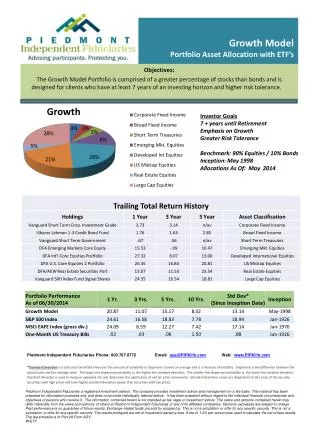

Studies into Global Asset Allocation using the Markov Switching Model

310 likes | 463 Vues

Studies into Global Asset Allocation using the Markov Switching Model. October 2007. Overview. Background Aim of thesis The model Results Summary. Background. The main question …. Are forecasts of financial markets more powerful if a switching process is incorporated ?

Studies into Global Asset Allocation using the Markov Switching Model

E N D

Presentation Transcript

Studies into Global Asset Allocation using the Markov Switching Model October 2007

Overview • Background • Aim of thesis • The model • Results • Summary

The main question …. Are forecasts of financial markets more powerful if a switching process is incorporated ? • This question leads to many issues • For today just focus on FX – although equities and bonds covered in thesis Background

Previous studies • Forecasting returns for international financial markets (FX, Equities, Bonds) quite common in both practical and academic publications • Harvey (1994 etc) , Ilmanen (1996), Messe & Rogoff (1983) …. • But very few “comprehensive” pieces – multiple markets, economic relevance Background

Theory: Frankel – Froot Model Expensive, strong momentum Time • Constant interaction between value and momentum Cheap, poor momentum Fair Value Background

The 5 Questions • Is there are predictable component to international investment returns • Linear regressions • Is there evidence to support the Frankel – Froot model • Compare linear vs. Switching / Frankel Froot • What is the nature of switching in international markets • Conditional switching vs. Markov switching • Is there an economic relevance to the modelling • Portfolio simulations • Is there a memory of success of styles • Reward models Aim of the thesis

Currency Model - Value • Money Supply Model • Strong theoretical basis • Well recognised • 12m changes for each variable (so no base year issues) The model

Currency Model - Momentum • Price Momentum & Sentiment • Natural extension from Chan, Jegadeesh & Lakonishok (1996) The model

Regression results 1) Is there are predictable component to international investment returns ?

Can Combine theory with model – The Markov Switching Model • Markov Switching model synonymous with works of Hamilton (early 90s) • Commonly accepted non linear model • Been used in FX markets, very rarely seen in other asset classes • In this case – each regime is represented as a “state” 2) Is there evidence to support the Frankel – Froot model

The Two States Value State Momentum State Transition 2) Is there evidence to support the Frankel – Froot model

Log Ratio Tests • Not strictly comparable, but evidence quite compelling • Frankel Froot structure stronger than 17/20 competing models 2) Is there evidence to support the Frankel – Froot model

Conditional and Unconditional Switching • Switching can be naïve and endogenous • Use this to understand the nature of the switching • Use forecast GDP (wealth) and volatility (fear) as influences on switching environment • Loosely follows a utility function 3) What is the nature of switching in international markets

Conditional Switching Transition Transition function 3) What is the nature of switching in international markets

Log Ratio Test • Not uniformly conclusive, either very powerful or basically noise 3) What is the nature of switching in international markets

Further conclusions • Average duration of value regime >6m, while for momentum <2m. Supports Frankel – Froot hypothesis • Generally length of both regimes get shorter in volatility – whipsawing of investment styles, while regimes get longer in times of wealth 3) What is the nature of switching in international markets

Economic Relevance 4) Is there an economic relevance to the modelling ?

Economic Relevance • Also ran optimised portfolios 4) Is there an economic relevance to the modelling ?

Economic Relevance • More powerful forecasts from switching • Other markets show that cross sectional information increases, although time series decreases • Money can be made from these models 4) Is there an economic relevance to the modelling ?

Is there memory ? “The model of speculative bubbles developed by Frankel and Froot (1988) says that over the period of 1981-85, the market shifted weight away from the fundamentalists, and towards the technical analysts or “chartists”. This shift was a natural Bayesian response to the inferior forecasting record of the former group, as their forecasts of dollar depreciation continued to be proven wrong month after month” • Frankel, Jeffrey and Froot Kenneth, October 1990, pg 22 5) Is there a memory of success of styles ?

Test with reward model • Reward of 1,-1, based on the success of last month • Do 5 years of rolling regressions • Test values of λ for relevance • Can also compare against each regime (see who is forgotten quickest) 5) Is there a memory of success of styles ?

Graph of reward model 5) Is there a memory of success of styles ?

Test with reward model • Reward of 1,-1, based on the success of last month • Do 5 years of rolling regressions • Test values of λ for relevance • Can also compare against each regime (see who is forgotten quickest) 5) Is there a memory of success of styles ?

Reward model results • Has memory, momentum forgotten quicker (truely short term) 5) Is there a memory of success of styles ?

Summary • Markets have some level of predictability • Switching better than linear • Regime switching may lead to less “accurate” individual forecasts – but possibly contain more information • Can loose information in time series, but gain cross sectional information. Summary

Summary • Switching in defensive assets more likely to be driven by fear, where in aggressive assets more likely to be driven by greed • Regime switching portfolios outperform linear counterparts • Memory exists – but differs between markets and asset classes • Frankel – Froot model well supported Summary

Comprehensive Testing • Regression results (linear, regime switching) • Forecast analysis (in / out of sample statistical) • Simulated portfolios (optimised and naïve) • 5 currencies, 9 equity markets, 6 bond markets • 10 years data • Over 10,000 regressions Summary