Download

1 / 21

210 likes | 324 Vues

This study investigates the Black-Scholes model's applicability in American markets, contrasting dynamic trading with fixed-time trading. It delves into option trading concepts, including calls, puts, and the fees involved. The research also examines the validity of Black-Scholes generated values against historical data across various industries and volatility levels. By utilizing Java for simulation and analysis, the results highlight the model's effectiveness in estimating call options while identifying limitations such as market crashes and external influences. Ultimately, it emphasizes the necessity of human judgment in trading decisions.

E N D

Aileen Wang Period 5 An Analysis of Dynamic Applications of Black-Scholes

Purpose Investigate Black-Scholes model Apply the B-S model to an American market Dynamic trading vs. fixed-time trading

What is option trading? • Option trading is a variation of market trading • Calls and puts • Fee charged for making a contract • Owner (buyer) of the contract has the option to exercise or to not exercise contract at time of maturity • More controlled • Investor has more clout • Not necessarily at market price

Questions To what kind of stock options is the Black-Scholes model most applicable to? Validity: How does Black-Scholes generated call and put values compare with the actual historical values? Variable factors: Stocks of a different industry (finance sector stocks vs. agriculture vs. technology) Different volatilities, different price levels

Scope of Study • Analysis of input variables • What are they? • How will they be obtained? • What formulas are necessary to calculate them?

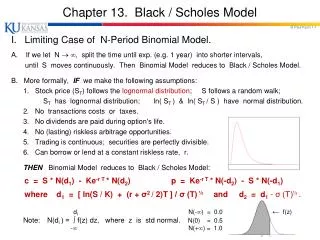

Related Studies • 1973: Black-Scholes created • 1977: Boyle’s Monte Carlo option model • Uses Monte Carlo applications of finance • 1979: Cox, Ross, Rubenstien’s bionomial options pricing model • Uses the binomial tree and a discrete time-frame • Roll, Geske, and Whaley formula • American call, analytic solution

Background Information • Black-Scholes: Two parts • Black-Scholes Model • Black-Scholes equation: partial differential equation • Catered to the European market • Definite time to maturity • American Market • Buy and sell at any time • More dynamic and violatile

Procedure and Method • Main language: Java • Outputs: • Series of calls and puts • Spreadsheet, time-series plot • Inputs • Price • Volatility • Interest rate • Test data and historical data

AAPL – Sample Case • At a given time t, the stock price for AAPL was 239.94. • APPL options used are ranged from 90.00 to 190.00 in increasing increments of 5.00. • Three days until maturity, volatility of 20%, and a risk free rate of 0.35%

AAPL – Sample Case • Graphs comparing call and put values of expected versus actual.

AAPL – Sample Case • Model is a good estimator for call, but put values tend to deviate as strike price increases

Limitations • Why doesn’t B-S always work? • Out of the money • Strike price is above stock price, option has no value • Disregards risk such as • Stock market crashes • Unexpected outside influences (terrorist attacks, mergers and acquisitions) • Typos?

Limitations • B-S has many assumptions that are far from valid in real life: • Disregard of extreme moves • Assumes instant, cost-free trading • Continuous time and continuous trading • Standard trading (volatility risk of currency adjustments)

Limitations • Disregarding extreme moves • B-S model does not cater to external influences • Influences are not predictable • Unforeseen risk = risk that cannot be avoided by investors

Limitations • Instant, cost-free trading • Real life trading is not instant • Investor through system • System orders on trading floor • Order is put in • Not cost free either • Commission on stock trades • Fee for setting an option contract

Limitations • Continuous time and continuous trading • Several gaps in time on the stock exchange • Big gaps: Friday afternoon – Monday morning • Daily gaps: Tuesday afternoon – Wednesday morning • Holidays: Stock exchange is not open for Christmas • Company/news changes during the gaps are not reflected in the market immediately

Limitations • Standard trading • Standard trading means that currency exchange rates stay constant over time • FOREX • Market for currency trading • In the real world, currencies vary on a daily basis just like stocks

Results • Explore • Option pricing with mathematics • Validity of the model • Comparing stocks of different volatility, industry, and nature • Further research • Comparison with other mathematical models • Application into markets in other countries

Concluding thoughts • Models • Models are only models • Models cannot ever predict human behavior • Business and investing is not purely mathematical • Always use proper human judgment • Never rely on models to make all the decisions, financially or otherwise