Download

1 / 20

200 likes | 546 Vues

CMBS Market Overview. FNCE 332 Fall 2002. CMBS Market Overview. The rise of the conduit loan market How conduit CMBS are structured Rating conduit CMBS: turning a sow’s ear into silk How CMBS trade in the market. The Rise of the Conduit Loan Market. Pre 1990

E N D

CMBS Market Overview FNCE 332 Fall 2002

CMBS Market Overview • The rise of the conduit loan market • How conduit CMBS are structured • Rating conduit CMBS: turning a sow’s ear into silk • How CMBS trade in the market

The Rise of the Conduit Loan Market • Pre 1990 • 1991 - 1994 - RTC turns to the capital market • 1995 - Conduits take over • Have conduits and the capital markets tamed the real estate boom bust cycle?

Reason for growth of CMBS • Sheer size of many of the larger assets are too big for the original lenders (insurance companies, Banks etc) • Capital markets are a more efficient method of securing financing • Capital markets are an efficient way to share/distribute the default risk

Creation of a CMBS Bond • A loan is given to a borrower of a commercial property • Originator collects a series of mortgages to create a pool • During the warehousing, Originator hedges • Hedge using Derivatives such as Swaps, Futures

Rating Conduit CMBS • Expected Losses - Default Probability x Loss Rate • 18% default rate X 60% loss rate = 10.8% expected loss • Underwriting - LTV, DSCR, Cap rate • Diversity - Geographic and property type • Administration • Servicer / Trustee review • Legal infrastructure • Ongoing review • Triple AAAs can withstand upwards of 35% default rate @70% loss rate

Marketing Stage • Marketing material is provided to investing public(Pre-Sales Reports, Prospectus) • Rating Agencies issue their final opinions • Sell Side firms “Launch” the deal(indicate indicated yields for each tranche • As much of the deal is sold as possible • Once completed it trades in the secondary like any other bond

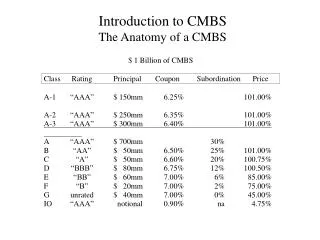

Typical CMBS Bond Structure Bond Rating % of DealSpreadYield AAA 75% S+50bps 5.45% AA 8% +80 5.65% A 8% +110 5.95% BBB 6% +135 6.20% BBB- 3% +175 6.60% IO T+400 8.25% * assumes 10YS of 4.85%, 10YT of 4.25%

How CMBS Trade in the Market 10 Year Maturity

CMBS Vs. MBS • Both are real estate but MBS are residential properties, CMBS Commercial properties(Office, Apts, Malls, Industrial etc) • CMBS are much less subject to prepayment risk, due to lockout, penalties & defeasance • However, CMBA sre more at risk from defaults • non recourse loans, no GSE guarantee

SIZE OF 3 TYPES OF CMBS In $Billions

Examples of CMBS Large Loan/Single Asset • Rockefeller Center $1.2 B (Single) • Mall of America $300 M (Single) • 4 Times Square $430 M (Single) • Citigroup Center $342 M (Large) • Buckland Mall $ 96 M (Large) • Chrysler Building $180 M (Portion)

Who Buys CMBS • Money Managers (Fidelity, PIMCO etc) • Insurance CO's (AIG, Traveler’s, etc) • Bank’s • Hedge Funds • CBO Issuers (Resecuritize) • Sell side firms (Goldman, Merrill) make a mkt.