Cost

Cost. Cost concepts. MEANING OF COST. COST is the Expenditure incurred on various inputs to produce goods and services. Cost function : Functional relationship between cost and output. C=f(q) Where f=functional relationship c= cost of production q=quantity of product. TYPE OF COST.

Cost

E N D

Presentation Transcript

Cost concepts MEANING OF COST • COST is the Expenditure incurred on various inputs to produce goods and services. • Cost function : Functional relationship between cost and output. • C=f(q) • Where f=functional relationship • c= cost of production • q=quantity of product

Money Vs. Real Cost Money cost : Money expenses incurred by a firm for producing a commodity or service. It is actually paid hence recorded in the books of accounts of a firm. Therefore it is also known as accounting cost. Money costs are generally referred to as production cost as well. Ex: Salaries to employees, Rent on Building Real Cost: The value of exertions of labour and waitings and sacrifices required for saving the capital is the real cost. It is not measurable hence not paid to anyone ,therefore not shown in the books of accounts of a firm.

EXPLICIT Vs IMPLICIT COST EXPLICIT COST :Actual payment made on hired factors of production. For example wages paid to the hired labourers, rent paid for hired accommodation, cost of raw material etc IMPLICIT COST : Cost incurred on the self - owned factors of production. For example, interest on owners capital, rent of own building, salary for the services of entrepreneur etc.

FIXED Vs VARIABLE COST Fixed cost : Are the cost which are incurred on the fixed factors of production. These costs remain fixed whatever may be the scale of output. These costs are present even when the output is zero. These costs are present in short run but disappear in the long run. Also called as “supplementary cost”. Numerical example of fixed cost Output:0 1 2 3 4 5 TFC Rs:20 20 20 20 20 20 Variable Cost : Are those costs which vary directly with the variation in the output. These costs are incurred on the variable factors of production. These costs are also called “prime costs”, “Direct cost” or “avoidable cost”. These costs are zero when output is zero. Numerical example, Output:0 1 2 3 4 5 TVC 0 10 16 25 38 55

PRODUCTION Vs SELLING COST PRODUCTION COST Money expenditure of producing certain quantities of output. Ex: cost of machine,Salaries to employees, Expenses on purchase of raw materials SELLING COST Expenditure on selling the putput, ie., to make the product reaching the consumer. Ex: Expenses on Advertisement, sales promotion, commission to sales staff.

TOTAL COST The sum of total fixed cost and total Variable cost is the total cost of producing certain level of output. TFC remains same at all levels of output but positive when the output is zero. TVC changes along with the output but zero when the output is zero. TC = TFC + TVC TFC = TC- TVC TVC =TC-TFC

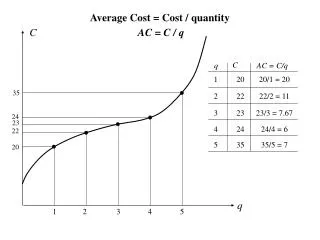

AVERAGE COST Average cost is the cost of producing per unit of output. It is the sum of average fixed cost & average variable cost. Average cost of production is inversely related with average product. As long as the output rises AC falls and when the output begins falling AC rises. AC = TC/ Q = TFC + TVC / Q = AFC + AVC

MARGINAL COST Marginal cost is the change in total cost by producing one more or less unit of output. Marginal cost is the change in Total Variable cost when one more or less output is produced as the TFC remains same at all levels of output. MC = TCn-TC n-1 = TVCn-TVC n-1

RELATIONSHIP BETWEEN AC & MC • Relationship 1.When Ac is falling ,AC>MC 2.When AC is constant AC=MC 3.When AC is rising AC<MC 4.MC curve cuts the AC Curve at its lowest point. 5.Both AC & MC curves are U shaped.

Important formulae at a glance1. TFC = TC – TVC or TFC=AFC x output or TFC = TC at 0 output.2. TVC = TC – TFC or TVC = AVC x output or TVC =ΣMC3. TC = TVC + TFC or TC = AC x output or TC = Σ MC + TFC 4. MCn=TCn – TCn-1 or MCn= TVCn – TVCn-1 5. AFC = TFC / Output or AFC = AC-AVC or ATC – AVC 6. AVC = TVC / Output or AVC = AC-AFC 7. AC = TC / Output or AC=AVC + AFC