Download

1 / 32

320 likes | 525 Vues

Common Stock And Dividends. Chapter 15 & 16. 04/20/2009. Learning Objectives. Characteristics of common stock. Advantages and disadvantages of equity financing. Process of issuing common stock. Stock Options Cash Dividends Stock dividends, stock splits Stock repurchases.

E N D

Common Stock And Dividends Chapter 15 & 16 04/20/2009

Learning Objectives • Characteristics of common stock. • Advantages and disadvantages of equity financing. • Process of issuing common stock. • Stock Options • Cash Dividends • Stock dividends, stock splits • Stock repurchases

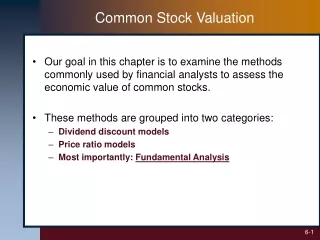

52 Weeks Yld Vol Net Hi Lo Stock Sym Div % PE 100s Hi Lo Close Chg s 42½ 29 QuakerOats OAT 1.14 3.3 24 5067 35 34¼ 34¼ -¾ s 36¼ 25 RJR Nabisco RN .08p ... 12 6263 29¾ 285/8 287/8 -¾ 237/8 20 RJR Nab pfB 2.31 9.7 ... 966 24 235/8 23¾ ... 7¼ 5½ RJR Nab pfC .60 9.4 ... 2248 6½ 6¼ 63/8 -1/8 Stock Quote – Wall Street Journal Company Issuing the Stock Link to NASDAQ

Characteristics of Common Stock • Ownership - shareholders • Dividends: • Vary over time • Not guaranteed • Unlimited growth • Residual Claim on income • Voting Rights • Sometimes Preemptive Right to buy New Stock • Lowest claim in case of liquidation

Management of Publicly Traded Corporations • Shareholders elect a group of individuals called the Board of Directors who oversee the management of the corporation. • The Board of Directors selects and oversees the managers who are responsible for day-to-day operations of the firm. • Directors have fiduciary responsibility to act in the best interests of those who elected them. (Fiduciary means legal duty to act in the best interests of those who entrusted you.)

Ownership of Common Stock • Mostly owned (70%) by institutional investors • Investors are taking a more active role, seats on board, etc • Institutional investors include: Pension plan funds (CALPERS) Insurance companies Mutual funds Hedge funds

Board of Directors Elections • Majority voting • For each seat open, one vote can be cast per share owned. Those who own the most shares get their candidates elected • Cumulative voting • Each shareholder gets one vote per share times the number of seats open. Candidates do not run for a specified seat. Votes may be spread out among candidates as desired, or all votes can be cast for one candidate.

Cumulative Voting Example • Suppose you own 100 shares • Suppose there are three open director slots • Then you would have 100 x 3 or three hundred votes to cast. • Under majority voting, you could only cast one hundred votes for each candidate • Under cumulative voting, you could cast all three hundred votes for one candidate or split them up any way you want. • Thus, minority shareholders, by cumulating their votes and casting them for one person could elect someone to the board.

Pros and Cons of Equity Financing Disadvantages of Equity Financing • Dilution of ownership and power due to more shares of stock outstanding. • Lower earnings per share/stock price • A lot more work than Debt offering • Flotation costs (expensive) • Fees paid to investment bankers, lawyers, accountants, printers, SEC • Usually much higher than for debt issues.

Pros and Cons of Equity Financing Advantages of Equity Financing • No interest or principle to pay (unlike debt) • No obligation to pay dividends. • Management doesn’t like debt (risk averse) • Reduces financial risk (total debt ratio) • This may be a more important advantage to firms that already are relatively risky due to the kind of business they do (e.g. high tech has high business risk)

Issuing Common Stock • Sell to existing shareholders or to new shareholders? How much $ do you need? • Initial Public Offering (IPO) (first time) • Role of Investment Bankers • Underwriting – syndicate guarantees the sale, sets the price, buys the stock and resells it to the general public (expensive) • Best efforts – sell what they can • Investment bankers include: Goldman Sachs, Morgan Stanley, Merrill Lynch, J.P. Morgan, Credit Suisse First Boston, & others

Pricing New Issues of Stock • If publicly traded, stock sells for existing market price • If IPO, a difficult task, much haggling with the investment banker, (and often wrong) • Google • Methods include present value of future cash flows, comparisons to similar types of companies, market value of angel and secondary private offerings, etc.

Rights and Warrants • Stock Rights • Preemptive rights give owners of stock the right to maintain their % ownership of the firm • If the firm issues new stock, owners have the “right” to purchase their proportionate share of the new stock issue • Because rights typically have a lower exercise price than the market price, the rights can be sold on the open market for the difference

Rights and Warrants • A warrant is a security giving the owner the option to buy shares of common stock at a certain exercise price for a set period of time. • Like rights except that they are sold to investors rather than given away. • Each warrant allows you to buy a particular number of shares of stock for a favorable exercise price. • Sometimes given to Bond and Preferred Stock investors as an incentive (see Indenture Agreement)

Stock Options • An option to buy shares of stock at a pre-determined price, usually set at the current market price of the stock or slightly below • Given to Directors, Officers and Employees as an incentive to stay with the company and make it grow • The recipient usually has a period of time, say ten years, in which to exercise the options before they expire • Options typically vest over time, meaning the recipient can’t exercise them until a certain amount of time has passed.

Stock Options (Cont’d) • Certain restrictions may apply as to when an option may be exercised • Shares used for stock options exercised usually come from Treasury stock • Employee writes a check to the company for the exercise price of the option • Income must be recognized by the employee at time of exercise – market price less exercise cost • Exercise and sell?

Stock Options – Expense? • Much controversy over whether stock options are compensation to the recipients and therefore should be recorded as an expense on the books of the company • FASB and legislators pushed for expensing. FAS 123® • Primarily High Tech firms have pushed to not record them as an expense. Why? (Dilutes earnings; less viable to firms)

Stock Option Backdating • Normally, stock option exercise price is set on the date the option is approved by the BOD, according to the bylaws of the Corporation • Some companies decided to date the options as of the date of the lowest recent price • This substantially increases the value of the option. • Done primarily for top management! • Another example of greed

Dividend Policy • A company that projects low growth, and has excess funds, may pay large dividends (PG & E) • Management expects high growth, high need for cash; may mean high retained earnings but low or no dividends (high tech firms)

Factors that affect dividend policy • Restrictions on dividend payments Bond indenture agreements Lack of retained earnings • Availability of cash • Stockholders’ preferences Capital gains vs ordinary income

On August 25, 2002 Southside Bankshares announced a quarterly dividend of $1 per share to be paid to shareholders of record September 9, 2002. Dividend will be paid on Sept. 15, 2002 Dividend Payment Procedures Each dividend must be declared (approved) by the Board of Directors. This is usually done at the quarterly Board meetings.

On August 25, 2002 Southside Bankshares announced a quarterly dividend of $1 per share for shareholders of record September 9, 2002, and to be paid on September 15, 2002 25 31 1 7 9 15 August September Ex-Dividend Date Declaration Date Date of Record Dividend Payment Procedures Payment Date Ex-dividend date is the date you must buy stock in order to be shareholder of record

Dividend determination methods • Dividend Rate. Most companies use a fixed dollar amount per share. This amount is determined by the Board of Directors • Dividends tend to stay the same or increase slightly each year; shows stability, positive future • Decreases in dividends can severely impact the stock price

e.g. if there is a 10% stock dividend, you would receive one additional share for every 10 that you currently own. Alternatives to Cash Dividends • Stock Dividends • Existing shareholders receive additional shares of stock instead of cash dividends • Stock dividends represent a distribution of stock of less than 25% of total shares outstanding • Done usually if the firm wants to conserve cash • The number of shares is expressed as a percentage of current stock holdings.

Stock Dividend • A stock dividend is recorded at the current market price of the stock • For example, if the market price of the stock is $21, and the par value of the stock is $1, then stock dividend of 20,000 shares would be recorded as: • Retained Earnings 420,000 Common Stock (at $1 par) 20,000 Capital in excess of par 400,000

Stock Dividends Impact on Balance Sheet (Market price $21 per share) BEFORE 10% Stock DIVIDEND Common Stock (200,000 shares, $1 par) $200,000 Capital in Excess of Par $1,800,000 Retained Earnings $10,000,000 TOTAL COMMON STOCK EQUITY $12,000,000 AFTER 10% STOCK DIVIDEND (Stock price = $21) Common Stock (220,000 shares, $1 par) $220,000 Capital in Excess of Par $2,200,000 Retained Earnings $9,580,000 TOTAL COMMON STOCK EQUITY $12,000,000

e.g. a 2-1 split means that each investor will end up with twice as many shares as they had prior to the split. Alternatives to Cash Dividends • Stock Splits • If total shares will increase by more than 25%, the company will usually declare a stock split. • Expressed as a ratio to original shares. Link to Reuters

Stock split • Typically signals good news, in that the company expects to grow and increase stock price • Keeps stock price affordable for the greatest number of potential investors • Gives something of value to the shareholder without using up cash • Has no impact on the capital structure of the company

Stock Splits Impact on Balance Sheet BEFORE SPLIT Common Stock (200,000 shares, $1 par) $200,000 Capital in Excess of Par $1,800,000 Retained Earnings $10,000,000 TOTAL COMMON STOCK EQUITY $12,000,000 AFTER THE 2 to 1 STOCK SPLIT Common Stock (400,000 shares, $.50 par) $200,000 Capital in Excess of Par $1,800,000 Retained Earnings $10,000,000 TOTAL COMMON STOCK EQUITY $12,000,000

Impact of Stock Split on Shareholder • Before Split 100 shares x $10 = $1,000 value • After 2 for 1 Split • Per book argument (no increase in value) • 200 shares x $5 = $1,000 value • Investor positive reaction (value increases to $11.00 per share prior to split) • 200 shares x $5.50 = $1,100 value

Stock Repurchases • A firm buys back its own stock on the open market • A very common occurrence recently • By reducing the number of shares outstanding, earnings per share are increased • Rather than pay out a dividend, which would have immediate tax consequences for the investor, a stock repurchase increases the share price • Stock repurchase reverses the impact of dilution

Stock Repurchase Effect • Serves as a perfect replacement for a dividend payment to shareholders • Example: stock worth $60 per share pays $4 dividend. Shareholder has a Stock worth $60 and must pay tax on the $4 dividend • If dividend money used to repurchase stock instead, shareholder ends up with stock worth $64 with no immediate recognition of income