Oligopoly

Explore oligopoly characteristics, interdependence among firms, game theory strategies, kinked demand curve models, and assessment of oligopoly in the market. Learn about stable prices, firm strategies, and the implications of kinked demand curves. Dive into the world of oligopoly dynamics and decision-making strategies in a few-firm market structure.

Oligopoly

E N D

Presentation Transcript

Oligopoly Topic 7(b)

OLIGOPOLY Contents 1. Characteristics 2. Game theory 3. Oligopoly Models: a. Kinked Demand Curve b. Price leadership c. Collusion d. Cost-plus pricing 4. Assessment of Oligopoly

Oligopoly • In this topic we will consider the behaviour of firms when the industry is made up of only a few firms: oligopoly. • A crucial feature of oligopoly is the interdependence between firms’ decisions.

Interdependence between firms • In oligopoly, the industry is made up of only a few firms. • Each of these firms makes up a significant part of the total market. • Each can exercise some market power (eg. their output decisions influence the market price). • Therefore, each firm’s decisions influence the decisions made by the other firms. • In other words, firms’ decisions are interdependent.

Characteristics of Oligopoly • Small mutually interdependent number of firms controlling the market • Significant market power • One firm cut the prices => others are affected • Homogenous or differentiated products • High barriers to entry • Examples

Non-price competition… • is common in oligopoly, such as: • advertising, product innovation, improvement of service to customers. • is preferred to price wars which usually bring losses to all parties.

2. Game Theory • A model of strategic moves and countermoves of rivals. • Firms chooses strategies based on their assumptions about competitors likely behaviour or response. • Strategies could relate to pricing, advertising, product range, customer groups etc. • Game theory provides a framework or model to help analyse this behaviour.

2. Game Theory – a two-firm Payoff matrix • Two airlines competing for the domestic air travel market • Vietnam Airlines • Jetstar • Assume two airlines choose their strategy independently (ie. No collusion) • Payoffs are the outcomes (or profits) for the 2 firms for each combination of strategies.

2. Game Theory – MAXIMIN strategy • Firms maximise the minimum expected payoff. • For Vietnam Airlines: • if they choose a Low Fare option, they will receive either $8m or $20m profit, depending on the option chosen by JS – so the worse VA will make $8m profit. • If they choose a High Fare option, they will receive either $5m or $15m – the worse is $5m profit • The maximum (the best) of these two minimums is $8m, so VA will choose the Low Fare option.

2. Game Theory – MAXIMIN strategy • For Jetstar: • if they choose a Low Fare option, they will receive either $8m or $20m profit, depending on the option chosen by VA – so the worse Jetstar will make $8m profit. • If they choose a High Fare option, they will receive either $5m or $15m – the worse is $5m profit • The maximum (the best) of these two minimums is $8m, so JS will also choose the Low Fare option. • Both firms choose the Low Fare option if act independently. • There is an incentive to collude

2. Game Theory – MAXIMIN strategy • For VA: • Low Fare: Min. $10m profit ; Max. $15m profit • High Fare: Min. $12m profit; Max. $20m profit => VA choose High Fare option • For JS: • Low Fare: Min. $5m profit; Max. $8m profit • High Fare: Min. $2m profit; Max. $10m profit => JS choose Low Fare option Possibly, they cater for different market segments. There is no incentive to collude

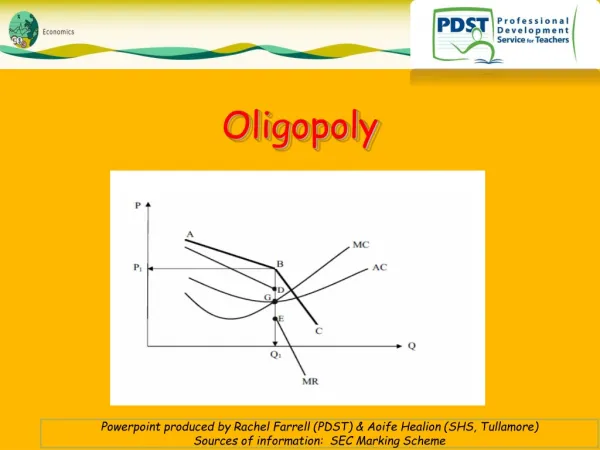

3. Oligopoly ModelsKinked Demand Curve Model • D1: When the firm changes prices => other firms react similarly • There is no substitution effect • demand will change but not by much • demand is price inelastic • D2: When the firm changes price => other firms don’t follow. • There is substitution effect • Change in demand more sensitive to price changes • Relatively elastic curve Rivals ignore Rivals match

Kinked demand curve for a firm under oligopoly $ • Assumptions: • Independent among firms (ie. no collusion) • Rivals will match price decreases and ignore price increases A B P1 D Q O Q1 fig

The MR curve $ B P1 MR a D = AR Q O Q1

The MR curve $ P1 a D = AR b Q O Q1 MR

As long as MC shifts within C1 & C2, the optimum output is Qo & price is Po => stable price 3. Oligopoly ModelsKinked Demand curve

Stable price under conditions of a kinked demand curve $ MC2 MC1 P1 a D = AR b Q O Q1 MR

Kinked Demand Curve Model • Assumptions: • All firms are independent (ie. no collusion) • Rivals match price decreases and ignore price increases • Implication of Kinked Demand Curve: Stable Price • If a firm raises price, it will lose customers and sales to other firms • If it reduces price, other firms will match => a price war. • Therefore, firms tend to maintain the same price. • Substantial cost changes will have no effect on output and price as long as MC shifts between C1 & C2. Another reason why price is stable. • Limitations • It does not explain the determination of current price • Sometimes prices rise substantially during inflation period, which is contrary to the stable price conclusions of Oligopoly

3. Oligopoly Modelsb)Price Leadership Model • Assumes implicit collusion • Follow the leader • dominant firm makes prices changes • most efficient, oldest, most respected, largest • others follow • Usually • prices don’t change very often • price changes are very public • price may be low to act as barrier to entry

Price leader aiming to maximise profitsfor a given market share $ AR = Dmarket O Q fig

Price leader aiming to maximise profitsfor a given market share $ Assume constant market share for leader AR = Dmarket AR = Dleader O Q fig

Price leader aiming to maximise profitsfor a given market share $ AR = Dmarket AR = Dleader MRleader O Q fig

Price leader aiming to maximise profitsfor a given market share $ MC AR = Dmarket AR = Dleader MRleader O Q fig

Price leader aiming to maximise profitsfor a given market share $ MC l PL AR = Dmarket AR = Dleader MRleader O QL Q fig

Price leader aiming to maximise profitsfor a given market share $ MC l t PL AR = Dmarket AR = Dleader MRleader O QL QT Q fig

3. Oligopoly Models c) Collusion • Definition: when an industry reaches an open or secret agreement to • fix price • divide up or share the market • or other ways of restricting competition b/w themselves.

3. Oligopoly Models c) Collusion Why collude? • removes uncertainty • no price wars • increase profits • barrier to entry • Types of collusion • Explicit • centralised cartel (OPEC) • Implicit • price leadership model

Collusion (contd.) • Difficulties: • Difference in cost structures • Large number of firms in the market • Cheating • Falling demand • Legal barriers

3. Oligopoly Modelsd) Cost-plus pricing • Also known as “mark-up” pricing • Price = unit cost + a margin (%) • Example: the unit cost of washing machines is $200 plus a 50% mark-up => Price = $300. • If producers in an industry have roughly similar costs, then the cost-plus pricing formula will result in similar prices and price changes. • Therefore, Cost-plus pricing is consistent with collusion and price leadership.

4. Assessing oligopoly • Negatives: • P > MC : no allocative efficiency • P > min. AC : no productive efficiency • Collusion • Positives: • Economies of scale • Innovation