Download

1 / 24

240 likes | 291 Vues

Explore the correlation between short and long-run economic theories using a comprehensive analysis of economic policy and framework. Discover the impact of wage and price changes on economic recovery, and learn to apply macroeconomic concepts to real-world scenarios such as Japan's Lost Decade. Delve into aggregate demand and supply dynamics and understand the role of economic policy in shaping the economy. This detailed study from "Modern Macroeconomics" provides a deep insight into the interplay between economic indicators and policy decisions, offering a holistic view of macroeconomic performance.

E N D

P R E P A R E D B Y Modern Macroeconomics:From the Short Run to theLong Run Economics: Principles, Applications, and Tools O’Sullivan, Sheffrin, Perez 6/e. They could not have differed more sharply on economic theory and policy. FERNANDO QUIJANO, YVONN QUIJANO, AND XIAO XUAN XU

A P P L Y I N G T H E C O N C E P T S What went wrong for the Japanese economy during its decade-long economic downturn? Japan’s Lost Decade What are the links between presidential elections and macroeconomic performance? Elections, Political Parties, and Voter Expectations Will increases in health-care expenditures crowd out consumption or investment spending? Increasing Health-Care Expenditures and Crowding Out 1 2 3

LINKING THE SHORT RUN AND THELONG RUN 15.1 • The Difference between the Short and Long Run ●short run in macroeconomicsThe period of time in which prices do not change or do not change very much. ●long run in macroeconomicsThe period of time in which prices have fully adjusted to any economic changes. • Should economic policy be guided by what we expect to happen in the short run, as Keynes thought, or what we expect to happen in the long run, as Friedman thought? To answer this question, we need to know two things: • 1 How does what happens in the short run determine what happens in the long run? • 2 How long is the short run?

LINKING THE SHORT RUN AND THELONG RUN 15.1 • Wages and Prices and Their Adjustment over Time ●wage–price spiralThe process by which changes in wages and prices cause further changes in wages and prices.

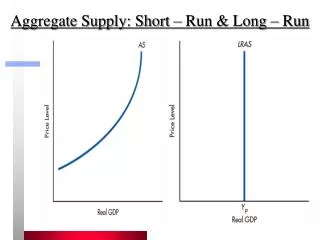

HOW WAGE AND PRICE CHANGES MOVE THE ECONOMY NATURALLY BACK TO FULL EMPLOYMENT 15.2 Using aggregate demand and aggregate supply, we can illustrate graphically how changing prices and wages help move the economy from the short to the long run. 1 Aggregate demand. ●aggregate demand curveA curve that shows the relationship between the level of prices and the quantity of real GDP demanded. 2 Aggregate supply. ●short-run aggregate supply curveA relatively flat aggregate supply curve that represents the idea that prices do not change very much in the short run and that firms adjust production to meet demand. ●long-run aggregate supply curveA vertical aggregate supply curve that reflects the idea that in the long run, output is determined solely by the factors of production and technology.

HOW WAGE AND PRICE CHANGES MOVE THE ECONOMY NATURALLY BACK TO FULL EMPLOYMENT 15.2 • Returning to Full Employment from a Recession • FIGURE 15.1How the Economy Recovers from a Downturn If the economy is operating below full employment, as shown in Panel A, prices will fall, shifting down the short-run aggregate supply curve, as shown in Panel B. This will return output to its full-employment level.

HOW WAGE AND PRICE CHANGES MOVE THE ECONOMY NATURALLY BACK TO FULL EMPLOYMENT 15.2 • Returning to Full Employment from a Boom • FIGURE 15.2How the Economy Returns from a Boom If the economy is operating above full employment, as shown in Panel A, prices will rise, shifting the short-run aggregate supply curve upward, as shown in Panel B. This will return output to its full-employment level.

HOW WAGE AND PRICE CHANGES MOVE THE ECONOMY NATURALLY BACK TO FULL EMPLOYMENT 15.2 • Returning to Full Employment from a Boom • In summary: • If output is less than full employment, prices will fall as the economy returns to full employment. • If output exceeds full employment, prices will rise and output will fall back to full employment.

HOW WAGE AND PRICE CHANGES MOVE THE ECONOMY NATURALLY BACK TO FULL EMPLOYMENT 15.2 • Economic Policy and the Speed of Adjustment • FIGURE 15.3Using Economic Policy to Fight a Recession Rather than letting the economy naturally return to full employment at point b, economic policies could be implemented to increase aggregate demand from AD0 to AD1 to bring the economy to full employment at point c. The price level within the economy, however, would be higher.

1 A P P L I C A T I O N JAPAN’S LOST DECADE APPLYING THE CONCEPTS #1: What went wrong for the Japanese economy during its decade-long economic downturn? • Following World War II, Japan’s economy grew rapidly. However, around 1992 it ground to a halt, and by 1993–1994 the country was suffering from a recession. Prices stopped rising, and deflation—falling prices—began in Japan. • Deflation might sound like a good thing, but it actually caused a lot of problems for Japan. • Wholesale prices fell for several years. • Also, starting in 1990, real-estate prices fell nearly 50 percent. • Banks lost vast sums of money on real-estate-related loans. • For Japanese borrowers, falling prices—a negative inflation rate—raised the real rate of interest they were paying on their existing loans, essentially increasing their burden of debt. • Result: aggregate demand was weak. • Restoring the health of the banking system was a major priority. Toward the beginning of the next decade of 2000, the economy began to improve somewhat. Beginning in 2003, the Japanese economy grew by 2.3 percent, up from nearly no growth at all.

HOW WAGE AND PRICE CHANGES MOVE THE ECONOMY NATURALLY BACK TO FULL EMPLOYMENT 15.2 • Liquidity Traps ●liquidity trapA situation in which nominal interest rates are so low, they can no longer fall. • Political Business Cycles ●political business cycleThe effects on the economy of using monetary or fiscal policy to stimulate the economy before an election to improve reelection prospects.

2 A P P L I C A T I O N ELECTIONS, POLITICAL PARTIES, AND VOTER EXPECTATIONS APPLYING THE CONCEPTS #2: What are the links between presidential elections and macroeconomic performance? • The original political business cycle theories focused on incumbent presidents trying to manipulate the economy in their favor to gain reelection. Subsequent research began to incorporate other, more realistic factors. • The first innovation was to recognize that political parties could have different goals or preferences. • Republicans historically have been more concerned about fighting inflation, whereas Democrats have placed more weight on reducing unemployment. • The second major innovation was to recognize that the public would anticipate that politicians will try to manipulate the economy. • If the public is not sure who will win the election, the outcome will be a surprise to them—a contractionary surprise if Republicans win and an expansionary surprise if Democrats win.

UNDERSTANDING THE ECONOMICS OFTHE ADJUSTMENT PROCESS 15.3 • FIGURE 15.4How the Changing Price Level Restores the Economy to Full Employment With the economy initially below full employment, the price level falls, as shown in Panel A, stimulating output. In Panel B, the lower price level decreases the demand for money and leads to lower interest rates at point d. In Panel C, lower interest rates lead to higher investment spending at point f. As the economy moves down the aggregate demand curve from point a toward full employment at point b in Panel A, investment spending increases along the aggregate demand curve.

UNDERSTANDING THE ECONOMICS OFTHE ADJUSTMENT PROCESS 15.3 Why changes in wages and prices restore the economy to full employment: (1) Changes in wages and prices change the demand for money. (2) This changes interest rates, which then affect aggregate demand for goods and services and ultimately GDP.

UNDERSTANDING THE ECONOMICS OFTHE ADJUSTMENT PROCESS 15.3 • The Long-Run Neutrality of Money • FIGURE 15.5Monetary Policy in the Short Run and the Long Run As the Fed increases the supply of money, the aggregate demand curve shifts from AD0 to AD1 and the economy moves to point a. In the long run, the economy moves to point b.

UNDERSTANDING THE ECONOMICS OFTHE ADJUSTMENT PROCESS 15.3 • The Long-Run Neutrality of Money • FIGURE 15.6The Neutrality of Money Starting at full employment, an increase in the supply of money from Ms0 to Ms1 will initially reduce interest rates from rF to r0 (from point a to point b) and raise investment spending from IF to I0 (point c to point d). We show these changes with the red arrows. The blue arrows show that as the price level increases, the demand for money increases, restoring interest rates and investment to their prior levels—rF and IF, respectively. Both money supplied and money demanded will remain at a higher level, though, at point e.

UNDERSTANDING THE ECONOMICS OFTHE ADJUSTMENT PROCESS 15.3 • The Long-Run Neutrality of Money ●long-run neutrality of moneyA change in the supply of money has no effect on real interest rates, investment, or output in the long run.

UNDERSTANDING THE ECONOMICS OFTHE ADJUSTMENT PROCESS 15.3 • Crowding Out in the Long Run • FIGURE 15.7Crowding Out in the Long Run Starting at full employment, an increase in government spending raises output above full employment. As wages and prices increase, the demand for money increases, as shown in Panel A, raising interest rates from r0 to r1 (point a to point b) and reducing investment from I0 to I1 (point c to point d ). The economy returns to full employment, but at a higher level of interest rates and a lower level of investment spending.

3 A P P L I C A T I O N INCREASING HEALTH-CARE EXPENDITURES AND CROWDING OUT APPLYING THE CONCEPTS #3: Will increases in health-care expenditures crowd out consumption or investment spending? • In 1950, health-care expenditures in the United States were 5.2 percent of GDP; by 2000, this share had risen to 15.4 percent. • Since 1950, the average life span has increased by 1.7 years per decade. • Two economists, Charles I. Jones and Robert E. Hall, go further and suggest normal increases in economic growth will propel health-care expenditures to approximately 30 percent of GDP by the mid-century. • Their argument is that as societies grow wealthier, individuals face the tradeoff of buying more goods (automobiles or cars) to enjoy their current life span or spending more on health care to extend their lives. • Assuming this argument is correct and health-care expenditures increase, what other component of GDP will fall? • If investment is crowded out, living standards would fall in the long run, reducing the ability to consume both health and non-health goods. • Spending on health would then come at the expense of spending on consumer durables or larger houses. That would be the preferred outcome.

CLASSICAL ECONOMICS IN HISTORICAL PERSPECTIVE 15.4 • Say’s Law Classical economics is often associated with Say’s law, the doctrine that “supply creates its own demand.” Keynes argued that there could be situations in which total demand fell short of total production in the economy for extended periods of time. • Keynesian and Classical Debates If wages and prices are not fully flexible, then Keynes’s view that demand could fall short of production is more likely to hold true. However, over longer periods of time, wages and prices do adjust and the insights of the classical model are restored.

K E Y T E R M S aggregate demand curve liquidity trap long-run aggregate supply curve long run in macroeconomics long-run neutrality of money political business cycle short-run aggregate supply curve short run in macroeconomics wage–price spiral