Download

1 / 32

320 likes | 510 Vues

Top Risks in Sponsored Projects Financial Compliance: A Specific Focus on Direct Costs vs. F&A Costs. Barbara Siegel, Acting Deputy Director of Grant and Contract Administration Tracy R. Walters, Director of Grant and Contract Financial Administration. Overview. Top Audit and Compliance Risks

E N D

Top Risks in Sponsored Projects Financial Compliance:A Specific Focus on Direct Costs vs. F&A Costs Barbara Siegel, Acting Deputy Director of Grant and Contract Administration Tracy R. Walters, Director of Grant and Contract Financial Administration

Overview • Top Audit and Compliance Risks • Institutional Fiscal Requirements • Challenges to University Compliance • Consequences of Noncompliance • On the Horizon

Top Compliance RisksSource: Huron Consulting • Cost Transfers • Effort Reporting • Subrecipient Monitoring • Direct Charging of Administrative Costs • Charging Costs at End of Award Period • Appropriate Cost Charging • Recharge Centers / Service Center Rates • Fixed Price Agreements • Financial Status Reports • Mandatory Cost Sharing

Institutional Fiscal Requirements • Meet federal cost accounting standards and comply with federal regulations in order to transact business with federal agencies. • Federal government wants assurance and verification that colleges and universities expend federal awards efficiently and effectively.

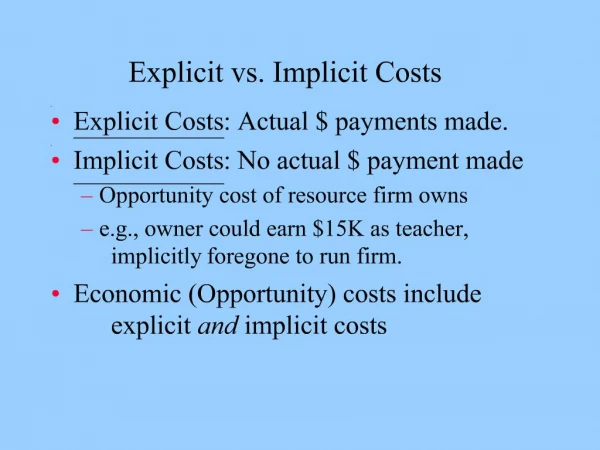

Institutional Fiscal Requirements • The Disclosure Statement (DS-2) is a document that explains (fiscal roadmap) how the University performs its cost accounting practices. The federal government wants to know how Yale treats direct costs and facilities & administrative costs (F&A), also referred to as direct & indirect costs, and complies with Cost Accounting Standards (CAS). In addition, it wants an assurance that institutions actually follow their disclosed practices. • DS-2 provides formal guidelines for: • Charging direct & F&A costs • Tracking & reporting cost sharing • Tracking & reporting time & effort • Accounting for Service Centers • Without an approved DS-2, future federal funding is at risk. • Required by Office of Management & Budget (OMB) Circular A-21.

Institutional Fiscal Requirements Disclosure Statement (DS-2) • Educational institutions subject to OMB Circular A-21 that received aggregate sponsored agreements totaling $25 million or more during their most recently completed fiscal year shall disclose their cost accounting practices by filing a Disclosure Statement.

Institutional Fiscal Requirements Cost Accounting Standards (CAS) Applicable to Educational Institutions • OMB Circular A-21, Subsections C.10-14 impose 4 of the 19 CAS on educational institutions: • CAS 501 – Consistency in estimating, accumulating and reporting costs • CAS 502 – Consistency in allocating costs incurred for the same purpose • CAS 505 – Accounting for unallowable costs • CAS 506 – Cost accounting period must coincide with Institution’s fiscal year

Institutional Fiscal Requirements • CAS 502 – Consistency in allocating costs incurred for the same purpose • Requires that “…all costs incurred for the same purpose, in like circumstances, be treated as either direct costs only or F&A costs only with respect to final cost objectives” • Prohibits charging as a direct cost any cost for which other costs incurred for the same purpose, in like circumstances, have been included in any F&A cost pool to be allocated to that or any other final cost objective.

Challenges to University ComplianceDirect Costs vs. F&A Costs Federal OMB RegulationsCircular A-21 A cost is allocable to a sponsored agreement if (1) it is incurred solely to advance the work under the sponsored agreement; (2) it benefits both the sponsored agreement and other work of the institution, in proportions that can be approximated through use of reasonable methods; or (3) it is necessary to the overall operation of the institution and, in light of the principles provided in this Circular, is deemed to be assignable in part to sponsored projects Where the purchase of equipment or other capital items is specifically authorized under a sponsored agreement, the amounts thus authorized for such purchases are assignable to the sponsored agreement regardless of the use that may subsequently be made of the equipment or other capital items involved.

Challenges to University ComplianceDirect Costs vs. F&A Costs Federal OMB Regulations Circular A-21 cont’d Any costs allocable to a particular sponsored agreement under the standards provided in this Circular may not be shifted to other sponsored agreements in order to meet deficiencies caused by overruns or other fund considerations, to avoid restrictions imposed by law or by terms of the sponsored agreement, or for other reasons of convenience. Any costs allocable to activities sponsored by industry, foreign governments or other sponsors may not be shifted to federally sponsored agreements.

Challenges to University ComplianceDirect Costs vs. F&A Costs Health and Human Services (HHS) Policy • A “direct cost” is any cost that can be specifically identified with a particular project, program, or activity or that can be directly assigned to such activities relatively easily and with a high degree of accuracy. Direct costs include, but are not limited to, salaries, travel, equipment, and supplies directly benefiting the grant-supported project or activity. • Most organizations also incur costs for common or joint objectives that, therefore, cannot be readily identified with an individual project, program, or organizational activity. Facilities operation and maintenance costs, depreciation, and administrative expenses are examples of costs that usually are treated as F&A costs. • The organization is responsible for presenting costs consistently and must not include costs associated with its F&A rate as direct costs.

Challenges to University ComplianceDirect Costs vs. F&A Costs Application of Federal Regulations: • Costs charged to sponsored projects must be allowable, that is, • Allowable: To be allowable, costs must be reasonable and necessary; be allocable to federally sponsored projects under the principles and methods provided in OMB Circular A-21; be given consistent treatment; and conform to any limits or exclusions set forth in A-21 or the terms and conditions of the award (defined specifically in OMB Circular A-21 Section J General Provisions of the cost principles). • Reasonable and Necessary: A cost may be considered reasonable if the nature of the goods or services acquired or applied, and the amount involved therefore, reflect the action that a prudent person would have taken under the circumstances prevailing at the time the decision to incur the cost was made.

Challenges to University ComplianceDirect Costs vs. F&A Costs Application of Federal Regulations cont’d: • Costs charged to sponsored projects must be allocable, that is, • Allocable: A cost is allocable to a particular cost objective (i.e., a specific function, project, sponsored agreement, department, or the like) if the goods or services involved are chargeable or assignable to such cost objective in accordance with relative benefits received or other equitable relationship. • Consistently treated: All costs incurred for the same purpose, in like circumstances, are either direct costs only or F&A costs only with respect to final cost objectives. • Conform to any limitations or exclusions: Costs must conform to any limitations or exclusions set forth in these principles or in the sponsored agreement as to types or amounts of cost items.

Challenges to University ComplianceDirect Costs vs. F&A Costs Application of Federal Regulations cont’d: • Direct costs of sponsored projects must be incurred solely to advance the work of the project (or interrelated projects) and be reasonable and necessary for the performance of the project • Costs must be allowable as either an indirect or direct cost only, not both • Cost accounting standards require institutions to be consistent in the way that costs are estimated, accumulated and reported and in the treatment of costs as either direct or indirect • Institutions must exercise caution when direct charging costs normally considered as facilities and administration (F&A) types of expenses

Challenges to University ComplianceDirect Costs vs. F&A Costs Yale Policies • Under federal regulations and sponsor requirements, departmental types of expenses (including but not limited to administrative or clerical salaries, office supplies, postage, local telephone costs, photocopy costs, network charges, cell phones, etc) should normally be treated as an F&A cost and recovered through the F&A cost rate. • In unlike circumstances where the nature of the work performed on a project requires extensive departmental support, some administrative-type expenses may be treated as direct costs.

Challenges to University ComplianceDirect Costs vs. F&A Costs Yale Policies Federal vs. Nonfederal: • Many non-federal sponsors do not fully reimburse the University for its Facilities and Administrative (F&A) costs (commonly referred to as indirect costs) on sponsored awards. In recognition of this practice, Yale expects these non-federal sponsored projects to directly pay for costs which are normally F&A costs if: • the terms and conditions do not specifically prohibit such costs; and • a benefit exists to the sponsored project. • While some state awards appear to be state funded, Yale Federal pass-through awards received from a state agency must be treated as Federal Funded (may not be easily identifiable) • State contracts that stipulate the University must comply with OMB Circular A-21 regulations within the contract must be treated as a Federal Funded Award.

Challenges to University ComplianceDirect Costs vs. F&A Costs Common F&A Type Expenses: • Administrative and Clerical Salaries • ITS Communications Charges • Local Telephone and Internet Charges • Cellular Telephone Charges • Dues and Memberships • Office Equipment (Facsimiles, Copiers, Printers) • Computer Desktop/Laptop Purchases • Books and Periodicals • Paper Supplies and Envelopes • Lab Coats and Laundering • Annual Safety Cabinet/Hood Certifications • Malpractice Insurance • Entertainment

Challenges to University ComplianceDirect Costs vs. F&A Costs Key Concepts: • Ensure that costs directly charged to an award are for the direct benefit of the project. • Use and follow University guidelines on proper cost allocation methodologies. • Ensure accountability and fiscal integrity of expenses.

Challenges to University ComplianceDirect Costs vs. F&A Costs Key concepts • “Unlike circumstances”: A cost normally treated as an F&A cost may be appropriate as a direct cost on a federally sponsored project if: • The cost is allowable (defined as necessary, reasonable, and allocable) and permissible under the law, terms and conditions of the award, and the circumstances are “unlike” • Unlike circumstances may be determined by the nature of the project (see examples in OMB A-21, Exhibit C) • The project is considered a “major project” (Note: There are some projects that are not considered “major” but may still qualify as “unlike circumstances.”)

Challenges to University ComplianceDirect Costs vs. F&A Costs Key concepts • Examples of "major project" where direct charging of administrative or clerical staff salaries may be appropriate: • Large, complex programs such as General Clinical Research Centers, Primate Centers, Program Projects, environmental research centers, engineering research centers, and other grants and contracts that entail assembling and managing teams of investigators from a number of institutions.

Challenges to University ComplianceDirect Costs vs. F&A Costs • Major Project Examples cont’d • Projects which involve extensive data accumulation, analysis and entry, surveying, tabulation, cataloging, searching literature, and reporting (such as epidemiological studies, clinical trials, and retrospective clinical records studies). • Projects that require making travel and meeting arrangements for large numbers of participants, such as conferences and seminars. • Projects whose principal focus is the preparation and production of manuals and large reports, books and monographs (excluding routine progress and technical reports).

Challenges to University ComplianceDirect Costs vs. F&A Costs • Major Project Examples cont’d • Projects that are geographically inaccessible to normal departmental administrative services, such as research vessels, radio astronomy projects, and other research fields sites that are remote from campus. • Individual projects requiring project-specific database management; individualized graphics or manuscript preparation; human or animal protocols; and multiple project-related investigator coordination and communications.

Challenges to University ComplianceDirect Costs vs. F&A Costs Non Personnel Examples • ITS Communications Charges • Dedicated line used to conduct a telephone survey or 24 hour “Hot-line” specified within a project’s scope. • T-1 Line used exclusively for computational analysis or constant transmission of study data associated with a specified project. • Toll-free (i.e., 1-800) line for study participants to contact researchers regarding a study.

Challenges to University ComplianceDirect Costs vs. F&A Costs Non Personnel Examples (cont’d): • Computer Desktop/Laptop Purchases • May be allowable as a direct cost in specific situations where the nature of the research requires a computer, e.g., the computer is attached to a piece of equipment and is required for collection and/or analysis of information/data for the sponsored project or the computer needed to record data while in the field, such as an archaeological site. • Because a computer is potentially used for many different activities (instruction, research, and administration), it may not easily be assigned to any one of these activities. Thus, computer costs are normally an F&A expense and included in the University’s F&A rate calculation. • There are some sponsors that prohibit the purchase of computers while others require that the computer must be exclusively used for the research. Yet other sponsors state “primarily”.

Challenges to University ComplianceDirect Costs vs. F&A Costs Non Personnel Examples (cont’d): • Cellular Telephone Charges • Dedicated specifically and exclusively for safety measures involving project staff required to work in high crime areas or potentially dangerous populations • Dues and Memberships • Not typically allowable as a Direct cost • Books and Periodicals • Books and subscriptions not available in the University or departmental library and specifically identifiable to a project. • Paper Supplies and Envelopes • Project surveys, mailings and return metered envelopes supporting projects involving human participants.

Challenges to University ComplianceDirect Costs vs. F&A Costs • “Exceptional Circumstances” Proposals • The project scope of work must qualify as a major project under which exceptions could be granted • The budget should include “exceptional” costs • The budget justification must describe the rationale for the exceptional costs. • The project narrative should also describe the exceptional circumstances • Institutional approval and Sponsor’s acceptance is required; Provided that the expense is budgeted, justified and not specifically denied in the notice of award.

Challenges to University ComplianceDirect Costs vs. F&A Costs • Challenges of policy/procedure Implementation: • Yale Policy/Procedures and Departmental Training • Understanding what is treated as a direct cost and when there may be acceptable exceptions for the direct charging of F&A type expenses • Breaking old habits and routines

Consequences of Non-Compliance • Disallowance of costs • Published and publicly available audit findings • Greater audit oversight • Adverse effects on Facilities & Administrative rate negotiations • Loss of future funding • Loss of University credibility

On the Horizon • Increasing number of federal desk reviews, federal on-site visits and cost reviews. • Tougher A-133 compliance supplements and audits. • Greater emphasis placed on the Statement on Auditing Standards No. 112 (SAS112) • Substantially increases policy and procedural documentation of institutions’ internal control processes. • Lowers the bar on audit findings • An inappropriate or disallowed charge may result in findings regardless of materiality of charges.

Resources OMB Circular A-21 (http://www.whitehouse.gov/omb/circulars/a021/a21_2004.html) OMB Circular A-133 (http://www.whitehouse.gov/omb/circulars/a133/a133.html) Understanding SAS 112(http://www.aicpa.org/Professional%2BResources/Accounting%2Band%2BAuditing/Audit%2Band%2BAttest%2BStandards/Practice%2BAids%2Band%2BTools/Understanding%2BSAS%2BNo%2B112.htm) NIH Grants Policy & Guidance (http://grants.nih.gov/grants/policy/policy.htm) NSF Proposal and Award Policies and Procedures Guide (New and Effective January 2009) (http://www.nsf.gov/pubs/policydocs/pappguide/nsf09_1/index.jsp)

Resources NSF Proposal and Award Policies and Procedures Guide (http://www.nsf.gov/pubs/policydocs/pappguide/nsf08_1/index.jsp) Policy 1403 Charging of Administrative or Clerical Salaries and Certain Other Expenses to Federal Funds(http://www.yale.edu/ppdev/policy/1403/1403.pdf) Policy 1405 Charging of Facilities and Administrative Type Expenses to Non-Federal Sponsored Projects (http://www.yale.edu/ppdev/policy/1405/1405.pdf) Procedure 1305 PR.04 Unallowable Costs(http://www.yale.edu/ppdev/Procedures/gc/1305PR.04UnallowbleCosts.pdf) Direct Charging of Network and Certain Other Administrative Costs to Sponsored Awards (http://www.yale.edu/researchadministration/documents/NetworkChargingCentralCampus041007.pdf