirdness of negative coefficients. • JPM is especially strange because the sign of the monthly S&P lag flips signs. • From looking at semi-variances, this seems to be driven by high upward semi-variance. • However, we do have a pretty clear pattern: the previous day’s sector RV does seem to be an important driver of realized variance.

Analysis • Increasing the time horizon also doesn’t seem to solve the problem of the negative monthly coefficients. • I’ll talk about this later, but what effect does the time-frame have on the model’s coefficients? • I plan on investigate this further for next semester.

Analysis • It’s also interesting to note that even with the inclusion of the S&P and sector, we still see the same-stock daily lags decreasing in importance as the time horizon increases and the monthly lags increasing in importance. • Further, the weekly lag seems to be relatively unimportant. It seems that the most important drivers are the short term and the long term. • For JNJ we see some intuitive results for the sector and the stock: the lagged daily effects grow weaker as the prediction horizon increases and the monthly effects are stronger.

Analysis • It’s interesting to note the patterns in RV predictions. • Regression models with sector and S&P realized variance seem to have much greater ability to exhibit spikes in realized variance. • This makes intuitive sense: it’s likely that events which cause spikes in volatility for the market or the sector to be associated with spikes in a specific stock.

Analysis • It’s also interesting to note trends in realized variance over this data set. The first graph is from about 1999-2001 and the second graph is from 2006-2008. • Day ahead predictions seem close for both time periods. • However, for the early part of 2006-2008 (pre-credit crisis) the model consistently over-predicts week ahead and month ahead realized variance. • It seems that 2006-2007 was a period of below average volatility in the market. • It would be interesting to see how the model changes for different periods of data corresponding to different volatility regimes.

Extensions For Next Semester • Breaking up realized variance into continuous and jump components for both the sector and stock:

Extensions For Next Semester • Including the sector and S&P realized variances seems to increase the prediction of spikes in realized variance, it would be interesting to see how the inclusion of jumps as regressors changes these dynamics. • Further investigation using semi-variance of the negative coefficient in monthly lags.