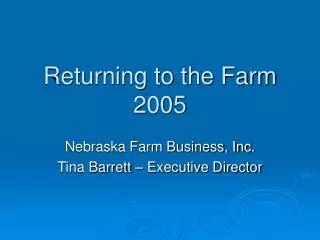

Returning to the Farm 2005

410 likes | 579 Vues

Returning to the Farm 2005. Nebraska Farm Business, Inc. Tina Barrett – Executive Director. Nebraska Farm Business, Inc. Services We Offer: Tax Planning Tax Preparation W-2/1099 Preparation Monthly Accounting Payroll Business Planning Financial Analysis. Nebraska Farm Business, Inc.

Returning to the Farm 2005

E N D

Presentation Transcript

Returning to the Farm 2005 Nebraska Farm Business, Inc. Tina Barrett – Executive Director

Nebraska Farm Business, Inc. • Services We Offer: • Tax Planning • Tax Preparation • W-2/1099 Preparation • Monthly Accounting • Payroll • Business Planning • Financial Analysis

Nebraska Farm Business, Inc. • Our Averages Data Is Published and Distributed to Lenders, Senators, Educators, Farmers & More.

Net Farm Income Trend 2004 New Record NFI: $78,930

NFI vs. Family Living Trend 2004 Family Living Expense: $44,811 (Avg. of 145 Farms)

Net Farm Inc. vs Gov’t Pmts 1998-2001 – Government Payments Exceed Net Farm Income

Net Return Per Acre Trend Irrigated Corn, Nebraska Trend Net Return Per Acre, Including Labor & Management Charge.

So you think…. “All good things come to those who wait” Just try not filing your tax return, and see all the “good” things the IRS has waiting for you!

Returning to the Farm • Things to think about first: • Do you want to farm together or farm together separately? • Do you want to make management decisions together or on your own? • Will you share equipment or have separate lines? • Are you willing to risk financial stability of older operations with a new addition?

Returning to the Farm • If you will farm together: • What entity will you choose? • How will the labor and management be split? • How will estate planning effect both farm and non-farm heirs? • Will government payment limitations be a problem?

Returning to the Farm • If you will farm together separately: • What entities will you choose? • How will labor be shared? • How will equipment be shared? • Will the farm-heirs be able to survive alone with the estate planning in place?

Entity Selection Reasons for Entities • Estate Planning • Business Succession • Income Tax

Estate Planning • Maintain Cash Flow & Financial Security • Assure Equitable Split of Assets Among All Heirs • Minimize Estate Taxes • Concerns of Remarriage of Surviving Spouse

Business Succession • Team Approach to Management • “Power” Struggle • Fair Compensation • Expecting the Unexpected • Phased-Out Retirement

Income Tax • Savings Are Possible With Entities • Reduction in Self-Employment (SE) Greatest • Tax Savings Come With Accounting Costs

Choosing the Right Entity • Sole Proprietor • Partnership • LLC/LLP • S-Corporation • C-Corporation

Sample Farm Family Planning • Jim and Jane Farmer Want to Know if They Should Have a Different Entity than a Sole Proprietor. • They Have Two Children and Do Not Itemize.

Sample Farm Family Planning • Why would you choose a C-Corp? • Remember, this example did not include things like the deduction of: • Health Insurance, • Medical Expenses, • Retirement Plans, • Other Fringe Benefits

Example of Savings from Benefits Fringe Benefits: • Health Insurance - $10,000 / year • Medical/Prescription Costs - $4,500 / year • Retirement Plan - $3,000 / year Total Benefits: $17,500 / year

Tax Drawbacks to Entities • Loss of Step-Up in Basis • Machinery contributed to a corporation goes in at your basis (No tax consequences) • Machinery in a corporation does not receive a step-up in basis at the time of death, the stock owned receives the step-up.

Tax Drawbacks to Entities • Loss of Step-Up in Basis • Example: • FMV of Machinery = $500,000 • Basis in Machinery = $200,000 (Amount Remaining to Depreciate) • If owned by individual at time of death, the surviving spouse inherits the machinery with a new basis = FMV and pays no tax upon the sale of assets

Tax Drawbacks to Entities • Loss of Step-Up in Basis • Example: • FMV of Machinery = $500,000 • Basis in Machinery = $200,000 (Amount Remaining to Depreciate) • If a corporation owns the machinery, it must pay tax on the sale of the assets and the individual must pay tax on the dividends to have use of the cash.

Entities & FSA • What Should You Keep In Mind Regarding FSA Payment Limitations: • Sole-Proprietors each get payment limits • Partnerships look to the number of partners • S & C Corps are immediately consolidated into one payment limitation.

Entities & FSA • What Should You Keep In Mind Regarding FSA Payment Limitations: • Payment Limitations Must Be Considered to Make Sure You Don’t Lose Payments! • Or at least make sure the tax savings is worth losing the payments.

Entities & FSA • Remember: • The Entity Should Have Significant Contribution of Active Personal Management • And, It Should Not Exist Only To Receive More Payments (or to Avoid Tax)

Retirement Savings • With Reduced Social Security Payments – There Are Reduced Retirement Benefits • What if Social Security Is Not Longer Available? • Saving on Own Is Important

Retirement Savings • What Would Happen If You Contribute ~¼ of tax savings to Retirement Per Year (or $5,000)?

Retirement Savings * Still Have $12,377 Extra $’s For Reinvestment or Debt Reduction

Retirement Savings * Still Have $7,377 Extra $’s For Reinvestment or Debt Reduction

Successful Entity Organization • Corporation Get Extra 15% Tax Bracket, • Individual Can Get All Medical, etc, Benefits Tax Free • Individual Taxpayer Pays on Wage and Rent Received.

Successful Entity Organization • Partnership Can Own Machinery and Operate Farm. • Can Enter Partnership 80% - 20% and Switch Ownership Over Time,

Successful Entity Organization • LLC Allows Shared Investment Of Machinery While Maintaining Separate Operations. • Income Split Between Individuals

Other Things to Remember • Adding Entities, Adds Bookwork, • Adding Entities also Costs Money: • Legal Fees to Set Up • Accounting Fees to Prepare Tax Returns • Adding Payroll, etc. Can Cause Headaches!

Professional Cost of An Entity CorporationsPart/LLC’s Set Up Cost $500-$1,000 $500-$1,000 Business Return $500 $400 Each Individual $100 $100 Payroll Forms $50 N/A * Does Not Include Tax Planning (+ ~$150), Accounting ($420 – 1st Set, $250 – 2nd Set)

Nebraska Farm Business, Inc. 3815 Touzalin Ave Suite 105 Lincoln, NE 68507-1600 (402) 464-NFBI info@nfbi.net www.nfbi.net