Download

1 / 7

70 likes | 83 Vues

Explore the complexities of bank regulation, stress tests, and broken business models in the European banking sector. Understand the impact of runs and deleveraging on financial stability and learn strategies to address these issues effectively.

E N D

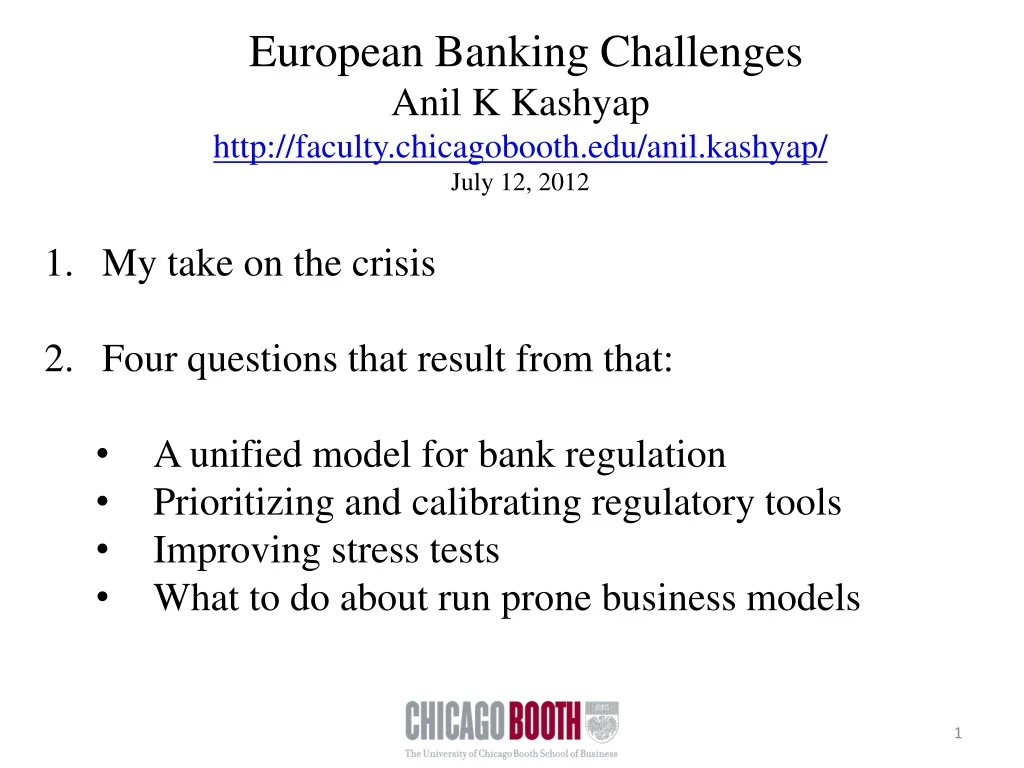

European Banking Challenges • Anil K Kashyap • http://faculty.chicagobooth.edu/anil.kashyap/ • July 12, 2012 • My take on the crisis • Four questions that result from that: • A unified model for bank regulation • Prioritizing and calibrating regulatory tools • Improving stress tests • What to do about run prone business models

Component 1 of the crisis: Runs • The crisis featured 5 non-traditional runs that mostly caught us by surprise: • ABCP • Repo (specifically regarding Bear Stearns) • OTC customers • Prime Brokerage customers • MMMFs

Component 2 of the crisis: Deleveraging • Deleveraging is critical because • Explains the amplification of the initial subprime shock • Explains the pervasive fire sales in fall 2008 • Hunch: it has something to do with the slow recovery, from both the household side and the corporate side • What is the mechanism that explains Reinhart-Rogoff?

Question 1: Modeling • What is the right model for nesting fire sales, deleveraging and default? • My answer is that work on financial frictions ought concentrate on “credit supply” problems, but that still leaves lots of unanswered issues.

Question 2: Regulatory Tools • How do we pick between capital, liquidity, loan to value, debt to income, haircuts/margins, dynamic provisioning, deposit insurance, taxes? • Which bundles work best together? • How do we calibrate the settings? • My provisional answer: think about markets channels through which tools operate, not the agents on which they bind.

Question 3: Stress Tests • Was the SCAP lucky or best practice? US banks raised equity, Europeans have not. Why? • The resolved asymmetric information • The public backstop in the US was key • Chris Dodd’s threat of restricting pay • My provisional answer, definitely not asymmetric information

Question 4: Broken Business models • Global regulation has gotten bogged down tackling run prone business models • MMMFs (a well funded menace) • Prime Brokerage • MMMFs need capital or variable NAV • Primer Brokerage is harder to fix, what is the social value of collateral (and do we have enough safe assets)?