Download

1 / 15

150 likes | 470 Vues

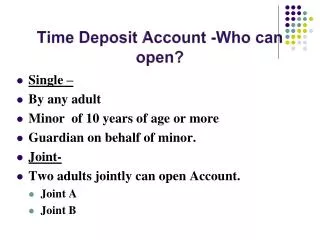

Recurring Deposit account (Who can open?). Single account- Can be opened by any adult A minor of 10 years of age or more By guardian on behalf of minor Joint account- Two adults can open Account as Joint. FEATURES Recurring Deposit Scheme.

E N D

Recurring Deposit account (Who can open?) • Single account- • Can be opened by any adult • A minor of 10 years of age or more • By guardian on behalf of minor • Joint account- • Two adults can open Account as Joint. RULE NO : 105-106 POSB Manual Volume -I

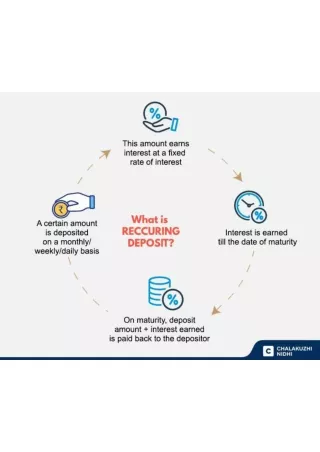

FEATURES Recurring Deposit Scheme • Minimum Denomination Rs.10/- and thereafter in multiple of Rs.5/-. • Maximum - No limit • Maturity period - 5 years. • Maturity value for Denomination of Rs.10/- • A/c opened from 01/03/03 to 30/11/11 = Rs.728.90 • A/c opened from 01/12/11 to 31/03/12 = Rs. 738.62 • A/c opened from 01/04/12 to 31/03/2013 =Rs.746.51 • A/c opened from 01/04/13 onward =Rs.744.53 • Rate of Interest ------ 8.3 % w.e.f. 1/04/2013 RULE NO : 105-106 POSB Manual Volume -I

Loan/Withdrawal • One interim withdrawal is allowed during the period of 5 years. • Admissible after one year from the date of opening. • Twelve deposits should have been made. • Should not be a discontinued account. • Up to 50% of the amount at credit on the date of loan can be withdrawn. • Amount of withdrawal should be divisible by 5. • Any withdrawal/loan taken on or after 01.01.2005 interest will be charged as per the interest fixed for the 5 year TD account + 2 % • The withdrawal/loan amount can be repaid in one lump sum or in instalments • Depositor may repay the amount of withdrawal in equal instalments or in lump sum • The repayment should be in equal monthly instalments and in multiples of Rs.5/- • Instalments should not go beyond maturity date. RULE NO : 105-106 POSB Manual Volume -I

Premature Closure • Permissible only after three years from the date of opening. • If there are advance deposits, account can not be closed prematurely till the period of advance is over. • Interest will be calculated at the rate of savings accounts • Default fee paid if any will be refunded to the depositor • Rebate paid if any is recovered. • Head and Sub Offices are authorised to close the account independently • Post maturity interest – For completed months up to date of payment from the date of maturity at the rate of SB account. RULE NO : 105-106 POSB Manual Volume -I

Default Fee • If a depositor does not deposit the monthly installment in due time default fee is charged. • Default fee @ 2% of Denomination will be charged • Maximum Four defaulted installments are permissible in an RD account at a time. • If five defaulted installments becomes due, Account is treated as discontinued, depositor can continue the account by depositing all the due installments together in the sixth month. • After it the account will permanently discontinued and depositor can not continue the account. • A permanently discontinued account can be only be closed either after 3 Years of opening or after maturity i.e. 5 years from the date of opening. RULE NO : 105-106 POSB Manual Volume -I

Rebate • If monthly installments are paid in advance for 6 month or more , rebate will be paid at the following rate. • Denomination Rs. 10/- • Up to 5 months - Nil • For 6 months to 11 months - Re.1/- For 12 months or more - Rs.4/- • Proportionate for other Denomination. Rule No.

Counter Operation Recurring Deposit New Account Open • Procedure same as per Savings Bank new account open • If opened through cheque, date of clearance of cheque will be the date of opening RULE NO : 103 POSB Manual Volume -I

A/C OPENING BY CHEQUE • RD account can be opened by means of crossed cheque or demand draft issued in favour of Postmaster or the depositor. • In this case, entry of deposit will not be made in the pass book. Pay-in-slip will be accepted and counterfoil duly date stamped should be handed over to the depositor. • Cheque/draft will be sent for clearance and after realization of the cheque, entry will be made in the account as well as passbook. However, date of opening of account will be the date of presentation of the cheque.

Contd…… • If the cheque presented for deposit is not drawn in favour of the Postmaster by the depositor the following conditions should be satisfied. • Counter PA will check that endorsement as per following procedure has been made on the back of cheque:- • If the cheque is drawn in favor of the Postmaster by the depositor or by a person other than the depositor, it must be endorsed on its back as, “ for opening of…………account in the name of……………..( signature of drawer)”. In case the cheque is drawn in favor of depositor, it must be endorsed by the depositor for payment on its back as “ Pay to Postmaster…………………P.O for opening of………………account in the name of………………(signature of depositor) Rule No.

Counter PA should also check that:- • (i) If the cheque is drawn if favour of the depositor, he will either himself or his messenger enter details of cheque in pay-in-slip. • (ii) There is also no objection to the acceptance of cheque drawn by a third party in favour of the Postmaster provided the cheque is accompanied by an application from the depositor requesting the Postmaster to credit the amount into his account. • Note:- A cheque drawn on the POSB in favour of a person other than the depositor may also be accepted for credit in Post Office Savings Bank provided it has been duly endorsed in favour of the depositor. Rule No.

Contd…… • (iii) the cheque is neither postdated nor is more than 6 months old. Cheque drawn by a government department should not be more than 3 months old. • (iv) the cheque is written and signed in ink or with ball point pen. • (v) the cheque is drawn or endorsed in favor of the Postmaster of the office in which the account of the depositor stands. • (vi) the cheque should be crossed generally or specially to the Post Office Savings bank. • (viii) the cheque is not mutilated or torn and there are no over writings, erasures or corrections. Rule No.

Final Closure of RD account Account can be closed after completion of 5 years Application for withdrawal duly filled along with passbook should be submitted at the post office where the account stands Account will be closed at all HOs and departmental Sub offices independently If the date of maturity falls on holiday or Sunday, the account can be closed on previous day

Extension of RD account • Account can be continued with or without deposit for another block of five years. • No application required from the depositor to extend the account. • Can be closed any time during extension period. • Interest is paid @ applicable on the date of opening. • If continued, interest is paid as per the tables supplied by the department

Protected Saving Scheme • Under PSS Scheme if the depositor dies, full maturity value is paid to the nominee/legal heir • Conditions : • Benefit is extended to only one account • Available to accounts of denomination up to Rs 50/- • The age of the depositor at the time of opening the account should be between 18 and 53 years • The instalments should have been paid for 24 months

Protected Saving Scheme…. • 2 years should have been completed • During first 24 months, no withdrawal should have taken place • Account should not be a discontinued one • Claim should be preferred within one year from the date of death of the depositor • The Head Postmaster will settle the claims