Download

1 / 27

320 likes | 663 Vues

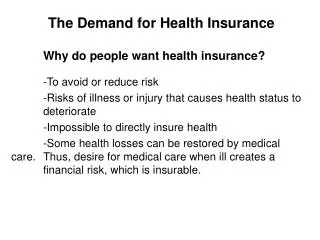

The Demand for Health Insurance. Why do people want health insurance? -To avoid or reduce risk -Risks of illness or injury that causes health status to deteriorate -Impossible to directly insure health

E N D

The Demand for Health Insurance Why do people want health insurance? -To avoid or reduce risk -Risks of illness or injury that causes health status to deteriorate -Impossible to directly insure health -Some health losses can be restored by medical care. Thus, desire for medical care when ill creates a financial risk, which is insurable.

Access motive (Nyman, JHE, 1999) Health insurance is not desired solely to protect against financial risk Desire to transfer purchasing power to “states of the world” where expensive but effective care results in high marginal utility of income

Example: Liver transplant $300,000 procedure, which would be unaffordable to someone with $50,000 net worth Utilization 1.33/100,000 Gain about 7 life years Assume value of a life year = $100,000 AFP for coverage = $4 Expected value of coverage = $9 Thus, it makes economic sense to insure this otherwise unaffordable procedure

Review of expected value and expected utility A risk averse person is willing to pay > AFP Expected value is the average value associated with the outcome of a risky situation: EV = iI Oi Where: i = the sum over all possible outcomes, i i = the probability of outcome i Oi = the value of outcome i

Expected Value example If you roll a die and I pay you $1 for a 1, $2 for a 2, and so on, the expected value of this game is: (1/6)*$1 + (1/6)*$2 + (1/6)*$3 + (1/6)*$4 + (1/6)*$5 + (1/6)*$6 = $3.50 A gamble is said to be “fair” if the expected value equals the cost

Risk aversion arises from a simple assumption about the shape of the U function: If utility generated by additional income declines with income (diminishing MUI), a plot of my utility against my income will be increasing, but concave FIGURE 1

Why does a concave U(I) imply risk aversion? -Suppose income is $30,000, generating U=40 -50% chance of incurring a $20,000 loss -Expected loss is $10,000; thus, expected income is $20,000 (note that when taking the gamble, the consumer will never actually have $20,000) -Utility falls to 20 if the loss occurs; expected utility is .5*40 + .5*20 = 30 -EU(gamble) < U(expected income): getting the average outcome for sure yields more utility than taking the gamble, implying that this consumer is risk averse

Graphically, EU can be determined using 3 steps: • Find the 2 outcomes (with and w/o loss) on the U(I) curve (A and B). Connect them with a straight line. • Calculate expected income with the gamble ($20,000) and find the point on the line associated with this income (C) • Find the point on the vertical axis associated with C. This is the EU of the gamble.

What certain income that would leave this person indifferent to taking the gamble? • Move horizontally from C (EU of taking the gamble) until you get to the utility of income curve (Fig. 3, point D) • Drop down from D to the income axis. This is the certain level of income that leaves this consumer just as happy as facing the gamble ($15,000). • This is $5000 less than expected income when taking the gamble. This consumer will pay up to $5000 to avoid the gamble (the risk premium). • Consumer prefers insurance with premium < $15,000 ($10,000 to cover the expected loss plus $5000 risk premium) to the gamble. Welfare gain from insurance = maximum WTP ($15,000) minus the actual premium.

What certain income that would leave this person indifferent to taking the gamble? (cont.)

Choosing an insurance policy Simple insurance policy: -Coinsurance rate of C -Policy pays (1-C)pmm if the consumer buys m units of medical care at price of pm -Consumer’s problem is to choose a policy (that is, a coinsurance rate) that maximizes EU

Choice of C is complicated because C influences the amount of care • Insurer will anticipate this behavioral response (known as moral hazard) and build its expected costs into the premium • Thus, policies offering lower C have higher premiums for two reasons: 1) they pay a higher fraction of the medical costs, and 2) enrollees respond to generous coverage by consuming more services This is the source of the fundamental trade-off in the choice of insurance: spreading financial risk vs. incentives to inefficiently increase care levels.

Risk-spreading vs. incentives • Risk averse consumer prefers high level of coverage • High coverage reduces OOP price, causing consumers to buy some units of care that they value less than its full cost. • For mild illness, demand = D1 and consumer chooses m1 without insurance or m2 with coinsurance = C • For severe illness, demand = D2 and consumer chooses m3 without insurance or m4 with coinsurance = C • Extra consumption induced by insurance creates welfare loss of A (mild illness) and B (severe). If coinsurance fell to 0, welfare losses would increase.

More elastic demand implies larger welfare loss - In the mild illness case, quantity of care is more responsive to price than in the severe illness case - Premium must cover expected costs of this extra care that the consumer doesn’t value very much (but will consume if the OOP price is low enough) • Insuring care for mild illness is less desirable than insuring the less price elastic services consumed for severe illness FIGURE 5

Price of insurance Premium consists of 2 components: • Expected costs of the benefits paid [(1-C)pmm] • Loading factor (L; the ratio by which premium exceeds expected benefit payout) Premium (R) is: R = (1+L)(1-C)pmm -If L=0, insurance is “free”; premium reflects only expected payout -With higher L, less insurance will be demanded -Could the welfare loss from moral hazard be thought of as part of the load?

Loading factors vary inversely with group size Typical Loading Fees By Group Size Table 1 • Fixed costs of writing and marketing policies can be spread over more people in larger groups • Large groups formed for reasons other than the purchase of health insurance (e.g., employee groups) are likely to contain good and bad risks; insurers don’t need to worry as much about risk selection and can limit underwriting

Summary of factors that influence D for insurance: • The more risk averse a consumer is, the greater the risk premium and willingness to pay for insurance • The greater the financial risk faced by the consumer, the more insurance they will desire • The more elastic the demand for services, the less insurance will be demanded • The higher the price of insurance (loading factor), the less insurance will be demanded

Are these predictions supported empirically? • Prevalence of insurance related to: -Elasticity of demand (e.g., mental health services covered less often and less generously) -Magnitude of risk (e.g., hospital vs. dental visits) -Size of employer Table 2 Table 3

The employer role and tax treatment of health insurance If the employer pays the premium, why wouldn’t everyone want generous coverage? Economists believe it doesn’t matter who writes the check; it’s the workers who “pay” Employers have an incentive to provide the least costly mix of wages and benefits that attracts the desired quantity and quality of labor. If an employer offers skimpy benefits, it will have to offer higher wages to attract the same work force.

Evidence on wage/benefit tradeoffs - Many studies show positive correlation between wages and benefits - Gruber (AER, 1994); costs of mandated maternity benefits were passed on, via lower wages, to female and married male workers of child-bearing age - Aggregate data: wages and salaries as a % of corporate revenues have declined since 1950, but total labor compensation (cash plus benefits) has remained constant at 65% of corporate revenues - Age/earnings profile flatter than age/total compensation profile Q1: What about near minimum wage workers? Q2: If workers really “pay” for their own insurance, are employers being irrational when they complain about high health costs?

So if the worker really pays for health insurance, why is the employer involved? -Economies of group purchasing -Employer-paid premiums escape taxation (deductible to the firm and pre-tax to the employee) -Worker with marginal tax rate t faces an effective premium of: (1-t)R = (1-t)(1+L)(1-C)pmm -Assuming L=10% for a large firm, a worker in the 28% tax bracket pays an effective premium < AFP

Policy objective of excluding premiums from taxable income is to encourage the purchase of insurance Is this an efficient way to accomplish this goal? -Insurance purchase is responsive to P (elast. –0.3 to –0.4) -Pre-tax treatment of benefits is worth the most to workers in the highest tax brackets -Income elasticity of the D for HI is around 1, so those getting the largest subsidy would be the most likely buy even without a subsidy -Since subsidy rises with the cost of the insurance plan, the quantity and type of coverage are distorted: -Complete coverage (e.g., low deductibles) -Coverage for low expense, low variation services such as routine dental and vision Conclusion: Flat tax credit would be more efficient and equitable

Employer role in plan choice As health plans have become more diverse (FFS, HMO, PPO, POS, etc.), employer plan choices increasingly restrict employees’ ability to choose style or site of care Moran, Chernew, and Hirth (HSR, 2001) found: -Employers with more diverse workforces accommodate preference heterogeneity by offering a broader set of plans -Fixed costs of offering additional plans preclude workers in smaller firms from receiving a broad set of plan choices -Firms in areas with fewer plan options available offer less choice to their employees

Why “co-premiums”? -Defined contributions to encourage choice of lower cost plans. Worker directly pays marginal cost. -Encourage use of alternative sources of insurance (spousal coverage, public programs) -Dranove et al. (JHE, 2000) found higher employee co-premiums were charged by employers facing higher costs of coverage and with workers more likely to have spouses eligible for their own coverage

“Crowd Out” of private coverage -Availability of public coverage makes private coverage less attractive -Cutler and Gruber (QJE, 1996) found that about half of the expansions of Medicaid to pregnant women and children over the 1987-1992 period were offset by reductions in private coverage. - LoSasso and Buchmueller (JHE, 2004) found similar levels of crowd out following SCHIP expansions