Download

1 / 25

250 likes | 409 Vues

The Balanced Scorecard: A Framework for Accountability. Presenters: Maureen Pettitt, Skagit Valley College, WA Doug Whittaker, Washington State Board for Community and Technical Colleges.

E N D

The Balanced Scorecard: A Framework for Accountability Presenters: Maureen Pettitt, Skagit Valley College, WA Doug Whittaker, Washington State Board for Community and Technical Colleges

“Colleges and universities are moving into a period when they will be expected to provide not only data on the attainment of defined outcomes…but also evidence that results have been attained at a reasonable cost. [They] will have to specify their aims, stand ready to justify activities, demonstrate their contribution to objectives, and defend the cost of the enterprise.” Berdahl & O’Connell (1999). American Higher Education in the Twenty-First Century.

External Accountability • Accountability performance indicators are developed for external audiences with limited areas of interest, resulting in measures that are “incomplete and one-dimensional views of performance.” • Desired improvements are unlikely to occur “until performance measures are linked to the drivers of institutional effectiveness in a meaningful way.”

State Performance Measures http://www.acct.org/policy/Accountability_Report.htm

Internal Assessment • To be useful internally, performance indicators must be tied to institutional values, goals, and objectives… • …and the objectives must be translated into specific research problems that can be studied...and around which strategies for improvement can be developed.

Balanced Scorecard • After publishing several well-received articles in HBR, Harvard professors Robert Kaplan and David Norton released their book in 1996

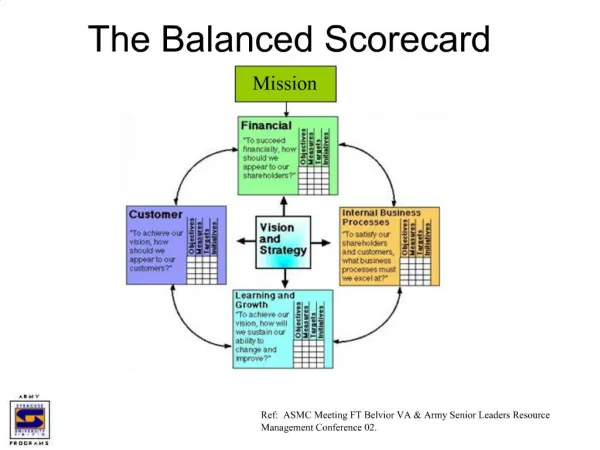

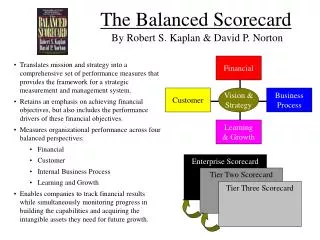

Definition • The Balanced Scorecard is a multidimensional framework that provides an ‘enterprise’ view of the organization’s overall performance by integrating financial measures with other key performance indicators.

“Think of the balanced scorecard as the dials and indicators in an airplane cockpit. For the complex task of navigating and flying an airplane, pilots need detailed information about many aspects of the flight...

They need information about fuel, airspeed, altitude, bearing, destination and other indicators that summarize the current and predicated environment. Reliance on one instrument can be fatal. Similarly, the complexity of managing an organization today requires that managers be able to view performance in several areas simultaneously.” Kaplan and Norton, 1992

Balancing Perspectives • Too often bad strategic decisions are made in an effort to increase the “bottom line” at the expense of other institutional goals. The BSC suggests that financial performance should not be viewed as the focus, but as the natural outcomeof balancing other important goals.

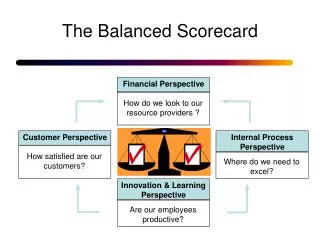

Four Strategic Issues • Customer • Internal business process • Financial • Innovation and learning

responsiveness, timeliness product/service quality and cost meet client needs “How do customers see us?” Customer Perspective

“At what must we excel?” accurate and timely delivery of services effective systems and processes environmental sustainability Internal Business Process Perspective

budgets revenue capital expenditures debt to asset ratio “How do we look to our key stakeholders?” Financial Perspective

“Can we continue to improve and create value?” employee skills and training use of technology encouragement of innovation continuous improvement Innovation and Learning Perspective

Ultimate Balancing Act The ultimate balancing act in any organization is the one whereby the needs and requirements of multiple stakeholders are reconciled and integrated.

Examples • Ohio State University • USC Rossier School of Education • Southwest University • Pacific Northwest College Exercises

Strategic Planning • An effective scorecard will identify a set of strategic questions, objectives, and measures that address the issue of adding value--and doing so at a rate that is better than the competition. This is the essence of strategy.

Strategic Planning (con’t) A balanced set of indicators can systematically stimulate better understandings and deeper insights that can form the basis for strategy.

Four Key Processes Translating the vision Feedback and learning Business planning Communicating and linking

Four Key Processes • Translating the vision helps managers build a consensus around the institution’s strategy and express it in terms that guide action • Communicating and linking lets managers communicate their strategy institution-wide, and link it to unit and individual goals

Four Key Processes (con’t) • Business planning enables the institution to integrate its business and financial plans • Feedback and learning give institutions the capacity for strategic learning, which consists of gathering feedback, testing the hypotheses on which strategy was based, and making adjustments