Download

1 / 12

120 likes | 331 Vues

Learn about stock and bond valuation methods, including CAPM and risk premium approach, with examples and calculations. Understand the concepts of bond valuation, yield to maturity, and realized yield in financial investments.

E N D

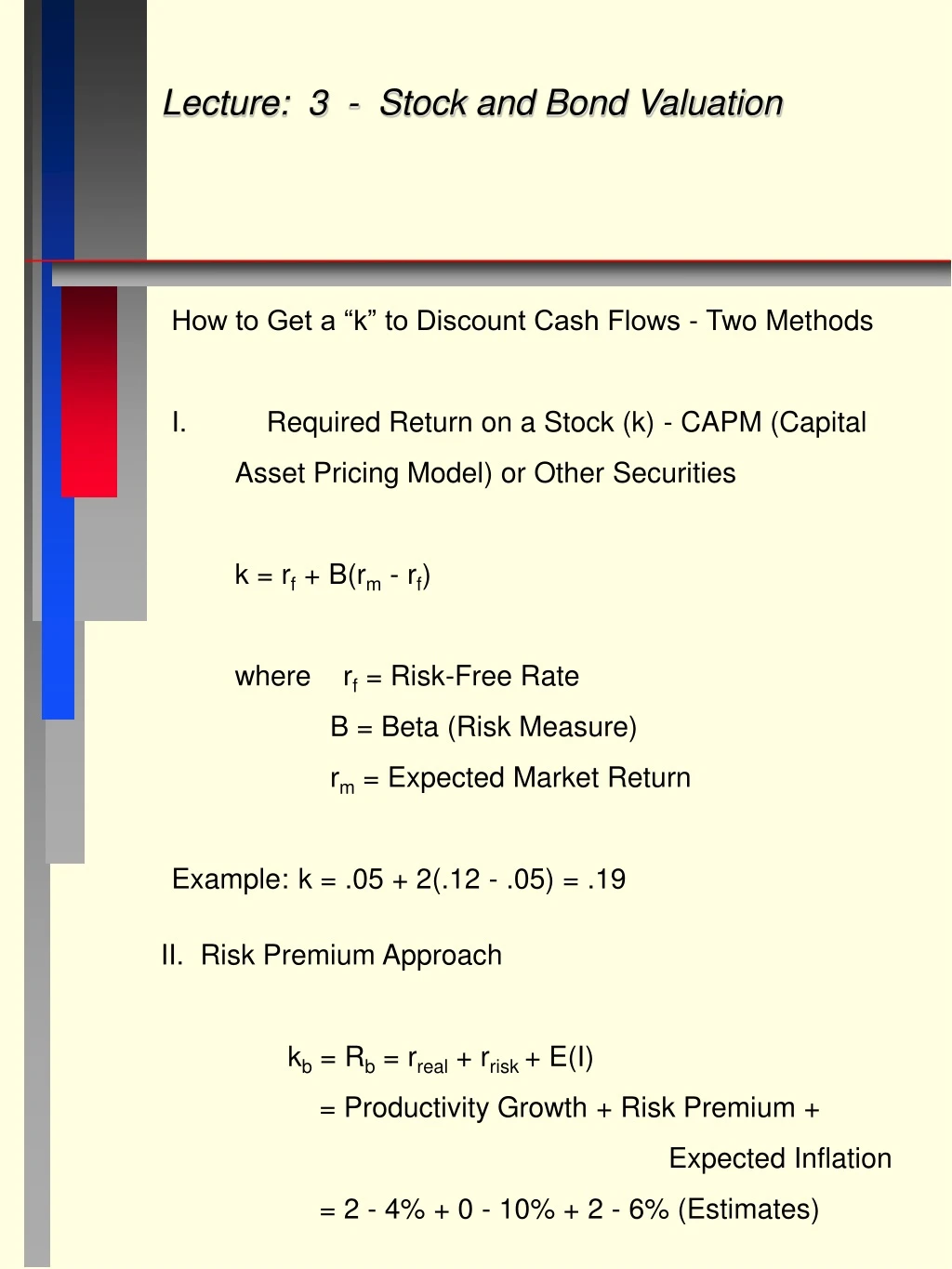

Lecture: 3 - Stock and Bond Valuation How to Get a “k” to Discount Cash Flows - Two Methods I. Required Return on a Stock (k) - CAPM (Capital Asset Pricing Model) or Other Securities k = rf + B(rm - rf) where rf = Risk-Free Rate B = Beta (Risk Measure) rm = Expected Market Return Example: k = .05 + 2(.12 - .05) = .19 II. Risk Premium Approach kb = Rb = rreal + rrisk + E(I) = Productivity Growth + Risk Premium + Expected Inflation = 2 - 4% + 0 - 10% + 2 - 6% (Estimates)

Lecture: 3 - Stock and Bond Valuation III. Bond Valuation Bond = Annuity Plus Single Par Payment (often Semi-Annual Payments) a. Par Value -face value, maturity value - usually $1000 b. Coupon Interest Rate - stated as a % of Par - 10% coupon on $1000 par => coupon = $100. c. Maturity - length of time until Par value is paid off

Bond Valuation “A Bond is an Annuity Plus a Single Face Value Payment” Annual Coupon Lecture 3 - Stock and Bond Valuation I. Bond Valuation General Formula B0 = I[PVAk,n] + M[PVk,n] B0= Bond Price I = Interest (coupon) Payment M = Par Value II. Example: Suppose a bond offers a 10% coupon, on $1000 par, for 3 years, and the expected inflation rate is 2%, the real rate is 3% and the bond’s risk is 1%. What is its price? B0 = $100[PVA.06,3] + $1000[PV.06,3] = $100(2.673) + $1000(.84) = $1107

QUESTION: If the company only agrees to pay $1000 at maturity, won’t those who buy this bond lose $107 at maturity? QUESTION: Would you buy this bond? Why? - greater coupon than par bonds. A par bond would cost $1000 but only pays a $60 coupon. The present value of the difference in coupons (100 - 60)(2.673) = 107 which is the difference in price between this bond and a par bond. Alternatively, a bond that offered a 2% coupon when rates are 6% will have a price of B0 = 20[PVA.06, 3] + 1000[PV.06, 3] = 893 or $107 less than the par bond.

Bond Valuation “A Bond is an Annuity Plus a Single Face Value Payment” Semi-Annual Coupon Lecture 3 - Stock and Bond Valuation I. Adjustments For Semi-Annual Coupon Bonds a. n = the number of semi-annual payments (maturity x 2) b. k = one-half the bond’s annual yield c. I = one-half the bond’s annual coupon II. Example: Suppose a bond pays 10% coupon, semi-annually, has 10 years until maturity and has a required return (or Yield to Maturity) of 8%. What is its price? B0 = $50[PVA.04,20] + $1000[PV.04,20] = $50(13.59) + $1000(.456) = $1135.5 QUESTION: Consider two identical bonds except that one pays an annual coupon and the other a semi-annual coupon. Which should have the higher price? ANSWER: The semi-annual bond.

Yield to Maturity and Realized Yield Lecture 3 - Stock and Bond Valuation YIELD TO MATURITY - The return one can expect on an investment in a bond if the bond pays all its coupons and par and yields do not change after you purchase the bond. PROBLEM: Suppose you observe a bond in the market with a price of $803 that pays a coupon of 10% till maturity in 5 years. What is its implied yield to maturity? Try 16% 803 = 100(PVA?,5) + 1000(PV?,5) = 100(3.274) + 1000(.476) = 803 REALIZED YIELD - The actual return one receives on the initial investment in a bond. QUESTION: If you buy a 20% coupon, par bond, with 3 years maturity and you hold it for three years are you sure to earn 20%? ANSWER: No because the calculation of YTM assumes that the coupons are reinvested at 20%, if rates change your realized yield will change because you'll earn more or less than 20% on their reinvested coupons.

Example: When you bought the bond, YTM was 20%. But suppose rates fell to 5% the day after you bought and stay there for three years. Your realized yield will be: use PV = FV[PVk,n] 1000 = (200(1+.05)2 + 200(1+.05) + 1200)[PVk,3] = 1630.5[PVk,3] => 1000/1630.5 = [PVk,3] = .6133 => k = 17% realized yield falls when reinvestment rate falls QUESTION: Then how can you truly lock-in a rate? ANSWER: Buy a bond with no coupons - called zero coupon bonds. QUESTION: How would you price a zero coupon bond? ANSWER: Use the second term in the bond pricing formula. QUESTION: Some find this attractive but is there a problem with being locked-in? ANSWER: Yes. How about if rates rise. You lose out on earning extra interest on reinvested coupons.

Stock Valuation “Valuation is Based Upon Expected Dividend Flow and the Future Expected Market Value of the Stock” Lecture 3 - Stock and Bond Valuation I. Common Stock Valuation General Formula P0 = E(D1)/(1+ke) + E(D2)/(1+ke)2 + ... + E(Dn)/(1+ke)n + E(Pn)/(1+ke)n where E means expectation,Dtmeans dividend at time t, P means stock price, and ke is the cost of equity. II. Example: Suppose a firm pays $4 in Dividends, which will increase by $1 in each of the next 3 years and we expect the price to be $30 at the end of the 3rd year. Assume stock beta = 1, the risk free rate is 10%, and the expected market return is 15%. What is the stock price? Ke = .10 + 1(.15 - .10) P0 = $4/(1.15) + $5/(1.15)2 + $6/(1.15)3 +$30/(1.15)3 = $4(.87) + $5(.756) + $6(.658) + $30(.658) = $30.94

Stock Valuation - Constant Growth “Valuation is Based Upon Expected Dividends That Grow at a Constant Rate For Ever” Lecture 3 - Stock and Bond Valuation Constant Growth Discounted Cash Flow Model, or DCF. P0 = = where D0 = present dividend paid at time 0 D1 = dividend expected at time 1 g = constant future growth in dividends k = required return (discount rate) Note: Works only for k>g and dividend paying firm PROBLEM: Suppose a company will pay a dividend of $5 in one year, has a required return of 10% and dividends grow 5% per year. What is the stock price? P = Mixture of Dividends PROBLEM: Suppose a firm will pay a dividend of $5 per year for 5 years and then increases the dividend by 10% per year thereafter. The firm has a required return of 15%. What is its price now? P = 5(PVA.15, 5) + [PV.15, 5] = 5(3.352) + 110(.497) = 71.43

Stock Valuation - Implied Required Returns and Growth Rates “Just Manipulate the Constant Growth Formula” Lecture 3 - Stock and Bond Valuation PROBLEM: Suppose we know the price of the stock in the market is $80, and it pays a dividend of $3 that will grow by 10% per year. What is the return the market requires on the stock? k = = = .14 PROBLEM: If the market price of a stock is $50, its required return is 15 percent and next year’s dividend is expected to be $5, by what percent must the market expect the company’s dividends to grow. g = k - so g = .15 - = .05

PRICE-EARNINGS RATIOS “PE’s Are Commonly Used to Compare Stocks” Lecture 3 - Stock and Bond Valuation PE Ratio - This is the number of dollars investors are willing to pay for each dollar of a company’s earnings. You can use the growth model to see why stocks have different price-earnings ratios P = = => = where E = earnings per share d = dividend payout ratio = Clearly, a larger growth rate and payout ratio and a smaller discount rate (k) makes for a larger price earnings ratio.