Download

1 / 33

330 likes | 473 Vues

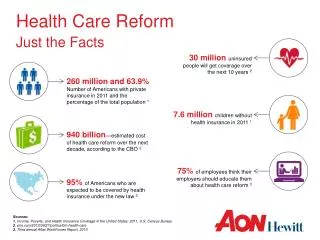

Health Care Reform Just the Facts. 30 million u ninsured people will get coverage over the next 10 years 2. 260 million and 63.9% Number of Americans with private insurance in 2011 and the percentage of the total population 1. 7.6 million children without health insurance in 2011 1.

E N D

Health Care ReformJust the Facts 30 million uninsured people will get coverage over the next 10 years 2 260 million and 63.9% Number of Americans with private insurance in 2011 and the percentage of the total population 1 7.6 million children without health insurance in 2011 1 940 billion—estimated cost of health care reform over the next decade, according to the CBO 2 95% of Americans who are expected to be covered by health insurance under the new law 2 75% of employees think their employers should educate them about health care reform 3 Sources: 1. Income, Poverty, and Health Insurance Coverage in the United States: 2011, U.S. Census Bureau 2. cnn.com/2012/06/27/politics/btn-health-care 3. Third annual Aflac WorkForces Report, 2013

Agenda • Review the New US Health Care System • Expanded Coverage • Individual Mandate • State-based Exchange (“Marketplace”) • Medicaid • Medicare • Affordable Care Act (ACA) Effect on: • Employers less than 50 employees • Employers greater than 50 employees • Questions

The New US Health Care System Expanding/Improving Coverage Paying for Expanded Coverage Health InsuranceExchanges with Reformed Rules Federal Subsidies to Buy Health Insurance in Exchanges Medicare/MedicaidPayment Changes ACA Penalties on Employer OptionalState Expansion of Medicaid “IndividualMandate”—now a “Shared Responsibility Payment” Increased Medicare Taxes on High-Income Individuals Increase inOther Taxes EmployerMandate – DELAYED UNTIL 2015 Taxation of High-Cost Employer Health Care Coverage = Direct impact to employers = Indirect impact to employers = Direct and indirect impact to employers 1 Supreme Court ruled states could decline to expand Medicaid eligibility without losing existing Medicaid funding 2 Supreme Court ruled “mandate” is a tax on not having health insurance

Coverage Options Today’s Options Effective January 1, 2014 Medicare Medicaid Marketplace Determines eligibility for Medicaid, and for premium assistance or lower out of pocket costs on health plans Employer-based Coverage (Active, Retiree or COBRA) TRICARE/ VA Health Coverage Individual Plans Expanded Coverage No pre-existing condition limitations Essential Health Benefits Preventive Care Cost sharing limits

Essential Health Benefits (EHB) and Removal of Pre-Existing Condition Limitations • Health Plans will offer the same set of essential health benefits with no annual or lifetime dollar limit. These essential health benefits include at least the following items and services: • Ambulatory patient services (outpatient care you get without being admitted to a hospital) • Emergency services • Hospitalization • Maternity and newborn care (care before and after your baby is born) • Mental health and substance use disorder services, including behavioral health treatment (this includes counseling and psychotherapy) • Prescription drugs • Rehabilitative and habilitative services and devices (services and devices to help people with injuries, disabilities, or chronic conditions gain or recover mental and physical skills) • Laboratory services • Preventive and wellness services and chronic disease management • Pediatric services • Essential health benefits are minimum requirements for all plans in the Marketplace. Plans may offer additional coverage. • Effective January 1, 2014, pre-existing condition limitations are prohibited (regardless of age).

Free Preventive Care • All Marketplace plans and non-grandfathered plans must cover the following list of preventive services without any cost to you! This applies only when these services are delivered by a network provider. • Abdominal Aortic Aneurysm one-time screening for men of specified ages who have ever smoked • Alcohol Misuse screening and counseling • Aspirin use to prevent cardiovascular disease for men and women of certain ages • Blood Pressure screening for all adults • Cholesterol screening for adults of certain ages or at higher risk • Colorectal Cancer screening for adults over 50 • Depression screening for adults • Diabetes (Type 2) screening for adults with high blood pressure • Diet counseling for adults at higher risk for chronic disease • HIV screening for everyone ages 15 to 65, and other ages at increased risk • Immunization vaccines for adults--doses, recommended ages, and recommended populations vary: • Obesity screening and counseling for all adults • Sexually Transmitted Infection (STI) prevention counseling for adults at higher risk • Syphilis screening for all adults at higher risk • Tobacco Use screening for all adults and cessation interventions for tobacco users

Cost Sharing Limits • Effective for plan years beginning on or after January 1, 2014, ACA places annual limits on total individual cost-sharing for essential health benefits. Once the limitation on cost-sharing is reached for the year, the enrollee is not responsible for additional cost-sharing for essential health benefits for the remainder of the year. • ACA’s cost-sharing limit is tied to the enrollee out-of-pocket maximum for HSA-compatible high deductible health plans (HDHPs). • For 2014, the out-of-pocket maximum cannot exceed $6,350 for self-only coverage and $12,700 for family coverage. • For plan years beginning after 2014, HHS will increase the cost-sharing limits by the premium adjustment percentage, similar to increases in the annual deductible limit.

Individual Mandate • The individual mandate is the requirement that most Americans obtain health insurance by January 1, 2014. If you don’t have health insurance in 2014, you’ll pay a penalty equal to the greater of $95 per adult and $47.50 per child (up to $285 per family), or 1% of your family income when you file your taxes. The penalty will increase significantly in 2015 and 2016: • For 2015: The greater of $325 per adult and $162.50 per child (up to $975 per family), or 2% of your income. • For 2016 and later: The greater of $695 per adult and $347.50 per child (up to $2,085 per family), or 2.5% of your income. • Transition relief has been provided to employees who are eligible for an employer sponsored group health plan that operates on a non-calendar year. • How will I prove I have health insurance? • You’ll get a certificate from your insurance company that says you have the minimum coverage. In 2014, you’ll have to submit a form with your federal tax return proving you have insurance.

Individual Mandate • Do any of the following apply? • You are part of a religion opposed to acceptance of benefits from a health insurance policy • You are an undocumented immigrant • You are incarcerated • You are a member of an Indian tribe • Your family income is below the threshold requiring you to file a tax return ($9,350 for an individual, $18,700 for a family in 2010) • You have to pay more than 8% of your income for health insurance, after taking into account any employer contributions or tax credits Start Here There is no penalty for being without health insurance Yes No • Were you insured for the whole year through a combination of any of the following sources? • Medicare • Medicaid or the Children’s Health Insurance Program (CHIP) • TRICARE (for service members, retirees, and their families) • The veteran’s health program • A plan offered by an employer • Insurance bought on your own that is at least at the Bronze level The requirementto have health insurance is satisfied and no penalty is assessed Yes No Source: Kaiser Family Foundation There is a penalty for being without health insurance 2014 2015 2016 and Beyond Penalty is $95/adult and $47.50/child (up to $285 for a family) or 1.0% of family income, whichever is greater. Penalty is $325/adult and $162.50/child (up to $975 for a family) or 2.0% of family income, whichever is greater. Penalty is $695/adult and $347.50/child (up to $2,085 for a family) or 2.5% of family income, whichever is greater.

Individual Plan Options • If your currently covered by an individual health plan, it must offer new benefits and protection levels at time of renewal on or after 1/1/2014 • Your health plan may change to cover these protections, or it may be eliminated and you’ll need to make a new election • Insurance companies will provide you 90-day notice if plan is being eliminated • Your choice of plans include: • Evaluate the private insurance market directly • Evaluate the Marketplace where you may qualify for premium subsidies or lower out of pocket costs based on your income/household size. • Open enrollment: October 1 – March 31 • If your individual health plan ends outside of this open enrollment, you will have a special enrollment period of 60 days prior to the end of the coverage, or after lose of coverage to enroll into the marketplace.

State Exchange Option • What is a health insurance marketplace or exchange? • A marketplace, or exchange, is a website where you can shop for health insurance. You can compare all of your options and costs side by side and see if you qualify for financial help. All the plans offered in a marketplace, or exchange, must meet certain rules relating to affordability, required benefits, and market standards. • What can I do through a health insurance exchange? • You’ll be able to: • Shop for health insurance offered by well‐known insurance companies. • Choose from health plans grouped by metallic levels: Bronze, Silver, Gold, and Platinum. The different plans will offer you choices in: • How much you’ll pay for coverage (premium amounts) • How much you’ll pay out of your own pocket for medical care and prescription drugs (deductibles, coinsurance, copays, and out‐of‐pocket maximums) • Networks of participating doctors, hospitals, labs, and other health care providers • Complete an application to find out if you qualify for financial help. • Enroll in health insurance that’s right for you or your family. The federal and state health insurance marketplaces will begin enrollment in October 2013 for coverage starting January 1, 2014.

Premium Assistance through Exchange • Who is Eligible? • Financial help comes in the form of a federal tax credit. You can use it immediately to lower what you pay for your health plan each month, or lower what you pay at tax time. Qualification depends on your household size and income. Plans and prices will be available for purchase on insurance marketplaces starting October 1, 2013. You will learn your exact costs and savings when you apply for coverage. • Generally you can qualify for financial help if: • Your employer does not offer a health plan; • You don’t receive Medicare; • Your family income is less than four times the federal poverty level. This chart gives you an idea of what that means.

Washington State Exchange: Open Enrollment • Washington healthplanfinder is Washington’s state-based exchange option. • Website: http://wahealthplanfinder.org/ • September 3, 2013 call center opens • Initial Enrollment Period for inside and outside of the exchange for Individual products will be October 1, 2013–March 31, 2014.

Medicaid Expansion in WashingtonApprox. 325,000 newly eligible • Eligibility will be based on applicants Modified Adjusted Gross Income (MAGI) from their most recent federal income tax filing, and how many people are in their household. • Washington’s Exchange, Healthplanfinder, will be used to process applications for Medicaid, Children’s Health Insurance Program (CHIP) or subsidized Exchange participants through the single portal • The portal opens October 1, to enroll Medicaid participants. Coverage will begin January 1, 2014. • The portal will verify data with IRS, SSA and Homeland Security reducing the eligibility verification down to a 45 minute process. • Applicants can also apply via mail, phone or in-person (available at EvergreenHealth and Community Health Access Department) • Medicaid coverage may start retroactively for up to 3 months prior to the month of application, if the individual would have been eligible during the retroactive period had he or she applied then. • Medicaid Eligible Income Levels (based on household size):

Medicare • Medicare is not part of the Marketplace, and you will still have the same benefits you have now whether its through Medicare or through a Medicare Advantage Plan • Medicare’s Open Enrollment Period (October 15-December 7) • For information on these programs, visit Medicare.gov. • Expanded Medicare benefits for preventive care, drug coverage • Medicare benefits have expanded under the health care law, including free preventive benefits, cancer screenings and an annual wellness visit. • You can also save money if you’re in the prescription drug “donut hole” with discounts on brand-name prescription drugs.

Young Adults/College Students Options • Enhanced Benefits provided under the ACA • Prohibits insurance companies from refusing coverage to or limiting the benefits because of a pre-existing medical condition • Requires insurance plans to cover preventive services with no copayment. • No annual/lifetime limits on essential health benefits • Parent’s Coverage: ACA ensures that children will be allowed to stay on their parents’ health insurance until age 26. • Individual Plans • Student Health plans sponsored by College/University • Marketplace: Subsidies may be provided based on income levels of household and availability of employer based coverage

Employer Based CoverageFewer than 50 employees • If Under 25 Employees, you may be eligible for Health Care Tax Credits. • Tax credits through the IRS are available for both for-profit and tax-exempt organizations to help cover the cost of coverage for employees. Starting in 2014, the credit will increase to cover 50 percent of premium costs. To qualify, small employers must: • Provide health insurance to employees and cover at least 50 percent of the cost of coverage. • Employ fewer than 25 full-time workers (employers with fewer than 50 part-time workers may be eligible). • Pay average annual wages below $50,000. • Starting in 2014, small employers with generally up to 50 employees will have access to the new health care insurance marketplaces through the Small Business Health Options Program (SHOP). • Washington healthplanfinder : To participate, businesses may have up to 50 employees, be based in or have an employee worksite in Washington State, and achieve minimum group participation rates. Participation rates include 100 percent for businesses with two to four employees and 75 percent for businesses with five to 50 employees. • Employers with more than 50 employees may be eligible to purchase coverage through Washington healthplanfinder in 2017. • Available only in select counties for January 1.

Employer Based CoverageFewer than 50 employees • If I offer a plan today, what can I expect? • Grandfathered Health Plans. You don’t have to do anything with the design of your health plan. You current plan will remain in place and continue to cover your employees as it does today. Your costs may increase due to new taxes/fees beginning 2014. • Non-Grandfathered Health Plans. Your plan may be discontinued for plan years beginning 1/1/2014. Some insurers, like Premera Blue Cross, will be transitioning your plan to a new, reform-mandated “metallic” plan. • What will these new plans look like? • Metallic levels. Federal healthcare reform categorizes plan levels into bronze, silver, gold and platinum. Platinum plans have the highest level of benefits and highest cost to you. • More benefits and cost. New plans will likely have more benefits than the current plan you offer employees. If this is the case, you may see an increase in cost. • [Optional for some Insurers] More wellness and discount opportunities. If your employees commit to certain activities related to wellness, an insurer may offer rate discounts.

Employer Based CoverageGreater than 50 employees • Employer Shared Responsibility Provision has been delayed until 2015. Employers with 50 or more full-time equivalent employees will face a penalty if they do not offer affordable minimum levels of healthcare coverage to their employees. • Health plan coverage for employees and their dependents (children under 26, but not spouses). • A plan that meets the Minimum Essential Coverage requirements. • A plan that meets the minimum actuarial value of 60 percent • A plan where the lowest cost option requires employees to contribute no more than 9.5 percent of their household income for self-only coverage • Coverage for at least 95 percent of your employees.

ACA Fees and Taxes • Transitional Reinsurance Fee • HHS issued proposed rule November 30, 2012 establishing reinsurance fee at $63.00 per capita for 2014 • Fee will be used to stabilize premiums in the individual market from 2014 to 2016 • But fee is assessed on both fully-insured and self-insured group health plans • Fees are based on the number of covered lives under a plan • Post-65 retirees who have primary Medicare coverage are not counted • PCORI Fee • PCORI fee is the fee imposed on health insurance issuers and plan sponsors of self-insured plans to fund the Patient-Centered Outcomes Research Institute (PCORI) Trust Fund that will research the comparative effectiveness of medical treatments • The fee is imposed based on the average number of lives for plans years ending after October 1, 2012 and before October 1, 2019 • The fee for plan years ending on or after October 1, 2012 and before October 1, 2013 is $1 X the average number of lives • The fee increases to $2 X the average of number of lives for plan years ending on or after October 1, 2013

ACA Fees and Taxes • Industry Fee Tax • As part of the Patient Protection and Affordable Care Act, the Industry Fee tax imposes annual fees on health insurers that start at $8 billion in 2014, increases to $14.3 billion in 2018, and will increase every year after that. The Joint Committee on Taxation estimates the tax will exceed $100 billion over the next ten years. • The fee will be divided among health insurance carriers based on each carrier’s share of the overall national premium base, and will only be assessed relative to insured health plans, including medical, dental and vision plans. The fee is not applicable to self-funded health plans or stop loss insurance policies. • The Industry Fee is not deductible for federal income tax purposes. This substantially increases the cost impact, which is expected to be in the range of 2.0 to 2.5% of premium in 2014, increasing to 3.0 to 4.0% of premium in later years. • Insurance companies will begin to reflect this additional cost in your 2014 premium rates.

Notice of Coverage Options Mandated for all Employers covered by the Fair Labor Standards Act • All Employers must provide employees with the Department of Labor (DOL) Notice of Coverage options covering: • Notification about the new Health Insurance Marketplace; • Inform employees that they may be eligible for a premium tax credit if they purchase coverage through the Marketplace; • Advise employees that if they employee purchase a plan through the Marketplace, they may lose the employer contribution (if any) to any health benefits plan offered by the employer. • Employers are required to provide this notice to all current employees by October 1, 2013, and to each new employee at the time of hire beginning October 1, 2013, regardless of plan enrollment status (if applicable) or of part-time or full-time status.

Summary of Benefits and Coverage (SBCs) Disclosure Rules • Employers are required to provide employees with a standard “Summary of Benefits and Coverage” form explaining what their plan covers and what it costs. • Employers need to distribute this to employees during annual enrollment and for new hires. • The purpose of the SBC form is to help employees better understand and evaluate their health insurance options. • Penalties may be imposed for non-compliance.

Sample of Employee Choice Options With Exchange Subsidy (Employer coverage fails affordability test) Without Exchange Subsidy (Employer coverage passes affordability test) Employee Data: Age 28 Salary: $20,000 Single Coverage Exchange $1,019 (employer penalty) Uninsured Penalty $200 Employer $1,950 Exchange $3,391 Uninsured Penalty $200 Employer $951 Exceeds 9.5% Affordability testing Within 9.5% Affordability testing Note: Exchange cost/subsidy estimates above are generic examples based on Silver Plan and provided by Kaiser Health Reform Subsidy Calculator

Employer Shared Responsibility Penalties—Delayed until 2015 (Also known as the ‘Pay or Play’ or ‘Free Rider Penalty’) The penalty is $2,000 annually times the number of full-time employees minus 30. The penalty is increased each year by the growth in insurance premiums. The employer must pay a penalty for not offering coverage. Does the employer offer coverage to its workers? Did at least one employee receive a premium tax credit or cost sharing subsidy in an Exchange? Start Here Yes No Does the insurance pay for at least 60% of covered health care expenses for a typical population? Employees can choose to buy coverage in an Exchange and receive a premium tax credit. The penalty is $3,000 annually for each full-time employee receiving a tax credit, up to a maximum of $2,000 times the number of full-time employees minus 30. The penalty is increased each year by the growth in insurance premiums. No The employer must pay a penalty for not offering affordable coverage. Yes Yes No Do any employees have to pay more than 9.5% of family income for the employer coverage (employee only)? Those employees can choose to buy coverage in an Exchange and receive a premium tax credit. Yes There is no penalty payment required of the employer since it offers affordable coverage. *Assumes employer has at least 50 full-time equivalent employees.

The ACA Penalties—Definitions • Who is an “applicable large employer”? • Employer that employed an average of at least 50 full-time employees on business days during the preceding calendar year • That includes “full-time equivalent employees” (FTEs), which are statutorily determined based on the hours of service of employees who are not full-time employees • Who is an employee? • Determination is based on IRS’s decades-old “common law” test • Employment relationship exists when the person for whom the services are performed has the right to control and direct the individual who performs the services, not only as to the result to be accomplished by the work but also as to the details and means by which that result is accomplished • Employment relationship exists if employee is subject to the will and control of the employer not only as to what shall be done but how it shall be done • Not necessary that employer actually direct or control the manner in which the services are performed; it is sufficient if the employer has the right to do so • Who is a “full-time employee”? • Employee works 30 hours or more per week, measured monthly • 130 hours of service in a calendar month is treated as monthly equivalent of 30 hours of service per week

The ACA Penalties—Definitions • What is “unaffordable coverage?” • Employer plan is unaffordable if the FTE’s required contribution exceeds 9.5% of taxpayer’s household income for the taxable year • Safe harbor methods for 9.5% calculation • W-2 wages • Rate of pay • Federal Poverty Level • Affordability is based on cost of self-only coverage, even if employee elects family coverage • What is “minimum actuarial value?” • Plan must pay at least 60% of covered expenses • Different methods to calculate MAV • Calculator approach • Design-based checklist • Actuarial certification

The ACA Penalties—Determining FTEs • Safe harbor methods available for transitional purposes for employers to determine FTE status of: • Ongoing employees • New employees • Ongoing employees • An employer will be permitted to use measurement and stability periods of up to 12 months to determine FTE status of ongoing employee • New employees • For new employee reasonably expected to work full-time, employer can exclude employee from health care coverage for first three months of employment without incurring penalty under the ACA • For new variable hour or seasonal employees, employers will use an initial measurement period/stability period to determine FTE status • All employees • Employer will not be subject to any ACA penalty if health care coverage offered to FTEs is: • Minimum value and • Affordable • Employer can use employee’s Form W-2 wages (Box 1) to determine affordability

The ACA Penalties—Determining FTEs Employers need to establish • Measurement period • Period of time over which employer tracks employee’s hours of service • Cannot be less than three months or more than twelve months in duration • Initial measurement period for new employees will be based on each employee’s start date • Standard measurement period for ongoing employees will be uniform period of time set by employer • Administrative period—optional (up to 90 days in duration) • Employer looks back at employee’s hours of service in measurement period • Did employee work an average of 30 hours per week during measurement period? • If yes, then employee is a FTE • If no, then employee is not a FTE and employer has to keep tracking hours of service in next measurement period • Stability period • Period of time employer must offer coverage to FTE to avoid ACA penalties • Stability period must at least equal measurement period, but not less than six months • If not an FTE in measurement period, stability period cannot exceed measurement period

The ACA Penalties—Determining FTEs • Employers may vary Measurement Periods and Stability Periods for following categories of employees • Union and Non-Union • Salaried and Non-Salaried • Employees of different entities • Employees located in different states • Employer is not required to offer coverage to any particular employee or class of employees, including part-time employees, but may be liable for penalty • However, an otherwise eligible employee (or dependent) cannot be required to wait more than 90 days before coverage becomes effective • No waiting period beyond 90 days • Eligibility conditions based solely on the lapse of time cannot be longer than 90 days • Employer cannot impose a waiting period that conditions enrollment on the first day of the month after completing 90 days • Employer may condition eligibility on an employee regularly working a specified number of hours per period (or working full time) • The employer may take a reasonable period of time to determine whether the employee meets the plan’s eligibility condition

2018 Excise Tax on High Cost Coverage (Also known as the “Cadillac Tax”) The excise tax was included in the Patient Protection and Affordable Care Act (PPACA) passed into law on March 23, 2010. The provision levies a 40% nondeductible tax on the annual value of health plan costs for employees that exceed $10,200 for single coverage or $27,500 for family coverage in 2018. The threshold increases annually at a rate of inflation (CPI) + 1% in 2018 and 2019, and CPI thereafter.