Uploaded by

sabine

4 SLIDES

277 VUES

60LIKES

Optimizing Portfolio Variance with Constraints Using Lagrangian Method

DESCRIPTION

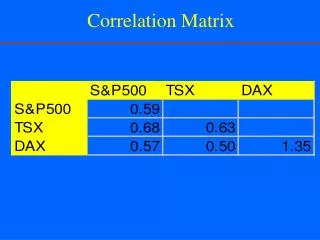

This document presents a solution to portfolio optimization problems by analyzing the correlation matrix. We derive the portfolio variance and explore the first-order conditions (FOC) necessary for achieving optimality under certain constraints, such as foreign content restrictions (X + Y < 30%). The Lagrangian approach is utilized to formulate the problem and derive conditions for the solution. This analysis is crucial for practitioners looking to enhance their portfolio management strategies while adhering to regulatory frameworks.

Download

1 / 4

Download Presentation

Télécharger la présentation

Optimizing Portfolio Variance with Constraints Using Lagrangian Method

An Image/Link below is provided (as is) to download presentation

Download Policy: Content on the Website is provided to you AS IS for your information and personal use and may not be sold / licensed / shared on other websites without getting consent from its author.

Content is provided to you AS IS for your information and personal use only.

Download presentation by click this link.

While downloading, if for some reason you are not able to download a presentation, the publisher may have deleted the file from their server.

During download, if you can't get a presentation, the file might be deleted by the publisher.

E N D

Presentation Transcript

Solution • The portfolio variance is: • The first order conditions are:

Constrained Optimization • Foreign content restriction: X+Y<30% • The Lagrangian: • FOC:

Solution • FOC:

More Related

Audio

Live Player