Variance Analysis

Variance Analysis. Topic Six by Dr. Ong Tze San tzesan@econ.upm.edu.my. Standard Costs. Standards are benchmarks or “norms” for measuring performance. Two types of standards are commonly used.

Variance Analysis

E N D

Presentation Transcript

Variance Analysis Topic Six by Dr. Ong Tze San tzesan@econ.upm.edu.my

Standard Costs Standards are benchmarks or “norms”for measuring performance. Two typesof standards are commonly used. Quantity standardsspecify how much of aninput should be used tomake a product orprovide a service. Cost (price)standards specify how much should be paid for each unitof the input.

Setting Standard Costs Accountants, engineers, purchasingagents, and production managerscombine efforts to set standards that encourage efficient future production.

QuantityStandards Final, deliveredcost of materials,net of discounts. Summarized in a Bill of Materials. Setting Direct Material Standards PriceStandards

RateStandards TimeStandards Often a singlerate is used that reflectsthe mix of wages earned. Use time and motion studies foreach labor operation. Setting Direct Labor Standards

RateStandards ActivityStandards The rate is the variable portion of the predetermined overhead rate. The activity is the base used to calculate the predetermined overhead. Setting Variable Overhead Standards

The purchasing manager is responsible for raw material purchase prices and the production manager is responsible for the quantity of raw material used. • The buying and using activities occur at different times. Raw material purchases may be held in inventory for a period of time before being used in production. Price and Quantity Standards Price and quantity standards are determined separately for two reasons:

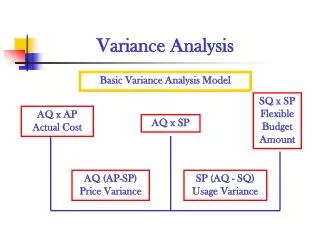

Price Variance Quantity Variance Difference betweenactual price and standard price Difference betweenactual quantity andstandard quantity A General Model for Variance Analysis Variance Analysis

Price Variance Quantity Variance Materials price varianceLabor rate varianceVOH spending variance A General Model for Variance Analysis Variance Analysis Materials quantity variance Labor efficiency variance VOH efficiency variance

Actual Quantity Actual Quantity Standard Quantity × × × Actual Price Standard Price Standard Price Price Variance Quantity Variance A General Model for Variance Analysis (AQ × AP) – (AQ × SP) (AQ × SP) – (SQ × SP) AQ = Actual Quantity SP = Standard Price AP = Actual Price SQ = Standard Quantity

Variances:Using the Factored Equations Materials price variance MPV = AQ (AP - SP) Materials quantity variance MQV = SP (AQ - SQ) Labor rate variance LRV = AH (AR – SR Labor efficiency variance LEV = SR (AH - SH) Variable manufacturing overhead spending variance VMSV = AH (AR - SR) Variable manufacturing overhead efficiency variance VMEV = SR (AH - SH)

Exh. 10-9 A Statistical Control Chart Warning signals for investigation • • Favorable Limit • • • • • Desired Value • Unfavorable Limit • 1 2 3 4 5 6 7 8 9 Variance Measurements