The Balanced Scorecard

The Balanced Scorecard. Presented To. Finance and Administrative Services Division. Presented By. John Sanders. The California State University Quality Improvement Programs. Seminar Outline. Introduction to the Balanced Scorecard What is it? Why do it?

The Balanced Scorecard

E N D

Presentation Transcript

The Balanced Scorecard Presented To Finance and Administrative Services Division Presented By John Sanders The California State University Quality Improvement Programs

SeminarOutline Introduction to the Balanced Scorecard What is it? Why do it? Balanced Scorecard Fundamentals The Four Perspectives Measures, Targets and Initiatives Roles and Responsibilities The CSUSM Finance & Administrative Services Strategy Map Using the BSC as a Management System

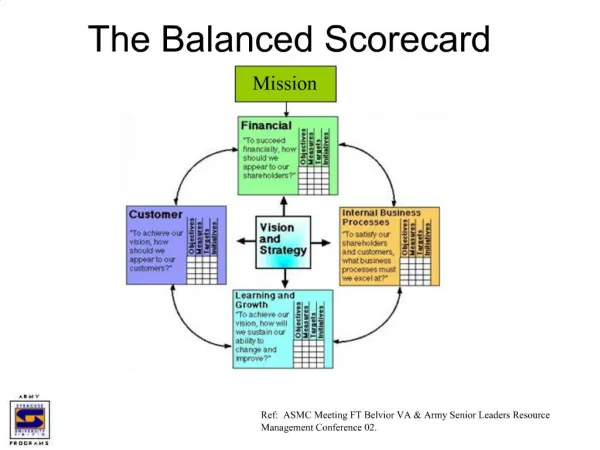

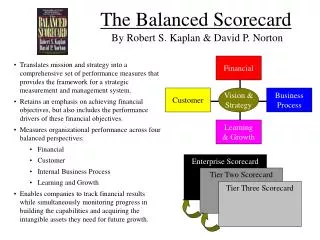

The Balanced Scorecard What is it? Definition: The Balanced Scorecard is a management tool that provides stakeholders with a comprehensive measure of how the organization is progressing towards the achievement of its strategic goals.

The Balanced Scorecard What is it? The Balanced Scorecard: • Balances financial and non-financial measures • Balances short and long-term measures • Balances performance drivers (leading indicators) with outcome measures (lagging indicators) • Should contain just enough data to give a complete picture of organizational performance… and no more! • Leads to strategic focus and organizational alignment.

The Balanced Scorecard Why do it? • To achieve strategic objectives. • To provide quality with fewer resources. • To eliminate non-value added efforts. • To align customer priorities and expectations with the customer. • To track progress. • To evaluate process changes. • To continually improve. • To increase accountability.

The Balanced Scorecard Why do it? It works! In just 90 days, Sandia Labs was able to redirect $190,000 in savings by dropping initiatives that didn’t fit their overall strategy. “The BSC has forced our management team to focus beyond financial measures… too often in the past we would get sucked into short-term thinking.” “The BSC dramatically improved our data analysis… we don’t overreact nearly as much as we used to.”

The Balanced Scorecard and The CSU Campuses currently working on the BSC • San Luis Obispo • Pomona • San Jose • San Marcos • Sonoma • Fullerton • Long Beach • Chico • Northridge • San Bernardino • Chancellor's Office

The Strategy Focused Organization Mission – What we do Vision – What we aspire to be Strategies – How we accomplish our goals Measures – Indicators of our progress

Environmental Scan Strengths Weaknesses Opportunities Threats A Model for Strategic Planning Values Mission & Vision Strategic Issues Strategic Priorities Objectives, Initiatives, and Evaluation

The Strategy Focused Organization • The Five Principles • Translate the strategy to operational terms. • Align the organization to the strategy. Source: The Strategy Focused Organization, Norton & Kaplan

The Strategy Focused Organization • The Five Principles (cont.) • Make strategy everyone’s job. • Make strategy a continual process. • Mobilize change through executive leadership Source: The Strategy Focused Organization, Norton & Kaplan

The Balanced Scorecard and The Big Picture • Activity Based Costing • Economic Value Added • Forecasting • Benchmarking • Market Research • Best Practices • Six Sigma • Statistical Process Control • Reengineering • ISO 9000 • Total Quality Management • Empowerment • Learning Organization • Self-Directed Work Teams • Change Management

Strategic Direction Create Environment For Change Strategic Performance Management System Communicate Strategies Define Objectives Implement BSC Balanced Scorecard Measure Performance Improve Processes Evaluate and Adjust Continuous Improvement Redefine Initiatives Linking it all together….

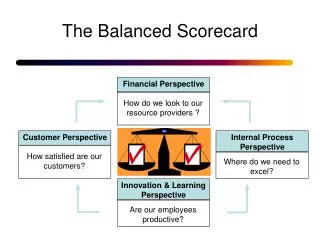

THE BALANCED SCORECARD FINANCIAL/REGULATORY To satisfy our constituents, what financial & regulatory objectives must we accomplish? CUSTOMER To achieve our vision, what customer needs must we serve? INTERNAL To satisfy our customers and stakeholders, in which business processes must we excel? LEARNING & GROWTH To achieve our goals, how must we learn, communicate and grow?

Customer Perspective To achieve our vision, what customer needs must we serve? Possible Performance Measures • Customer Satisfaction (Average) • Satisfaction Gap Analysis (Satisfaction vs. • Level of Importance) • Satisfaction Distribution (% of each area scored)

Financial / Regulatory Perspective To satisfy our constituents, what financial and regulatory objectives must we accomplish? Possible Performance Measures • Cost / Unit • Unfunded Requirements or Projects • Cost of Service • Budget Projections and Targets

Internal Perspective To satisfy our customers, in which business processes must we excel? Possible Performance Measures • Cycle Time • Completion Rate • Workload and Employee Utilization • Transactions per employee • Errors or Rework

Learning and Growth To achieve our goals and accomplish core activities, how must we learn, communicate and work together? Possible Performance Measures • Employee Satisfaction • Retention and Turnover • Training Hours and Resources • Technology Investment

Why Measure? • To determine how effectively and efficiently the process or service satisfies the customer. • To identify improvement opportunities. • To make decisions based on FACT and DATA

Measurements Should: • Translate customer expectations into goals. • Evaluate the quality of processes. • Track our improvement. • Focus our efforts on our customers. • Support our strategies.

Targets “If you don’t know where you’re going, you’re probably not gonna get there.” Forrest Gump

Targets • Targets need to be set for all measures • Should have a “solid basis” • Give personnel something for which to aim • If achieved will transform the organization • Careful not to develop measures/targets in a fragmented approach: i.e. Asking people to increase customer satisfaction has to be backed up with the knowledge, tools, and means to achieve that target.

Initiatives Once measures and targets are established, it is the responsibility of management to determine HOW the organization will achieve its goals. Measures are used to determine the effectiveness of strategic initiatives.

The Leadership Team • Develops the division’s vision, strategy and goals • Develops organizational objectives and targets • Provides leadership, endorsement and vision for the project • Clears barriers to scorecard progress

The Core Team • Drafts the strategy map and scorecard • Works with employees to develop measures supporting strategic objectives • Works with the Leadership Team to plan and implement the Balanced Scorecard in the FAS Division

Finance and Administrative Services Strategy Map

Link it together…. DIVISION CUSTOMER FINANCIAL INTERNAL PROCESS LEARNING & GROWTH Hum. Rscrs. Univ. Police Facilities DEPT. Police Parking FUNCTION Measure: Satisfaction Index Current: 3.0 Target: 4.0

The Balanced Scorecard as a Management System BSC reviewed regularly to enhance operational decision-making • Success of initiatives assessed based on DATA… not opinions • Leading indicators evaluated to confirm accuracy of assumptions

The Balanced Scorecard as a Management System The BSC is a “Living Document” that requires regular revision of objectives, measures and initiatives: • How are we doing? • Are we measuring the right things? • What initiatives do we need to get us where we want to go? • Have our organizational goals changed?

Advantages to this Approach • Simple to Use and Understand • Based on Vision and Strategy • Multidimensional • Quantitative and Qualitative Measures • Current and Future • Provides Measurement of and Method for Improving our Services • Ties QI initiatives together • Serves as a Communication Tool

Suggested Readings Kaplan, Robert and Norton, Edward. The Balanced Scorecard. Harvard Business Publishing, 1998 Kaplan, Robert and Norton, Edward. The Strategy-Focused Organization. Harvard Business Publishing, 2001 Buckingham, Marcus and Coffman, Curt. First, Break All the Rules The Gallup Organization, 1999 Brown, Mark. Keeping Score. Mark Graham Brown, 1996 http://www.afd.calpoly.edu/afd/Strategic_plan/ http://cqi.csusb.edu/

Thank You John Sanders The California State University (562) 951-4556 jsanders@calstate.edu www.calstate.edu/qi