Download

1 / 36

431 likes | 738 Vues

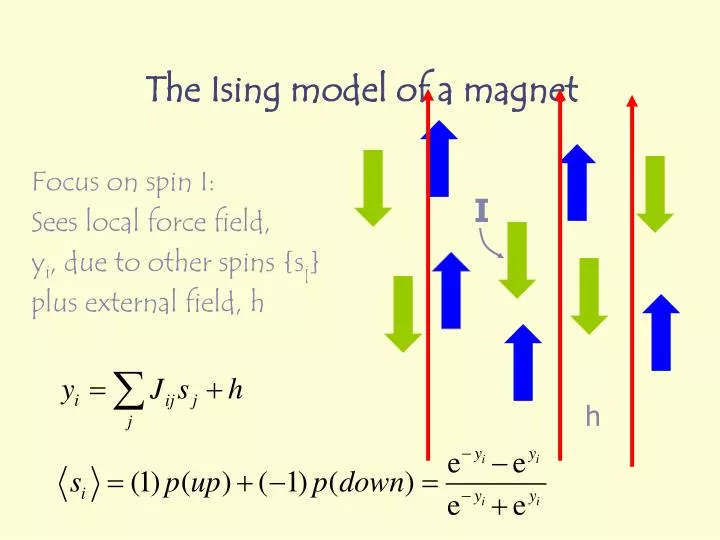

I. h. The Ising model of a magnet. Focus on spin I: Sees local force field, y i , due to other spins {s j } plus external field, h. Agents and forces. Forces in people -agents. buy. Hold. Sell.

E N D

I h The Ising model of a magnet Focus on spin I: Sees local force field, yi, due to other spins {sj} plus external field, h

Forces in people -agents buy Hold Sell

Cooperative phenomenaTheory of Social Imitation Callen & Shapiro Physics Today July 1974Profiting from Chaos Tonis Vaga McGraw Hill 1994

Time series and clustered volatility • Three states buy, sell, hold, do nothing • friction • T. Lux and M. Marchesi, Nature 397 1999, 498-500 • G Iori, Applications of Physics in Financial Analysis, EPS Abs, 23E

Auto Correlation Functions and Probability Density Numerical…but how can we understand what is going on?

Langevin Models • Tonis Vaga Profiting from Chaos McGraw Hill 1994 • J-P Bouchaud and R Cont, Langevin Approach to Stock Market Fluctuations and Crashes Euro Phys J B6 (1998) 543

A Differential Equation for stock movements? • Risk Neutral,(β=0); • Liquid market, (λ-)>0) • Two relaxation times • 1 = (λ-)~ minutes • 2 = 1 / ~ year • =kλ/ (λ-)2

R Gilbrat, Les Inegalities Economiques, Sirey, Paris 1931 O Biham, O Malcai, M Levy and S Solomon, Generic emergence of power law distributions and Levy-stable fluctuations in discrete logistic systems Phys Rev E 58 (1998) 1352 P Richmond Eur J Phys B4 (2001) 523 P Richmond and S Solomon Int J Mod Phys 12 (3) 2001 1 Over-optimistic; over-pessimistic;

Generalised Lotka-Volterra wealth dynamicswith Sorin Solomon, Hebrew University • a – subsidy/taxation/ ‘minimum wage’ • c – measure of competition • w – total wealth in economy =w(t) • D – ‘economic temperature’

Lower bound on poverty drives wealth distribution! wmax wmin

Why has Pareto exponent remained roughly constant and ~1.6-7 • Min wealth to survive is ~K • Average family has L members • Family needs KL or become violent, strike etc • <w> is by definition min since prices adjust to it ie KL~<w> • So poorest people who have no family will seek to ensure they receive <w>/L • Thus wmin~<w>/L • a = 1/(1- x m) ~ L/(L-1). • If L=3 then a =1.5 ; L=4 a =1.33; L>inf a >1

UK Income Distributions ?Boltzman distribution Badger 1980 Montroll & Shlesinger 1980 Cranshaw 2001 Souma 2002 UK

Problems • No clustered volatility • Not quite right shape around peak

Random walks Time Time

20th century maths • Fractional derivatives

19th century Irish Stock Exchange • Deals done 'matched bargain basis' • members of exchangebring buyers and sellers together • Essentially same as today albeit electronic trading • Today, many more buyers and sellers. • Recent studies of 19th century markets find they were well integrated (Globalization and History, Kevin H. O'Rourke & Jeffrey G. Williamson, MIT Press 1999) • Dublin traded international shares • Not solely a regional market. • World trends reflected in the Irish market • No exchange controls. • From 1801 to 1922 Ireland was part of UK • Largest shares: Banks and key railways – • Quality investments for UK investors • Also traded in London.

Irish Stock Market data. Fractional time derivativesLorenzo Sabatelli, Shane Keating Jonathan Dudley

Entropy • Energy is about what is possible • Entropy is about the probabilities of those possibilities happening • A measure of number of possibilities or states available, W

Long history of application to equilibrium but near critical points….???? Boltzmann-Gibbs Entropy

Issues • Self-organised critical systems? • Power laws? • Fractal behaviour? • Non extensive behaviour?

Tsallis ~1990 • Weighting of rare events.

Power laws and non-extensivity • Tsallis Cond-mat 0010150 • Mixing in many body systems • Complexity

Applied to stock returns • Michael & Johnson cond-mat/0108017 • S&P returns 1 minute data • q~1.4

Simulation • Long term buy hold • Noise trader • Fundamental trader • …….

And finally.. Chance to dream(by courtesy of Doyne Farmer, 1999) $1 invested from 1926 to 1996 in US bonds $14 • $1 invested in S&P index • $1370 $1 switched between the two routes to get the best return……. $2,296,183,456 !!

Alternative possibilities • Higher moments automatically scale as sums of power laws with different slopes (Bouchaud et al • Asyptotically dominant power law has exponent q • But for smaller values of τ, another power law whose exponent is non-linear function of q might dominate • Apparent multi-fractal behaviour, even though the process is a simple fractal with all moments determined by scaling of a single moment. • For short data set, simple fractal may seem like multifractal due to slow convergence.

Heavy Tails of Buy/ Sell Order Volumes & Market Returns Distributions • In most real markets, trades take place by matching pairs of buy and sell orders with compatible prices. • Volume of each trade equals smallest volume of matched pairs • Probability for each of 2 matched orders to exceed (or equal) a certain volume v is P(>v) ~ v-α • Probability that both have a volume (equal or) larger than v is product P(>v)P(>v)~v-2α • Prediction of GLV for such market measurements is that trades volumes and trade-by-trade returns follow power law with exponent γ ~ 2α ~ 3