Download

1 / 13

140 likes | 307 Vues

Calculating the Future and Present Value of Money. Future Value. FV = p • (1 + i) n Things we need to know: Interest rate = i Number of periods (years) invested = n Principal amount invested = p. Also, if the principal amount is not given, we need to know the future value = FV.

E N D

Future Value • FV = p • (1 + i)n • Things we need to know: • Interest rate = i • Number of periods (years) invested = n • Principal amount invested = p Also, if the principal amount is not given, we need to know the future value = FV

FV = p • (1 + i)n • Let’s assume that you have $1,000 to invest over a period of 5 years. Your investment is expected to earn 7% interest. • p = $1,000 • i = 7% • n = 5 Here is the formula you would use: FV = $1,000 • (1 + .07)5

FV = $1,000 • (1 + .07)5 • First, calculate the factor using the rate and length portion of the formula:1.075 = 1.07 • 1.07 • 1.07 • 1.07 • 1.07 = 1.40 • Next, multiply the factor by the amount invested to determine the future value $1,000 • 1.40 = $1,400 • The answer is $1,400. What does this mean?

Future Value • Based on the previous information, your $1,000 would be worth $1,400 five years from now. • This information can be useful when trying to plan for your future or purchase the luxury yacht you have been wanting.

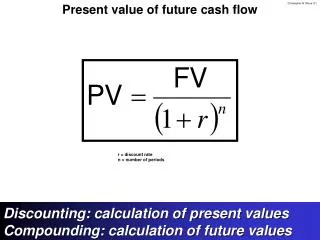

Present Value • PV = FV • 1 / (1 + i)n • Things we need to know: • Interest rate = i • Number of periods (years) = n • Future value = FV • Also, if the future value is not given, we need to know the present value = PV

PV = FV • 1 / (1 + i)n • Let’s assume that you need $1,000,000 to purchase your luxury yacht. You want to purchase this yacht in five years. The rate of return is 8%. • FV = $1,000,000 • i = 8% • n = 5 • Here is the formula you would use: PV = $1,000,000 • 1 / (1 + .08)5

PV = $1,000,000 • 1 / (1 + .08)5 • First, calculate the factor. This is done in two steps: • Calculate the denominator using the rate and length portion of the formula:1.085 = 1.08 • 1.08 • 1.08 • 1.08 • 1.08 = 1.469 • Divide t by the denominator calculated above to determine the factor:t / 1.469 = 0.6807 • Then, multiply FV by the factor to arrive at PV:$1,000,000 • 0.6807 = $680,700 • The answer is $680,700. What does this mean?

Present Value Based on the previous information, you would need to invest $680,700 now to purchase a $1,000,000 yacht in five years.

Lottery Winners Lottery winners are often faced with a big decision: Do I take the cash option, or do I take the annual payments over the course of a 25-year period? Let’s assume the lottery you have just won is valued at $34 million*, with a cash option of $16.2 million*. Using the time value of money, we can calculate which payment method would net you more money. *Taxes not included

Cash Option vs. Annuity Option If you were to select the cash option, you would receive $16.2 million today. Let’s calculate what your annuity payment option would be worth today. Your annual payments would be $1,360,000 for a 25-year period ($34,000,000 / 25 years), and we will assume an interest rate of 6%.

Cash Option vs. Annuity Option Based upon our calculations, it would be more beneficial to select the Annuity payouts. This would result in receiving an additional $1,168,560 over a 25-year period in today’s time value of money.