Download

1 / 10

100 likes | 251 Vues

Long-Term Growth in the European Union: Some Observations. Dr. Danny M. Leipziger Prof. of International Business George Washington University. Five Factors to Consider. The Labor Market Factors The Accumulation Factor The Moral Hazard Factor The Trichet Factor The Looking East Factor.

E N D

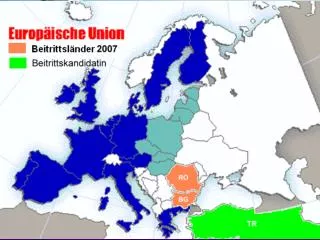

Long-Term Growth in the European Union: Some Observations Dr. Danny M. Leipziger Prof. of International Business George Washington University

Five Factors to Consider • The Labor Market Factors • The Accumulation Factor • The Moral Hazard Factor • The Trichet Factor • The Looking East Factor

Labor Market Factors • Ageing populations should raise wages in the long-run; however, with an inability to adjust internally to productivity differences (MW)—the German Stakhanovite worker problem-- will increase income differentials (UD) • Possible solution could be Singapore Tripartite Councils to enforce wage adjustments, although the rich EU members will be able to invest in new capital and the poorer not • Other alternative is increasing transfers to reduce income disparities, but will all members agree?

The Accumulation Factor • Imbalances among members resembles the US and China—excessive savings and surpluses matched by stretched govt deficits • The imbalances perpetuate themselves since the deficit members cannot devalue and also cannot invest given their fiscal indebtedness • The short-term solution is subsidies and transfers among groups of members but the Germany public seems tired of this but leaders are unwilling to see Euro-exit

The Moral Hazard Factor • Cheating and off-balance sheet expenditures predates Greece • Debt restructuring seems unpalatable although perhaps the best among poor options of euro-exit or the status quo. • Impossibility of member default creates moral hazard and mis-alignment between incentives facing the Union vs individual members

The Trichet Factor • Notion that adjustments are handled inside the Club is short-sighted and adds to cost • Greece mishandled from the start • More Intra-EU bailouts to come • The ECB will buy distressed assets at inflated prices and this confuses monetary policy • Combined with the Chang-Mai Initiative, the EU bailout fund of $ 1 trillion makes global solutions and IMF seem out of date.

The China Factor • Given lack of aggregate demand in surplus, hyper-savers and fiscal squeeze limiting demand in the highly indebted, luckily exports to China have emerged to prod growth • But how long will it last? China will move into higher tech industries one way or another • Will the golden goose turn into a hawk? • ECB will have a tough decision whether to allow Euro appreciation hurting exports and growth or sterilize inflows.

How Much Are Surplus EU Members Willing to Pay? • Pay to buy semi-distressed members’ debt to protect Euro integrity • Fund transfers to the “ south “ to offset lagging productivity and widening intra EU inequality • Finance additional investments in the south since aggregate demand will remain depressed and productivity differences will grow unless workers move north • Divert monies from pro-growth spending to maintain competitive euro and low inflation policy mix—cost of sterilization and 2% target

Predictions • Demonstrated willingness to pay an enormous price for EU stability and unity will prevail • Chinese import demand alone will not suffice • Costs will rise with greater transfers needed • Welfare levels may well decline • According to behavioralists, Europeans may still be happier nonetheless