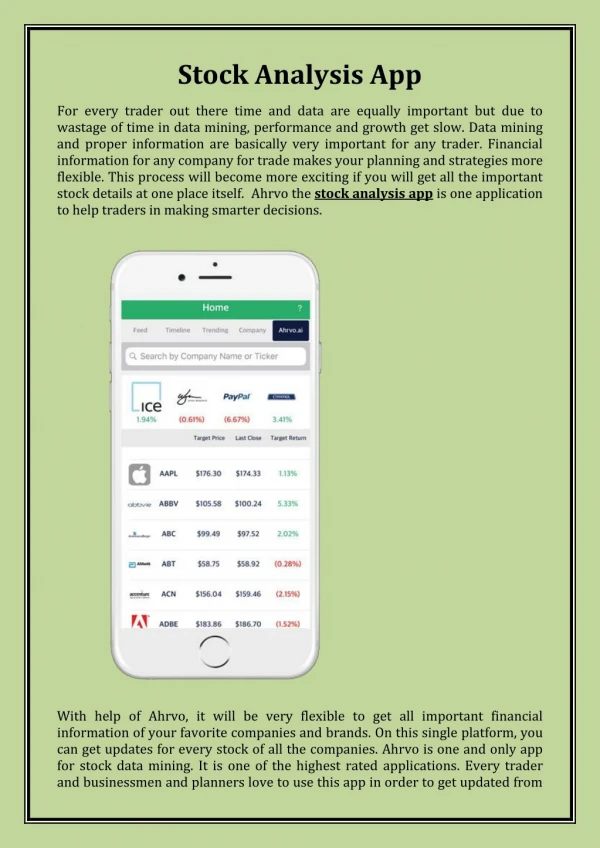

Initial Stock Analysis

This report provides a comprehensive analysis of price and return dynamics for Apple Inc. (AAPL) and Ford Motor Inc. (F) over various time periods. It examines measures of volatility, including realized volatility (RV) and bipower variation (BV), while considering stock splits and their adjustments. The study includes minute-by-minute geometric returns and volatility signatures, offering insights into the relative contributions of jumps and the impact of microstructure noise. The report also sets forth future steps to compare Apple and Ford's volatility with other industry players.

Initial Stock Analysis

E N D

Presentation Transcript

Initial Stock Analysis Andrew Bentley February 8, 2012

Outline • Price and returns for Apple Inc. (AAPL) and Ford Motor Inc. (F) • Measures of Volatility • RV, BV, Sub-Sampled RV, TV • Volatility Signatures • RV and BV • Relative Contribution of Jumps • Basic Comparison Between these Measures

Price and Returns • Unadjusted plots of price data against time • Adjusted plots of price data against time after correcting backwards for stock splits • Minute-by-minute geometric returns • “Returns” graphs consider intraday minute-by-minute returns as well as overnight returns.

AAPL: Unadjusted Prices 2:1 Split 2:1 Split

AAPL: Stock Splits • Three 2:1 Stock Splits • June 15, 1987 • June 21, 2000 • February 28 2005 • The June 2000, and February 2005 splits fall in the data range • Price adjusts “backwards” to account for the splits

F: Price Nov. 2006 Dec. 2008

Measures of Volatility • Goal is to measure the integrated variation • for a process: • The realized variance:

Estimators for IVt • Bipower Variation (BV): • Threshold/Truncated Variation (TV)

Truncated Variation, TVt(AAPL) • AAPL, cutoff of 4 standard deviations

Truncated Variation, TVt(F*) • F, cutoff of 4 standard deviations

Effects of Microstructure Noise • Observed data is actually some price plus some noise term • Look for ways to wash out the effect of the noise without loosing the vast majority of the data • Sub-Sampling • k can be thought of as an “offset”

Volatility Signatures • Measure of the calculated unconditional variance of the stock as a function of the sampling interval Δ • For T time periods, the average realized variance is: • This number is then properly annualized. • Replace RVt by BVtand other measures of intraday variance

Next Steps: • Examine Relative Contribution of Jumps of AAPL vs. those of F • Calculate correlation of the two vectors • Expected to be low. • Look at stock that are both in the same industry • Examine volatility of Apple with that of Microsoft, Google, Intel, and other technology sector firms. • Examine volatility of Ford with other car manufacturers like GM. • Examine correlation of intra-industry stocks • Expected to be high.