Exploring Endogenous Expectations in Accounting Research and Compensation Models

650 likes | 797 Vues

This presentation, delivered by Steven Huddart at Hong Kong Polytechnic University, discusses the critical role of endogenous expectations in accounting research. It emphasizes the necessity of integrating theoretical and empirical frameworks, focusing on micro-foundations and equilibrium views in management accounting. By examining various research methods, including empirical compensation studies and regulation impacts, it aims to broaden understanding of compensation structures, decision-making processes, and their influences on CEO performance through debt contracts.

Exploring Endogenous Expectations in Accounting Research and Compensation Models

E N D

Presentation Transcript

Compensation Research in Accounting Steven Huddart Hong Kong Polytechnic University June 7, 2013

Plan • Channel Demski on endogenization, equilibrium, and the art of modeling • Give examples from recent and current work and a range of research methods: • Empirical/archival compensation studies (Rhodes) • Regulation of compensation (Bozanic/Dirsmith) • Interaction of individual preferences with compensation (Fischer/Qu) • Be grateful for my good fortune in teachers, colleagues, co-authors, and students • Suggest opportunities to do more

Endogenous Expectations Analytic Modeling in Management Accounting Research Demski

Endogenous ExpectationsAAA Presidential Lecture, August 2003

Expectations are the centerpiece of accrual accounting, and expectations about these accruals and their use are the centerpiece of accounting research. Yet in our teaching and in our research we typically employ reduced-form specificationof the accounting process, coupled with transparent, largely exogenous expectation structures. The manner in which we estimate "abnormal accruals" or make use of analysts' forecasts are cases in point, as are value relevance, audit judgment, compensation and earnings response studies, and FASB deliberations. This reliance on largely exogenous expectation structures, I think, needlessly limits the depth and boundaries of our teaching and research. My purpose here is to document this claim, and to argue for a more inclusive approach to our scholarship, one that emphasizes "micro foundations" and an equilibrium view of behavior.

In emphasizing the underlying choices, my instinct is to rely on the context, forces, and behaviors involved, to emphasize the micro foundations or calculus of the choice setting, so to speak. Coupled with an equilibrium argument, we then have a picture of endogenous expectations and choices. This suggests our focus on understanding the nature and use of accounting measures should, ideally, be based on understanding how these choices are made, including the fact that coordinating forces, such as organizational architecture, market clearing, regulation, and education, are at work. Better integrating theoretical and empirical work is the key to the next round of progress, and that is why I stress micro foundations.

The Handbook of Management Accounting Research • organizational arrangements, including divisionalized structures, alliances and allocation of decision rights • decision methods and frames • evaluation and compensation, including costing systems • governance structures • the comparative advantage of the accounting system with its elaborate, nested controls and professional management.

The Ralph test • Stylize a research project to the point it can be brought into the classroom. • Is the central question in the research project of any classroom importance?

Primacy of the research question • We face an indescribably rich set of possible questions, so choose carefully. • interesting • potentially important • can be explored in depth if not answered • the research wants to know the answer • Studying how cash compensation varies with various performance measures is not very interesting. • Consider the total compensation framework. • Compensation comes in many forms and is spread across many periods. • Various forms of compensation are substitutes.

The Relation Between the Use of Accounting Measures in Debt and Incentive Contracts Rhodes

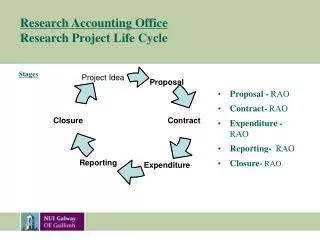

Shareholders CEO

CEO Compensation Firm Earnings

Pay for performance sensitivity PPS is measured using firm-regime-specific regressions with at least five consecutive years: CashCompensationit = α0 + α1Earningsit + εit

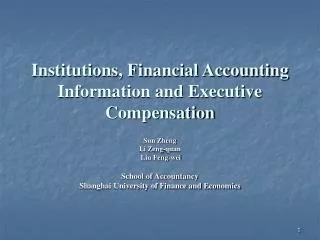

Debt contracts influence agents’ actions. • Beneishand Press (1995) show technical default being costly. • Dichev and Skinner (2002) suggest managers of firms in both good and bad financial health have incentives to avoid technical default. • Nini, Sufi and Smith (2012) show a significant increase in CEO turnover is associated with technical default, incremental to the effect of firm performance. • Interaction to explore: Do debt contracts influence compensation contract design?

Shareholders CEO Debtholders

CEO Compensation Covenant Threshold Firm Earnings

Results • CEO pay-for-performance sensitivity with respect to earnings is significantly lower when: • the firm’s debt contracts contain earnings-based covenants, and • earnings-based covenants usage is more intense in the firm’s debt contracts.

Importance • Interdependence between accounting measures in two contract settings. • There is more to compensation than just the contract between the shareholders and manager. • Debt contracts contain terms that implicitly serve to motivate a CEO. • A fuller measure of a CEO’s incentives considers incentives from the explicit compensation contract implicit incentives from other contracts.

The social constitution of regulation: The endogenization of insider trading laws Bozanic/Dirsmith

Ways to think about insider trading • How do profit-maximizing agents comply with a given set of regulations (e.g., Huddart, Ke, and Shi, 2007)? • Treat the regulatory framework as an exogenous constraint rather than as endogenous. • Specifying different rules in different economic contexts allows behavior and outcomes to be compared across regulatory regimes (e.g., Huddart, Hughes, and Williams, 20??). • The roles of agents in the process of moving from one regulatory regime to another, or in the translation of regulatory requirements into rules of the economic game, have not been modeled.

Overt Regulatory Capture • A regulatory agency is "captured" when it actually advocates for the interests of those to be regulated, especially large commercial enterprises having much at stake and considerable resources to wield in shaping policy outcomes they prefer, instead of the agency acting in the public's interest.

Ideological and Social Capture • Influence of those regulated may be subtle and indirect. • Those selected for regulatory leadership positions • often come from backgrounds sharing worldviews with those regulated • interact more with representatives from industries they regulate

Regulation is endogenous • Those regulated seek to influence emerging regulations so that the ultimate impact of the rules is muted or subverted to their advantage, i.e., they "endogenize" the regulations. • Endogenizationis an on-going, recursive process marked by moves and counter-moves among contending factions.

Illustration: SEC Rule 10b5-1 • Prohibits company officers from trading in their company’s stock while in "knowing possession" of material, nonpublic information. • Those subject to 10b5 effectively influenced this regulation (e.g., by way of successfully advocating for an affirmative defense provided for so-called "planned trades").

Processes • What are the social dynamics by which those subject to regulation seek to influence the institutional rules of the game embedded in regulations?

Endogenization processes Civil Rights Act Equal employment opportunity Securities and Exchange Act Insider trade Super-enfranchised Court theories awareness knowing possession use Seeking specificity ex ante Professionals negotiate the meaning insider trade activelyby influencing rule-writing safe harbors affirmative defenses 10b5-1 planned trades • Disenfranchised • Court theories • disparate treatment • disparate impact • sexual harassment • Exploiting ambiguity ex post • Professionals negotiate the meaning of EEO passively via “best practices” • grievance procedures • anti-harassment policies • formal hiring practices

Interpretation • The SEC was more responsive to those to be regulated by the new insider trading regulation than those whom this regulation was intended to protect from trading abuse. • While the vast majority of letters were received from non-credentialed sources, letters from credentialed actors were typically negative, and these negative letters were the letters the SEC overwhelmingly cited (by a margin of 78%) as having influenced its deliberations.

Endogenization of regulation • Justice • Government is responsive to those regulated. • Injustice • Government is differentially responsive.

Conclusion • The institutional environment affects those regulated. • Those regulatedplay an active role in defining, creating, and shaping the institutional environment

Directions • Research might: • probe the ex ante influence of those regulated on the regulations that are to constrain their behavior • examine the full range of regulatee action strategies • Compensation examples: “say on pay,” board composition rules, and rules and practices governing incentives for excessive risk (e.g., clawbacks) • Examine whether the SEC avoids endogenization by selectively: • engaging in differential enforcement • issuing interpretive and procedural rules that do not require public input proceedings • expressing general statements of policy

Optimal contracting with endogenous social norms Rotten apples and sterling examples: Moral reasoning and peer influences on honesty in budget reporting Fischer/QU

What guides behavior? • Traditional economic models incorporate • contractual incentives • legal incentives • reputation considerations • Individuals have innate preferences to conform to the behavior of their peers. • Psychology/sociology models also incorporate • injunctive norms of behavior • empirical norms of behavior

Norms for all kinds of acts • Desirable action: Kim, Morse, and Zingales (2006): • Academics’ research productivity is influenced by the cultural norm of the department that houses them. • Undesirable action: Fisman and Miguel (2006): • Differing propensities of Nigerian and Norwegian diplomats posted to New York City to accumulate unpaid parking tickets • Social norms related to corruption are significant and persistent because diplomats behave like others in their home countries. • Undesirable action: Chen and Sandino (2011) • Retail theft and collusive retail theft by employees is lower when pay is higher. • higher wages have the direct effect of curbing employee theft and also promote an ethical environment among coworkers

Incorporating Norms in an Economic Model: Two Modeling Issues • How do norms drive behavior? • Individuals incur psychic costs associated with undesirable actions. • What determines norms? • The cost incurred is due, in part, to how others in the group behave when faced with the same action choice. Hence, norms are endogenous.

Kohlberg’s (1969) Theory of Moral Reasoning Pre-conventional: responds to individual rewards and penalties Conventional: desire to respect group norms of behavior Post-conventional: motivated by personal principles and values

Assumptions • Principal employs a set of agents • Each agent i takes 2 actions • Desired action, ai • Undesired action, ui • Principal would like to induce a desired action level, ai, without inducing the undesired action, ui. • The cost of the desired action to the principal is k(ui) where k > 0

Assumptions Contract Form: wi+ bi r(ai,ui) wi is fixed wage bi is incentive parameter ri is report of performance Principal bears directly the consequences of the agents actions and, indirectly, the costs to the agents of implementing them

Assumptions • Risk-neutral agent maximizes pay net of personal cost of actions • wi + bi r(ai,ui) – f(ai– Nai)– f(ui+ Nui ) • where f(x) is the cost of the act Naiis psychic cost to i due to norm for action a

Assumptions • Norm of behavior, Ni, satisfies • Ni = (1 –ai)Ai– aiS, where Ai represents the personal standard of agent i Sis the endogenous average behavior of the peer group, i.e., the empirical norm ai [0,1) represents extent to which agent is conventional

Features • Undesirable action, ui, favorably influences performance measure used for contracting. • Undesirable action is costly to the principal. • Undesirable action choice is influenced by a personal norm of behavior, Ai, and a social norm of behavior, S. • The weight on the social norm, ai, measures the extent to which the agent is conventional. • Social norm of behavior is endogenous—it depends upon how agents behave within the organization.

Findings • Spillover effects arise from incentive contracts when social norms are endogenous. • High-powered incentives imply less effective social norms. • Post-conventional preferred when incentives are high. • Conventional preferred when incentives are low.

Findings • Norms for desirable action multiplies the benefits of financial incentives, while the presence of a norm for undesirable action reduces the benefits. • Agents’ relative sensitivities to each type of norm determines whether it is beneficial to split an organization apart to foster different norms in each part. • Differences in sensitivity to social norms create a costly adverse selection problem when the differences pertain to social norms for undesirable actions, but not when the differences pertain to social norms for desirable actions.

Foundational Questions • How and to what extent are individuals influenced by honest (or dishonest) example set by peers? • How do individuals’ responses to the actions of others vary across moral types? • How does susceptibility to external social influences vary with one’s personal standard?

Contributions • Probe with an experiment the validity of assumptions about individual preferences that underlie such models as Fischer & Huddart (2008). • Examine how individual traits such as moral types explains heterogeneous reporting behavior and susceptibility to social influences. • Extend ethics research in accounting by linking moral types to practical reporting outcomes.

Budget Reporting Experiment • Experimental setup • Participants play the role of managers • Observe private cost C perfectly • Submit budget report R to headquarters • Maximum cost is 6 and minimum cost is 4. • Economic Incentive (in Lira) • Fixed salary+budget slack:1000+1000*(Report-Cost) • Prior experimental evidence(Evans et al. 2001) • Reports are partially honest • Reporting Honesty=1.00- (Report-Cost)/(6-Cost) • Average honesty is 0.45.