Download

1 / 40

400 likes | 433 Vues

Explore the loanable funds market, interest rates, and inflation's impact on borrowing and saving. Learn about factors shifting supply and demand, and how the market model is applied efficiently. Discover the interplay between borrowers and savers, and how interest rates influence investment decisions.

E N D

22 Savings, Interest Rates, and the Market for Loanable Funds

Previously • CPI is the foundation of inflation calculation • Computation can be difficult because the typical “basket” of consumer goods changes over time • The BLS tries to adjust for this • Inflation is often misunderstood by the general public • There are several macroeconomic costs from inflation • Inflation is caused and controlled by expansions of a nation’s money supply

Big Questions • What is the loanable funds market? • What factors shift the supply of loanable funds? • What factors shift the demand for loanable funds? • How do we apply the loanable funds market model?

The Loanable Funds Market—1 • Loanable funds market • Includes such places as: • stock exchanges • investment banks • mutual fund firms • commercial banks • Borrowers use funds for businesses • Savers lend to businesses

Production Timeline:Firms Need to Borrow Firms need to borrow before production begins. That is why the loanable funds market is so important. Prepare to Produce Produce Sell Output Borrow $$ Build Capital Goods Hire Workers Repay Loans $$ Pay Workers $$ Time Today Future Periods

Notes about Borrowing • Every dollar borrowed requires a dollar saved • Lenders can’t lend money they don’t have • Savings provides funds for lenders to lend • Chain of borrowing: Savings → Borrowing → Investment → GDP • The loanable funds market makes this process efficient

Interest Rates • Interest rate • The price of loanable funds • Savers: the reward for saving • Borrowers: the cost of borrowing • Like other prices, it rises and falls • Affected by supply and demand • We can examine this market like any other market

Interest Rates and the Supply of Loanable Funds • When you save money, you are supplying funds. • The price you receive in return is the interest • Percentage (rather than dollars) • Example: • Interest rate = 3% per year • $500 ×0.03 = $15 • Saving $500 will pay $15 for the year • Loanable funds “law of supply” • The quantity of savings rises when the interest rate increases

Higher Interest Rates Yield Greater Future Returns This table represents the future value of $500 in savings at different interest rates. The interest rate is a reward for saving money.

Practice What You Know—1 • Where does the supply of funds in the loanable funds market come from? • Banks printing money • Firms borrowing money for investment • Government tax revenues from citizens • Consumers saving their money at banks

Interest Rates as a Cost of Borrowing • Interest rate on the demand side • Interest rate is the cost of borrowing • When should a firm borrow? • Do a cost-benefit analysis • Borrow funds if: Expected return on investment > Interest rate on loan

Practice What You Know—2 • The interest rate can be thought of as: • the rate at which banks loan funds. • the return on a capital investment. • the real rate of inflation. • the price of money.

Inflation and Interest Rates • Real interest rate • The interest rate corrected for inflation • Nominal interest rate • The interest rate before it is corrected for inflation • Fisher equation • Relates inflation to the real and nominal interest rate

Quick Summary • Supply of loanable funds • Comes from people saving money • Interest rate is a reward for saving • Demand of loanable funds • Comes from people wanting to borrow money • Interest rate is the cost of borrowing

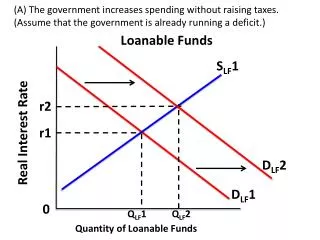

What Factors Shift the Supply of Loanable Funds? • Movement along the supply curve for loanable funds • Caused by a change in the interest rate • Shiftin the supplyof loanable funds is caused by • Changes in income and wealth • Changes in time preferences • Consumption smoothing

Shifts in the Supply of Loanable Funds—1 • Changes in income and wealth • Increases in income generally increase savings • Time preferences • People generally prefer goods sooner rather than later, and funds are no different

Time Preferences—1 • Time preferences are not uniform across individuals and societies • Less patient people prefer now to later and will save less • Time preferences help determine the savings rate

Time Preferences—2 • Application: Decision to attend college • Option 1: Get a job • Earn income immediately • Consume now • Option 2: Go to college • Forego current income and consumption • Higher future income and consumption

Practice What You Know—3 • How will an increase in time preferences affect the loanable funds market? There will be a(n): • increase in the supply of loanable funds. • decrease in the supply of loanable funds. • increase in the demand of loanable funds. • decrease in the demand of loanable funds.

Shifts in the Supply of Loanable Funds—2 • Consumption Smoothing: • No large changes in consumption with changes in income • Income changes over the course of the typical lifetime

Practice What You Know—4 • In the basic consumption-smoothing model, when are consumers dissaving? • During prime earning years • In their 20s and 30s • Very early in life • Late in life

Demand for Loanable Funds • Demanders of loanable funds are borrowers • Demand is driven largely by firms that need to borrow for large capital projects • Governments also borrow • Recall: • Borrowing must occur to build capital goods • This occurs before any production of final goods

What Factors Shift the Demand of Loanable Funds? • Movement along the demand curve for loanable funds • Caused by a change in the interest rate • Shift in the demand of loanable funds caused by • Changes in the productivity of capital • Changes in investor confidence

Shifts in the Demand for Loanable Funds—1 • Productivity of capital • If capital becomes more productive, the demand for loans will increase • The returns on investment (at any interest rate) will be greater • Example: Internet and computers • Investor confidence • If a firm is optimistic, it will borrow more today • Changes in capital productivity and investor confidence will shift the demand for loanable funds

Equilibrium in the Market for Loanable Funds—2 • In equilibrium: Savings = Investment • Supply of loanable funds is savings • Demand for loanable funds is firms wanting to borrow • Relationship between saving and borrowing • Every dollar borrowed requires a dollar saved

Practice What You Know—5 • What is true about equilibrium in the market for loanable funds? • Savings = Investment • Interest rate = Inflation • Investment = Interest Rate • Savings = GDP

Decline in Investor Confidence—1 • Investor confidence tends to decline when the economy slows • Firms expect reduced sales, and investors expect lower returns on their investments • Model predicts that this will result in a lower level of investment and a lower interest rate • Investment fell during both U.S. recessions between 2000 and 2012

Future of the Loanable Funds Market in the United States • Fall in the savings rate over past 30 years • Increase in time preferences • Leftward supply shift in loanable funds market • Foreign savings in United States could shift supply back to the right • Retirement of baby boomers • Another reason to believe there will be a leftward shift in the supply of funds • Result could be less investment and reduced GDP growth

Conclusion—1 • Loanable funds markets channel funds from savers to borrowers • Supply of loanable funds: household savings • Suppliers provide funds for firms to expand through investment, which is crucial for economic growth • The quantity of loanable funds supplied is positively related to the interest rate. • Supply increases with income and wealth but is also impacted by consumption smoothing and time preferences.

Conclusion—2 • Demand for loanable funds: loans to firms • Firms borrow to invest in capital that aids in production of future GDP • The quantity of loanable funds demanded is negatively related to the interest rate. • Demand increases with capital productivity and investor confidence. • Equilibrium in this market determines the level of savings, investment, and interest rates.